Q3 2024 Earnings Call Transcript")

")

What’s New

As we moved through the month of June, economic data and market action brought more of the same. Data releases continued to be on the softer side in the US, though we are yet to see anything alarming.

Major indices continued to grind higher, led by a smaller number of names, while yields moved modestly lower. Despite the relative calm we saw in markets, we are now at a point where we believe investors should keep a watchful eye on potential shifts in the backdrop.

After all, economic growth continues to slow, market internals appear a bit less healthy than they have been, and political volatility looks set to pick up.

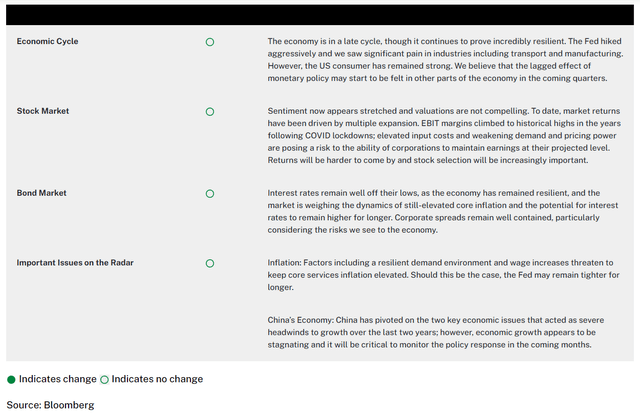

At this point, there can be little question that the US economy is slowing. This shouldn’t be much of a surprise to those paying attention, as growth was always going to have to come off of the elevated levels we saw to close out 2023.

Fiscal support had largely run its course, and the US economy simply cannot sustainably run above its long-term potential growth rate for a prolonged period on its own. The upshot to this is that a slowing economy has helped to bring inflation back toward the Fed’s target.

The risk, though, is that slowing growth can turn into something more nefarious. To that end, we’ve seen the unemployment rate continue to tick up, but nothing looks particularly problematic for now.

Nevertheless, a slowing economy poses a threat to top-line growth, and with the market trading at premium valuations, earnings growth is likely needed to support a continued move higher.

Under the surface, there are also some cautionary signs. The number of stocks above their longer-term moving average has come down, signaling narrower participation in the bull run, while the percentage of stocks making shorter-term lows also jumped during the month. We saw cracks from Nvidia (NVDA), if only for a brief period, and given the elevated level of market concentration we see today, this is certainly worth paying attention to.

Finally, the November general election came firmly into focus at the tail-end of the month, as President Trump and President Biden took to the stage for their first debate. Many spoke loudly in favor of President Trump, and markets reacted accordingly as yields surged to close the month.

To be clear, we are still early in the process and a lot can change. The key takeaway should be that as we move into the summer, we should expect political noise to increase and bring volatility with it.

Our Perspective

Against this backdrop, markets continue to look very expensive in the US. We’ve been talking about several industries being priced to perfection, and we continue to believe that this is the case. Such an environment continues to necessitate balancing risk and reward in portfolios.

We believe that our active approach to investment management will continue to allow us to uncover investment opportunities, while largely avoiding parts of the market where we see elevated risks moving forward.

We have been adamant that a soft landing is unlikely as we progress through the economic cycle, though we have to admit that the probability of such an outcome has risen over the last several quarters.

Historical evidence suggests that the Fed has never brought inflation down from the levels we’ve seen without causing significant economic hardship, yet it’s also important to acknowledge the amount of fiscal support that existed in the economy this time around as the Fed was hiking.

As we move closer to the beginning of a new easing cycle, the question is just how aggressive it will be. We maintain that any deep cuts are likely to be in response to an adverse economic scenario, which we certainly still believe is a possibility.

Earnings would likely be hit hard by any economic slowdown that drove the Fed to cut. However, the continued resiliency of the US economy and the downward trend in inflation has increased the odds of a more benign outcome.

Given the varied risks we see in the market today, we are placing an emphasis on risk management and have adopted a modestly defensive position strategy in our core portfolios.

Our View

Original Post

Editor’s Note: The summary bullets for this article were chosen by Seeking Alpha editors.

Read the full article here

Q3 2024 Earnings Call Transcript")

")