Q3 2024 Earnings Call Transcript")

")

")

Investment thesis

My previous bearish thesis about Enphase Energy (NASDAQ:ENPH) aged well as the stock tanked by 14% over the last three months. The environment is not improving for Enphase as interest rates remain unchanged and only one rate cut is expected in 2024. Revenue continues dropping rapidly, and inventory levels are compounding like a snowball. There are significant risks of Enphase’s supply chain disruptions due to potentially unfavorable developments in the U.S.-China relationships. My valuation analysis suggests that ENPH is substantially overvalued even when I incorporate aggressive revenue and profitability assumptions. All in all, Enphase Energy’s stock is now a “Strong Sell” in my opinion.

Recent developments

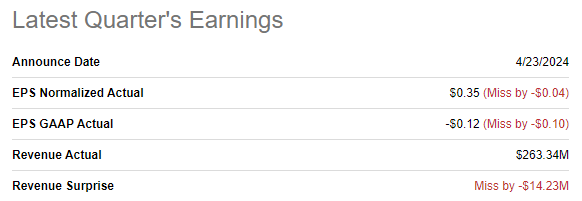

The latest quarterly earnings were released on April 23, when Enphase missed both revenue and EPS consensus estimates. Revenue decrease pace accelerated in Q1 2024 with a 63.7% YoY drop. The adjusted EPS shrank from $1.37 to $0.35 as a result of the massive revenue decline.

Seeking Alpha

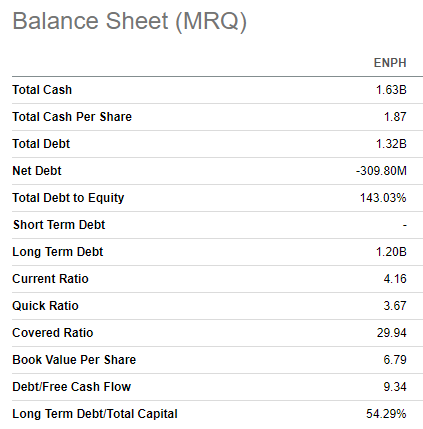

The company’s gross margin did not decrease much despite revenue growth, by around one percentage point. Enphase did not cut R&D or SG&A much, which made the operating negative at -10% in Q1. In absolute terms, the company’s operating loss was $27 million, which is immaterial compared to the $1.63 billion cash position as of the end of the quarter. Therefore, ENPH’s financial position is definitely strong enough to weather the storm.

Seeking Alpha

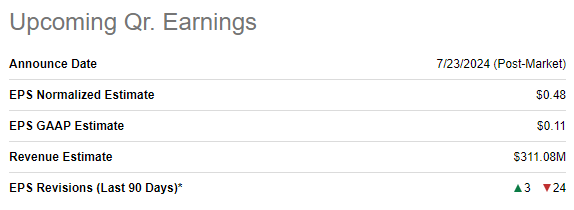

The upcoming earnings release is scheduled for July 23. Consensus estimates project Q2 revenue to be $311 million, 56% lower compared to the same quarter last year. The adjusted EPS is expected to decrease faster than revenue by declining from $1.47 to $0.48. Wall Street analysts are quite skeptical about the upcoming earnings release, with their 24 EPS downgrades over the last 90 days.

Seeking Alpha

Enphase continues navigating through a challenging environment, mostly caused by high interest rates. Since residential solar equipment are not cheap from households’ perspective, sales significantly depend on interest rates. Low interest rates make households more confident in their purchasing power, which increases chances of “investing” in a solar system. From the perspective of the Fed’s monetary policy, Enphase is likely poised to continue suffering from it. The latest information suggests that the Fed will make only one rate cut in 2024. With such a slow pace of cutting rates, there is notable probability that we might see high rates through 2025 as the labor market is still strong and inflation heading down.

The current global geopolitical situation is not favorable for Enphase’s investors as well. While the company’s revenue is mostly generated in North America and Europe, there is significant dependence on China from the production perspective. According to the company’s latest 10-K report, lithium-ion phosphate battery cells for Enphase’s storage products are supplied solely via two suppliers in China. Therefore, the uncertainty around the U.S. and China relationships means that there are risks of Enphase’s supply chain being disrupted by adverse geopolitical developments.

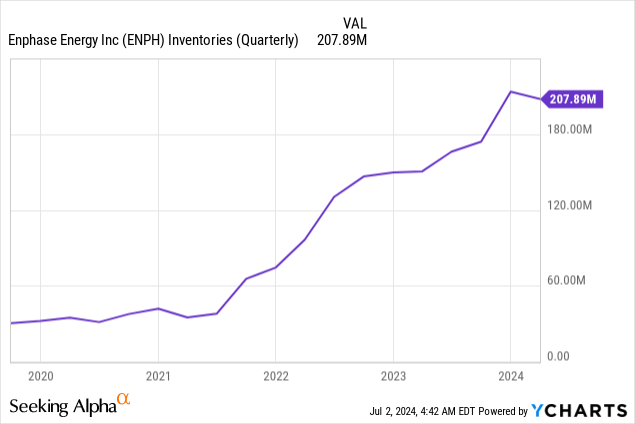

Sky-high inventory level is another big warning sign for investors. Even when the demand rebounds, Enphase will face the need to sell off its high inventory levels prior it returns to its pre-crisis profitability levels. This might mean that the recovery might take a couple more quarters than if inventory levels were lower.

Valuation update

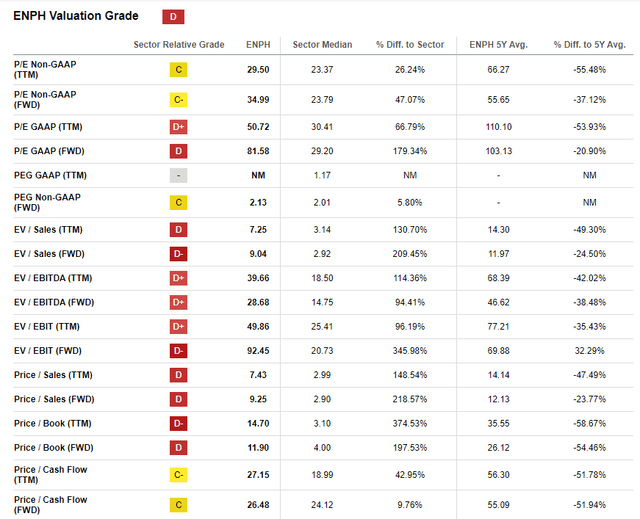

The stock is significantly lagging behind the broader U.S. market, with a 43% share price drop over the last twelve months. YTD performance is also poor, with its -26% for ENPH. Even this deep share price decrease over the last twelve months did not make valuation ratios reasonable. Enphase’s valuation metrics are substantially higher than the sector median. Comparing current multiples with the last five years’ averages is not applicable in this case because Enphase currently does not demonstrate the same revenue growth and profitability expansion as it did before 2023. Therefore, the stock is still overvalued from the perspective of valuation ratios.

Seeking Alpha

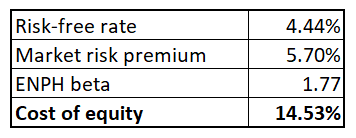

As usual, I am proceeding with the DCF model. ENPH’s dependence on debt is low compared to its market cap, which makes cost of equity the discount rate for my DCF. The company’s cost of equity is 14.53%, all variables for the CAPM formula are easily available on the Internet.

Author’s calculations

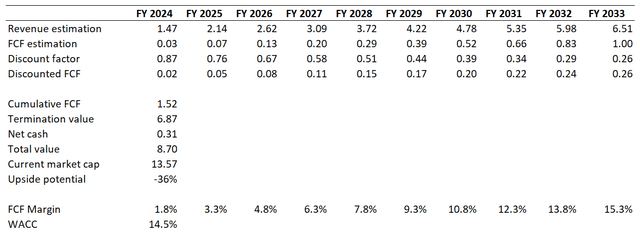

Revenue growth assumption is an 18% CAGR, which is a consensus from Wall Street analysts. Base year FCF margin is 1.8%, which is the trailing twelve months ex-SBC level. With aggressive revenue CAGR incorporating a 1.5 percentage points FCF margin expansion looks sound.

Author’s calculations

According to my DCF simulation, the business’s fair value is $8.7 billion. This is around 36% lower than the current market cap, meaning that ENPH still has the room to tank further.

Risks to my bearish thesis

Governments across the world are interested in acceleration of clean energy adoption, which has been a big secular headwind for Enphase historically. Political decisions from governments are difficult to forecast, which increases uncertainty for my bearish thesis. A sudden announcement that a major economy’s government plans to boost spending on supporting solar energy might send ENPH much higher.

As I explained in “Recent Developments”, Enphase’s financial performance significantly depends on interest rates. The stock market reacts faster than businesses to changes in monetary policy, meaning that ENPH’s share price significantly depends on the sentiment around the Fed’s next moves regarding changes in interest rates. Any hints that the Fed might start cutting rates more aggressively than expected will help the stock as well.

The company’s balance sheet is a fortress, and Enphase is definitely not the only company which valuation deteriorated in the current environment. Having a solid financial position and solar energy assets significantly losing their market values means there is a potential that Enphase might acquire new businesses which will have the potential to bring loads of synergies.

Bottom line

To conclude, Enphase is a “Strong Sell”. The stock is substantially overvalued, even with optimistic 18% revenue CAGR forecast and aggressive profitability expansion. The business will likely navigate through a challenging monetary environment for longer, as the Fed is not in a hurry to start cutting rates. There are significant risks to the supply chain, which can be disrupted if relationships between the U.S. and China get worse. The fortress balance sheet will definitely help to weather the storm, but at the end of this unfavorable cycle, ENPH will also face the problem of sky-high inventories.

Read the full article here

Q3 2024 Earnings Call Transcript")

")