Q3 2024 Earnings Call Transcript")

")

")

Dear readers/followers,

Sampo (OTCPK:SAXPF) (OTCPK:SAXPY) is one of those companies I write about in regular intervals as the quarterly reports and updates come in. It has gone from being a bank holding company/insurance business mix to a pure-play insurance company that unfortunately has underperformed the S&P500 by quite a bit both over the short-term and the long-term.

Thus, I’m fairly happy that I have been “out” of the investment for some time. Since my last article, which you can find here, the company has generated negative ROR during a time when other insurance companies in Europe have done rather well.

This is despite the company’s favorable pricing trends and its focus on improving underwriting quality. In this article, I mean to update on the business at this time and look at what sort of upside we have here.

In one of my previous articles, the company had dropped 15% in less than 4 months – so continued negative trends over the past 4 months are not surprising to me. I did not change my “HOLD” rating, and indeed this was the right choice – and I continue to have a “HOLD” rating on the company here.

Sampo – Plenty of qualitative upside from Insurance – but the right price is paramount

The arguments that exist against an investment in Finnish company Sampo are not based on poor fundamentals or company quality as such. Sampo has spent a number of years streamlining and improving its operations to levels where it can be considered a leader in the European, and specifically the Scandinavian insurance space.

Instead, we’re talking about pricing trends. Some analysts would argue that Sampo’s superb combined ratio (because it really is superb by any international measure) by far justifies its high valuation – and higher – and that the company can, in fact, be bought with a conservative upside here.

I would say that even as of the latest results, this is still an erroneous assumption – for the time being. As of today, the company’s native share price is still over €40/share. I consider this to be a material difference from any sort of conservative valuation.

While stability is certainly worth something, the overall increased interest rates mean that the risk-free rate is still above 4%, which means that any investment that only yields 3-4% has to justify itself not only on yield but on different sorts of upside – typically growth.

In my last article, I did increase my share price target on Sampo – I am not doing this as of this article because I do not believe the latest set of results justify this.

1Q24 is in – and the company showed a very decent performance but was hampered by very severe weather trends. All Sampo business areas performed well, with underlying trends remaining positive, stable-to-easing claims inflation, and good progress on the company ambitions with good online sales and growth in non-motor insurance. Motor insurance is one of the company’s biggest exposures.

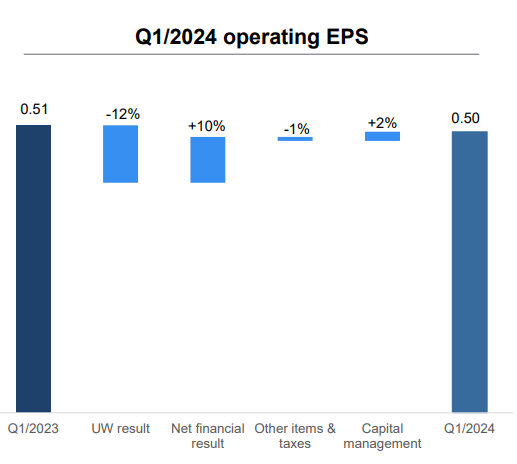

Also, on the fundamental side, investment yields are up, and we’ll see here that the risk-free rate for the company’s own investments is now at a very good level (so yours shouldn’t be worse in any way). However, the company’s operating EPS, a core KPI, was still at the following level.

Sampo IR

So despite all of this positivity, it’s down for the YoY period. You can see what sort of impacts these weather effects can have – and the underwriting results are one of the most challenged in terms of winter conditions since 2010. We’ve had a very cold winter this year, with temperatures dropping to below -40 to -48 where I currently am (which, granted, is far north, but still).

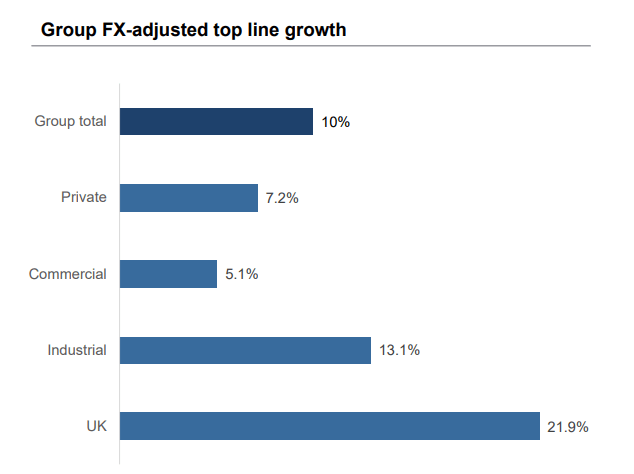

On the bullish side, we can focus on significant growth – also UK growth coming in at very good numbers.

Sampo IR

Generally speaking, I believe that all insurance companies need to prepare, at least those in this field, for more severe weather and meteorological trends – which will hurt the bottom line, and perhaps take away some of the stability that even Sampo has had on a historical basis.

The growth you see above was driven by personal and P&C insurance in private, with good retention, and decent growth in commercial. Industrial is good due to Jan 1 renewals in this period, which saw good price increases, and in the UK the growth came from an increase in live customer policies. So, all things said here, Sampo is going well.

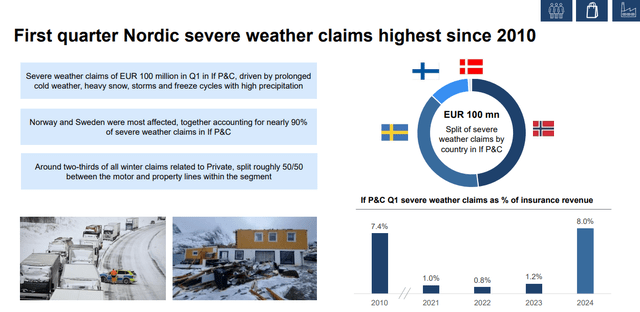

A quick snapshot of the winter here.

Sampo IR

Just that you see how “bad” things were here, doesn’t change the fundamental thesis on the company, but it does show you why I don’t go head-over-heels into this investment just because it’s “supposedly” cheap and a “BUY”, which it has been for many investors and analysts for some time.

The overall geographic trends in P&C operations for Sampo are broadly stable, with claims inflation at 4-5%, but frequency slightly rising and weather effects becoming more common. However, the Nordic P&C market is disciplined, with good dynamics that are mostly unchanged. Pricing increases ahead of inflation and retention remains high. The UK remains a growth area, with home policies up 27%. All of this comes to 10% group topline growth and an 89% claims inflation in the Nordic area.

Sampo continues to enjoy some leading combined ratios, going down as low as 83% (lower or better), and what I also like seeing is accelerated growth in the private insurance sector, driven by non-motor policies. Digital sales, which are more profitable, are also up.

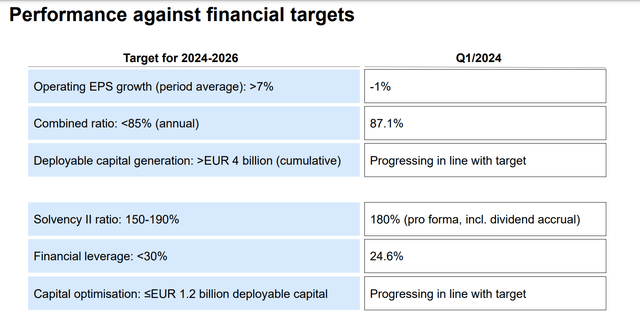

From the investment return perspective, returns for the company are now above 4% on a mark-to-market basis. From a fundamental perspective, when it comes to solvency and debt, Sampo continues to run high solvency at 180%, and leverage at 26.8%, which continues to be below the 30% target mark for the company.

Here are the current targets for the 1Q year, which are expected, as you can see, to come in broadly flat, and aren’t expected to massively improve above expectations either.

Sampo IR

For this set of results, I do not see a reason for me to raise the bar for the company’s price target, or for the expectations on a forward basis.

Here is the current valuation thesis for the company.

Valuation for Sampo – It’s not yet massively attractive, but there’s a possibility for a “BUY” here

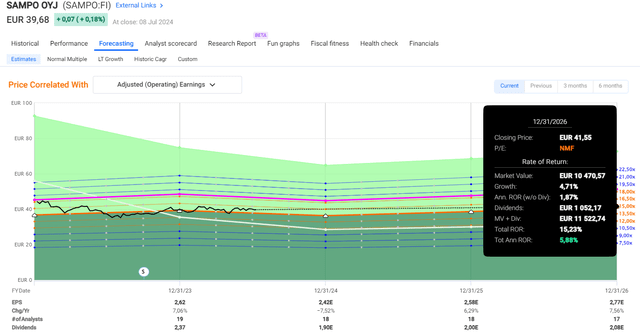

Sampo is expected to generate flat or slightly negative earnings here – according to some analysts, as much of a drop as 8% year-over-year (FAST Graphs Paywalled Link). Even with the expectation of around 6-7% per year in the 2 years after, this comes to a potential for flat development for this company.

And Sampo, which currently trades at almost 16x P/E, isn’t exactly attractive at that point when we take peer averages into account. You can find insurance companies with higher yields and close-to-similar fundamentals trading below 7x P/E. Lincoln (LNC) is one such, that I invest heavily into.

Sampo’s dividend yield is 4.5% (ignore the ADR implied yield). That means it’s only 0.5% above the company’s own mark-to-market investment portfolio yield. It’s not that attractive for an insurance business. When you combine this with the fact that 14-15x P/E is more or less the average for the past few years, you find yourself forecasting to an implied RoR of less than 6% per year.

Sampo Upside (FAST Graphs)

In fact, the 12-year average is closer to 13.5x – if we forecast to that longer-term average, we get almost negative RoR, that’s positive at 0.77% per year only because of the yield. If that wasn’t there, it would be negative at a non-trivial amount.

Historical levels are certainly not gospel in any way – but they do come with some relevance to me because I in part to model my future estimates on how the company has performed on a normalized historical basis.

The company remains at a very low level of debt, as evidenced by the A rating that the company still has, and at the sub-28% long-term debt/capital it has.

But still, 15% annualized RoR, which tends to be the minimum level I am looking for, demands us to forecast Sampo at over 22x P/E. That is a level where I never forecast any insurance company, no matter how good it is – at least not yet. As you see, I may be harping around quite a bit on normalized P/E ratios here, but the book ratios show a similar imbalance to the historical numbers – as do other KPIs that I consider relevant for Sampo. Nothing really shows a good upside here, and I cannot understand analysts that consider this one a “BUY” – and they exist.

The main question for you should be if you believe that Sampo’s divestment of Nordea has been a risk reduction and a value-add in terms of what the company has done since then.

I still do not believe this to be the case.

S&P Global analysts come to an average PT of around €43/share. This is from a target range starting at €38/share and going to €49, which is an insanely high price for this company given what growth is being expected here. Even that €43/share average PT is at least 10% too high, as I see it, for what the company is able to perform here.

At €38/share, we don’t exactly have a massive upside in any way, but we have a good enough upside to where I can see at least a double-digit upside, and above a 5% yield. That is the minimum that I would want for the company here.

Based on this, I give you my updated thesis for July 2024 for Sampo.

Thesis

- Sampo is one of the better insurance companies in all of Europe. Together with Allianz, Munich Re, and AXA, I consider them the 4 prime investments in multi-line and reinsurance. Whenever one of them is cheap, that is a time to “BUY” the company for me.

- Sampo, at this particular time, is not a cheap company per se. Trading at almost 16x P/E, both on a European and International comparison, it’s an expensive insurance company for what it offers, despite its superb management and A-rated credit safety as well as very low leverage and over €20B worth of market cap.

- I would currently view Sampo as a “HOLD” here. Once the company hits below €38/share, I would consider it a “BUY” again. This is a raising of my PT, but still nowhere near the current price of €39.8.

Remember, I’m all about :

1. Buying undervalued – even if that undervaluation is slight, and not mind-numbingly massive – companies at a discount, allowing them to normalize over time and harvesting capital gains and dividends in the meantime.

2. If the company goes well beyond normalization and goes into overvaluation, I harvest gains and rotate my position into other undervalued stocks, repeating #1.

3. If the company doesn’t go into overvaluation, but hovers within a fair value, or goes back down to undervaluation, I buy more as time allows.

4. I reinvest proceeds from dividends, savings from work, or other cash inflows as specified in #1.

Here are my criteria and how the company fulfills them (italicized).

- This company is overall qualitative.

- This company is fundamentally safe/conservative & well-run.

- This company pays a well-covered dividend.

- This company is currently cheap.

- This company has a realistic upside based on earnings growth or multiple expansion/reversion.

Because it is neither cheap nor has a solid upside potential, I view this as not being an interesting or valid investment at this time based on my goals. I give the company a “HOLD”.

Editor’s Note: This article discusses one or more securities that do not trade on a major U.S. exchange. Please be aware of the risks associated with these stocks.

Read the full article here

Q3 2024 Earnings Call Transcript")

")