")

")

")

")

")

Dear readers/followers,

Atea (OTCPK:ATAZF) (OTCPK:ATEAY) is an interesting IT company in the Nordic geographies that has seen good improvements over the past year or so, with better fundamentals and better low-risk operating specifics. In my last coverage back in December of 2023, I went positive on the stock. Because the ADR ATAZF is so thinly traded, it doesn’t yet appear in terms of development, but you can at the very least find my article on the company here.

Atea’s market position and exposure to Scandinavian organizations make it an attractive investment in the IT sector, but caution is advised due to potential macro-related risks – but those risks are as of now, not as high as they once were when I started covering the company many years ago. Also, and more importantly in this interest rate environment, the company’s fundamentals are vastly improved here.

What we’ll do here is update the company thesis for my recent “BUY” stance, see if my targets and that stance is still relevant, and see what we’ll do in terms of price targets and upside for 2024-2025. In short, to see if I will invest more, and if I believe it could be an idea for interested investors to do the same.

Atea ASA – An attractive IT company with a local market-leading profile

One of the best qualities about Atea as a business is the fact that it really offers a sort of market-leading or market-dominating advantage in Scandinavian geographies and markets. While it does something simple, like selling IT hardware and services as well as software services, which isn’t exactly one of the most advanced things a company can do in terms of services – it has scale and market advantage.

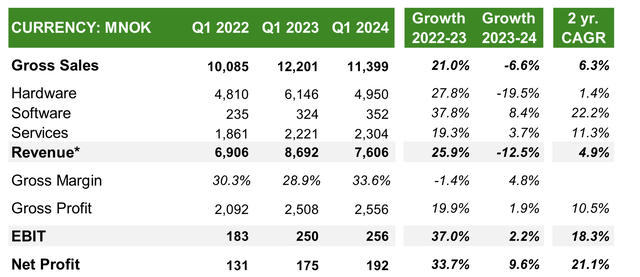

We’ll start by looking at the quarterly trends. Company revenues are down around 12.5% year-over-year, with revenues for the quarter of 7.6BNOK – but while revenues and top-line trends are down, the profitability of the company is significantly improved. Net income is up nearly 10%, gross profit is up almost 2%, and EBIT is up over 2%. So what has happened here?

Sales mix and improved profitability. Hardware is down from very high levels in last year, but what’s happening to the P&Ls here is increased software and services revenue mix, which come at higher gross margin levels and improve the results while absorbing a decline in overall revenues.

Atea IR (Atea IR)

Atea works with a group structure based on Geography – and for 1Q24, it was relatively clear what’s happening under the hood in the geographies here. Sweden, Denmark, and Finland as well as the Baltics saw a decline in company revenue, some as high as 30%, while the company’s core market of Norway was up 1.4%. The interesting trend was in margins though because every single company geographic segment saw significant margin improvements. The gross margin in say, the Baltics, is up almost 40%, and that is almost sector-leading here in Scandinavia. Core geographic sectors like Norway and Sweden are 33-36%, with Denmark and Finland between 21-31%.

In terms of earnings, Denmark remains the “company black sheep” here, generating negative EBIT. This geography has been the cause of many issues for Atea for years. One of the reasons the company got into trouble years ago in the first place was actually the Danish segment and how it was run. It bears watching as it seems that the company still has not gotten this under complete control.

Company operational cash flow was so-so – not bad, but not great. It’s typically not that great in 1Q, given the seasonally higher WC requirement, and cash collection was delayed by the coincidence of the Easter holidays. The company’s fundamentals in terms of the net financial situation are better than it has been in a very long time, though.

Atea is now a company that is essentially debt-free. By essentially, I mean that the company has a net debt position of 117M NOK, which means a net debt ratio of 0.1x to EBITDA and the ability for the company to pay down what debt it has with less than 30% of the quarterly current EBITDA. This is to be put into context to a loan covenant maximum of 2.5x, with a debt availability of 4.875B NOK.

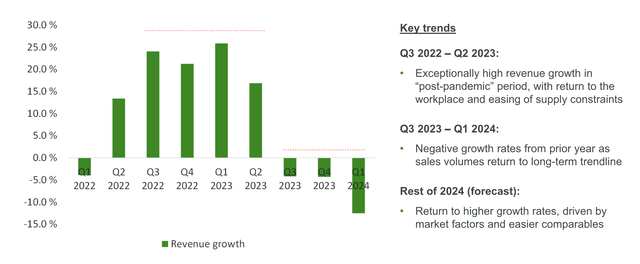

The company is coming out of the comparative periods where sales revenues were incredibly high due to post-pandemic purchases, with easing supply constraints and the like. This is still putting down the comparative YoY revenue growths, so it’s not all due to Atea itself – it’s also comps.

Atea IR (Atea IR)

The company is also struggling to bring Denmark into shape and has had a number of fairly recent wins, including servers and storage for central government ministries, regions, and municipalities, as well as PCs and accessories. These two contracts should provide some cushioning for the segment going forward, and these were wins that were both announced in 1Q of 2024, so they haven’t been taken into consideration before this.

The recent development in defense spending and public spending is also a significant advantage for Atea going forward because the company is a key IT supplier for all Nordic defense departments – not just in Norway but in all of Scandinavia and the Baltics as well – and all of these nations have announced significant investments into defense spending.

Atea will see advantages from such spending trends, to be sure.

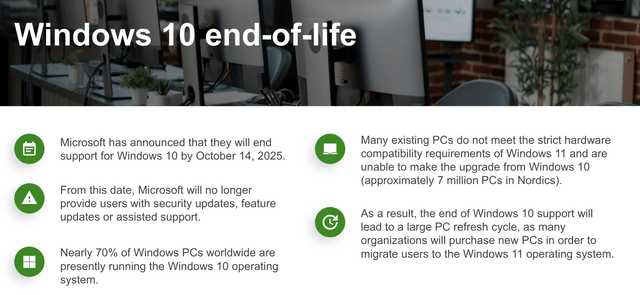

There’s also something simple as the Windows 10 end-of-life announcement.

Atea IR (Atea IR)

All of this taken into account means that I consider it likely for Atea to improve its earnings and revenue trends over the coming few years. While I do not think that Atea will reach necessarily pandemic levels of growth all that quickly, all of these trends will certainly act as cushioning for a very attractive future potential for this company.

The company also has 10 consecutive years of profitability behind it, proving clearly that it’s not a company that’s going “the wrong” way here.

There are really only a few drawbacks to Atea at this time. If you accept the company’s long-term premium for the reasons I describe above, the company could even be a solid “BUY” Here, but I caution against going “too high” here since the company has not achieved any sort of notable solid long-term premium since before 2019 – and I don’t consider the 2020-2021 period to count here for exactly the pandemic trends that came out of it.

Risks to Atea were one of a clear operational nature – I don’t consider that to be the case any longer with the significant tailwinds that we have here. The biggest risk I continue to see relevant to this company that I see would be the fact that the company really does not control much of the products that it sells and acts merely as a middleman.

Atea’s role in the chain is more that of a reseller of software and hardware. This, technically, opens it up to competition if another player were to make a market move – but viewing it so simplistically also takes away from the fact that Atea has decades of customer relationships and procurement experience under its belt.

So, all in all, I tend to view Atea as fairly positive here, provided that the valuation makes sense.

Valuation for Atea – There’s upside to be had here at the right price

As I said, I don’t think Atea should be as premiumized as some analysts or as some market trends are implying it should be. The 5-year P/E average is 22x P/E and above – and that includes all those years of pandemic sales we spoke about. So I don’t view this as a good target to work from for that reason, but also due to other reasons.

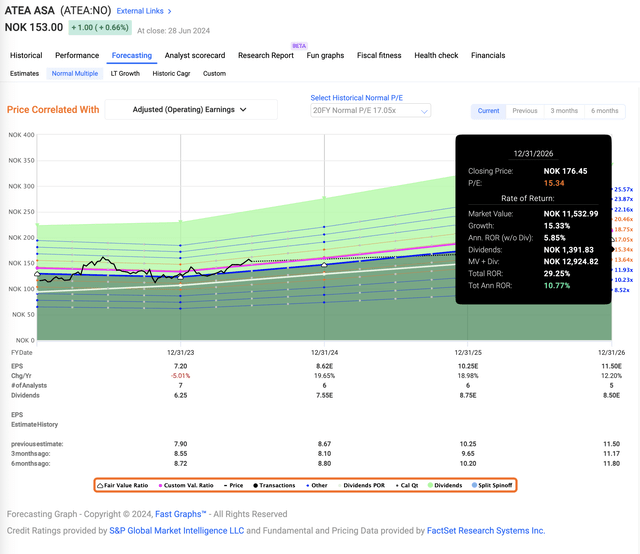

Here we also find the simple fact that Atea, when all is said and done, misses targets negatively over the past 10 years by more than 10-20% (Paywalled FAST Graphs Link). So either the company sets lofty targets that analysts adopt and that the company can’t then achieve, or analysts have a tendency towards exuberance for this company.

Either way or either case, I would use the most conservative 20-year average P/E I can find to estimate for Atea here. That also has to do with the fact that when I last invested in Atea, I did so at a very high yield above 6-7%. That yield is now 4.6%.

The problem with the valuation here is that there is zero room for error. If we use the 20-year average of about 17x P/E – which for a software and hardware reseller and IT consultant with less than 10% net margin is still high – then we have barely a 15% annualized upside here. But the company is also at a current share price of 153 NOK.

My last share price target for Atea was 130 NOK. I am, due to increases in defense spending and aforementioned trends, raising this target to 140 NOK, but this still leaves us shy of the current estimates. At a 15-16x P/E, this company does not generate alpha, meaning 15% annualized or above.

Atea Upside FAST Graphs (Atea Upside FAST Graphs)

And I would want that 15% annualized upside to around 15x-17x P/E consistently before I go in an invest more here. This is not a company I am rotating or selling off – not in any way – but it’s also not a company where I am keen on immediately investing more money at this valuation – especially, as you can see, the company actually has a fair bit of volatility to its share price. It’s not an unreasonable expectation here, for the company to go down to 15-16x P/E here, at which point we could easily get over 5% yield for Atea and which would improve the return profile.

As things stand, I would wait for this rather than investing more here.

Here is my current thesis for 2024E.

Thesis

- Atea is one of the market-leading IT companies in the Nordics, not in their own software, but in selling other companies’ hardware and software and servicing this. The company’s market share and exposure to multiple geographies and currencies make this an attractive play if you’re interested in higher-yielding IT with Scandinavian organizations as their backbone.

- At the right valuation, this company has the real potential for 50-150% RoR while paying a 5-6% yield, as I have invested in Atea in the past. For the time being, however, it’s coming out of what I view as being somewhat overvalued.

- I rotated most of my shares in the past, and I give Atea a conservative PT based on a relatively low EBIT margin and a volatile history despite a strong forecast, and would buy below 140 NOK/share. The company share price is currently 153 NOK. This makes the company a “HOLD” here, and I am changing my targets.

Remember, I’m all about:

1. Buying undervalued – even if that undervaluation is slight, and not mind-numbingly massive – companies at a discount, allowing them to normalize over time and harvesting capital gains and dividends in the meantime.

2. If the company goes well beyond normalization and goes into overvaluation, I harvest gains and rotate my position into other undervalued stocks, repeating #1.

3. If the company doesn’t go into overvaluation, but hovers within a fair value, or goes back down to undervaluation, I buy more as time allows.

4. I reinvest proceeds from dividends, savings from work, or other cash inflows as specified in #1.

Here are my criteria and how the company fulfills them (italicized).

- This company is overall qualitative.

- This company is fundamentally safe/conservative & well-run.

- This company pays a well-covered dividend.

- This company is currently cheap.

- This company has a realistic upside based on earnings growth or multiple expansion/reversion.

This means that the company fulfills all but two of my criteria, making it relatively clear why I moved to a “HOLD” here.

Thank you for reading.

Editor’s Note: This article discusses one or more securities that do not trade on a major U.S. exchange. Please be aware of the risks associated with these stocks.

Read the full article here

")

")

")

")