")

")

")

")

Sun Country Airlines Holdings, Inc. (NASDAQ:SNCY) reported its Q1 2024 earnings on May 7 and the results were not well received by the market. Sun Country Airlines stock lost 12.4% of its market cap despite posting adjusted operating margins of 18.2%. In this report, I will be unpacking the results to investigate what drove the share price decline and perform a stock price assessment.

Sun Country Airlines: Not Leveraging Business Model Strength

Sun Country Airlines

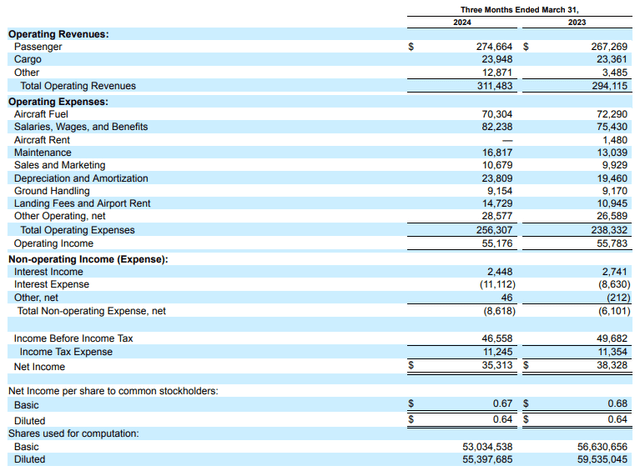

Looking at the revenue line, we see that revenues of $311.5 million were up 6%, missing analyst estimates by $7.34 million. Other revenues were up $9.5 million and this revenue increase was almost exclusively driven by seven aircraft that Sun Country Airlines has acquired including their leases to strengthen the fleet once the leases end. Cargo revenues were more or less stable and that’s a stark contrast with the cargo operations of other airlines. Sun Country Airlines operates on behalf of other companies with minimum guarantees and rate escalations contracted. The rate escalation was offset by lower departures and block hours flown.

The passenger revenues increased 2.8%. Charter revenues grew by 2.4% where 6% higher block hour revenues were offset by 3% fewer block hours and departures. The most disappointing part of the business likely was the performance in scheduled services. Much to my displeasure Sun Country Airlines elected to focus on scheduled services rather than its cargo and charter operations, which in my view provide better cost and top line shielding.

Scheduled service revenues declined by 8% despite 16% capacity being added to the system. Base fares dropped 20%, partially offset by a 9% growth in ancillary revenues resulting in an overall fare decline of 11%. So, what we’re seeing is that Sun Country Airlines had to lower fares to fill its airplanes, and it was not quite successful as load factors also dropped from 88.1% to 87.4%. That’s a big pain point for Sun Country Airlines. The airline bet on scheduled services, and it has not been a good bet. What makes matters worse is that for Sun Country Airlines Q1 revenues benefited from an “Easter in March” bump, but the overall performance in March bookings was below expectations, and for Sun Country Airlines Q1 tends to be stronger than Q2. So, sequentially, we will see unit revenues dip even further. And given that the first quarter was underwhelming it does not send a joyful message for Q2. What makes Sun Country Airlines a different breed of airline is its combination of charter, cargo and scheduled services where they can shift capacity from less protected revenue segments such as scheduled services into for example charters. However, they overestimated the scheduled services demand and as a result did not leverage their business model strength.

Total cost grew 7.5% which is favorable when considering the 16% capacity expansion resulting in a 5.4% reduction in unit costs. Excluding fuel and cargo-related costs, the unit costs would be less than a percent lower. If there’s anything that could be viewed as a positive it would be the lower overall unit costs, but that was driven by the lower fuel gallon prices.

In my view, by not leveraging its business segments efficiently, Sun Country Airlines saw its margin fall from 19% to 17.7%, missing earnings estimates by $0.04.

What Will Q2 2024 Earnings Look Like For Sun Country Airlines?

For the second quarter, total revenues are expected to be between $255 million and $265 million with block hour growth of 8% to 11%. The company expects margins between 4% to 7% showing the stark contrast between the seasonally strong Q1 and Q2. The company noted that its business is built for resiliency and can allocate capacity between different lines of business to maximize profits and earnings volatility. For Q2, however, the bulk of the capacity is already committed and there’s not much they can change about that now, so capacity allocation is a story for the second half of the year. I find it terribly painful for Sun Country Airlines that they mention the ability to shift capacity between their lines of business as a factor of resilience while that’s the one thing they failed to do in Q1, and it’s also going to cost them a good performance in Q2.

Sun Country Airlines Stock Flashes Strong Buy Signs

The Aerospace Forum

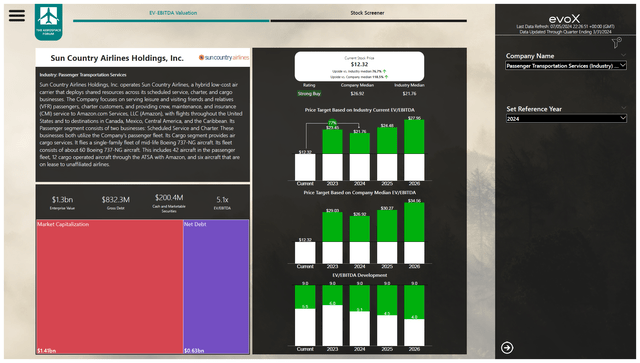

While I’m extremely critical of the capacity deployment by management, I still believe that Sun Country Airlines indeed does have a resilient business model that once leveraged correctly can provide significant upside. Using the more conservative median for the peer group to value Sun Country Airlines stock, we see a 77% upside to $21.75, and even if we would discount any upside by 50% due to execution risk by management, there would still be a compelling 38% upside. So, I believe the recent reduction in the stock price has created an even more compelling investment opportunity.

Conclusion: SNCY Stock Is A Strong Buy Despite Horrible Execution

While I most definitely am not pleased with the execution of management during Q1, and that’s likely also going to spill over to Q2 with some prospects of capacity redeployment from Q3 onwards, I believe the current stock price does not accurately reflect the resilient business model consisting of scheduled services and charters and cargo opportunities which provide some cost protection. As a result and in combination with the significant share price decline, I’m upgrading the stock to a strong buy with a 2024 price target of $21.75 down from my previous target of $22.29.

Read the full article here

")

")

")

")