Q2 2024 Earnings Call Transcript")

")

Recurrent MLP & Infrastructure Fund (MUTF:RMLPX) is an open-end equity mutual fund that was launched to eliminate some of the risks involved in holding individual names in the midstream space. One of the biggest values this portfolio brings to the table is that there are no K-1s and is taxed with a standard 1099. This means that you, the investor, don’t have to file your taxes late.

RMLPX was formed in 2017 with their own valuation spin in mind for how they include and weigh investments. As opposed to only using the standard EV/EBITDA multiple heavily used across the energy industry, the firm uses EV/IC (invested capital) and heavily focuses on returns on invested capital (ROIC).

Corporate Reports

ROIC is taken by dividing net operating income after tax (NOPAT) by the book value of invested capital.

ROIC Formula

What this ratio implies is the firm’s ability to generate a profit with capital investments as a basis. It essentially measures how efficiently the firm puts capital to work.

The managers also heavily utilize ROIC/WACC (weighted average cost of capital) in their analysis for company inclusion. What this metric looks at is the firm’s total cost of capital, between equity, debt, and preferreds, and is further divided into ROIC. In short, this compares capital efficiency to cost of capital.

The firm is very diligent in their name selection; each company must pass through their rigorous screening before being considered for further analysis and inclusion. With a portfolio concentrated in 27 securities, this level of rigor is required given the volatility of the oil and gas market.

RMLPX Strategy

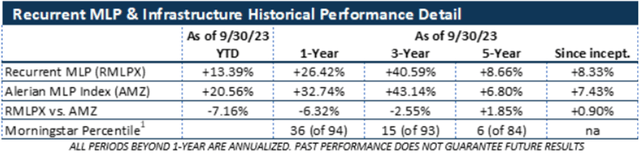

The portfolio is benchmarked to the Alerian MLP Index (AMJ) and has beat the index since inception.

RMLPX Benchmark

The portfolio has grown significantly since inception, reaching $677mm in net assets. Though this is smaller than the more actively traded ETFs out there, the portfolio is meant to be held and not necessarily actively managed as a position. The portfolio itself has a 10% turnover ratio, meaning that the portfolio managers aren’t frequently entering and exiting positions.

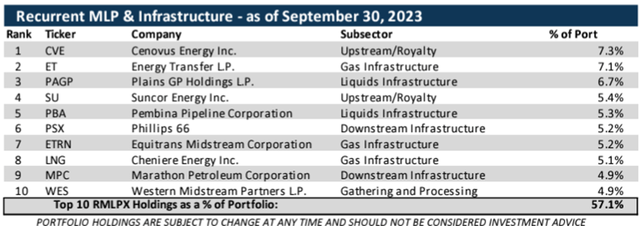

RMLPX Top Holdings

The top names in the portfolio make up 56% of the total weightings; however, unlike the previously covered URNM, RMPLX doesn’t concentrate heavily on the top few positions and has a more balanced portfolio throughout all positions. The top 10 positions hold a few names that I have covered, including Energy Transfer (ET). The top holding is Cenovus Energy (CVE).

Company Logo

Cenovus Energy is an Alberta, Canada-based IOC (integrated oil company) with a market cap of $41b, about 1/3rd of ConocoPhillips. Cenovus focuses their upstream operations in Canada’s oil sands and heavy oil as well as conventional drilling. The firm also owns or has joint interests in a number of refineries across the US Midwest and Rust Belt, and in Canada. Using figures from Seeking Alpha, the firm generated $9,985mm in EBITDA using TTM q3’23 figures for a margin of 19%. The firm is valued at 5x EV/EBITDA, significantly below its US-based peers and the industry average of 5.53x. Cenovus issues a dividend that currently yields 2.38%, putting it at the lower end when compared to its US IOC peers.

Company Logo

Skipping over Energy Transfer, which I have already extensively covered, we move onto Plains (PAGP). As opposed to the limited partnership units (PAA), the firm holds the general partnership units. For the most part, the two-unit classes trade in tandem and don’t offer much perceived difference for the typical investor.

TradingView

Plains is a midstream energy infrastructure firm based in Houston, Texas, with a market cap of $24b. The firm generated $1.45b in free cash flow for 2023 and trades at a FCF yield of 10% (considering PAA & PAGP). Plains manages long-haul intrastate and interstate pipelines for the transportation of oil, natural gas, and natural gas liquids. Their long-haul pipeline cuts through the central region of the US up to Canada in the Alberta region. 75% of their tariff volumes derive from the Permian Basin at 6MMbbl/d.

PAGP Asset Portfolio

Overall, I believe holding this fund will provide some much-needed income for any investor looking to retain the value of their portfolio in a turbulent economy. As discussed in my article entitled Short-term Bear, Long-term Bull, (XLE) US production has peaked in 2023 at 13,236Mbbl/d. As domestic producers consolidate, oil and gas production is going to be more heavily focused in key basins, such as the Permian Basin and DJ Basin for short-cycle and offshore for long-cycle production. As the world’s demand for hydrocarbons continues to climb, the necessity to produce and transport these fuels becomes all that much more valuable. The downside to the upstream side of the business is that oil prices are volatile; thus, company stocks will reflect this volatility. For those looking to minimize risk but retain exposure to the industry, midstream is oftentimes your best bet.

Fund Details

Management fees are standard for a managed mutual fund at 90bps with a total expense of 1.15%. Though this appears to be a monster chunk of change, bear in mind the standard advisory fee is 1% before portfolio expense, meaning that if you were to go to a financial advisor to manage your portfolio, you’d be paying them 1% of your assets before paying the additional fees associated with the mutual funds and ETFs held in the portfolio. Because RMLPX is a managed fund, the ideal method of ownership is to hold and forget about it until you’re ready to completely exit the market.

There are two ways to invest in this fund. You can either invest in the Class I shares, RMLPX, or directly with Recurrent in their SMA business (separately management accounts). The minimum initial investment for the Class I shares is $2,500.

Lastly, the fund pays out a robust distribution which yields 6.49%. Considering both the distribution and long-term trajectory of the midstream industry, I believe RMLPX will make a great addition to a balanced portfolio strategy.

Read the full article here

Q2 2024 Earnings Call Transcript")

")