")

")

The streamers have been getting pummeled after a massive Covid run up. Now, growth is slowing and the market is saturated. There needs to be consolidation for a recovery to really take hold.

Value In Streamers

I have long been a follower of the workings of the entertainment industry. It started when I was a teen with some thoughts of being a writer in Hollywood. After college in the 1990s, I got into finance and discovered Mario Gabelli.

Gabelli was already famous by the 1990s as a value investor and had done a lot of things. Among them was being a prominent investor in entertainment.

Currently, Gabelli’s firm owns the following streaming companies that we have been following (statistics are what I could find and could be off a bit):

| Company | Shares | Weight |

| Comcast (CMCSA) | 611m | .29% |

| Disney (DIS) | 334k | .32% |

| Netflix (NFLX) | 20k | .10% |

| Paramount A (PARAA)* | 2.8m | .6% |

| Paramount B (PARA)* | 458k | .07% |

| Warner Brothers Discovery (WBD) | 3.1m | .39% |

* Paramount Class A common stock is voting stock, and Class B is non-voting stock. There is no difference between the two classes except for voting rights. There are, however, far more shares of Class B outstanding, so most of the trading occurs in that class.

I mention Gabelli because he and his firm are long-term value investors. So, there is likely value in all of the stocks listed. However, it can take a long time for value to be recognized. Notice none of the positions are very large.

Gabilli owns nearly 900 stocks across multiple portfolio strategies. We do not need to be so spread out to still be diversified. With a few ETFs we can easily be globally diversified. I would point you to this article from the CFA Institute a few years back for a simple understanding of diversification.

What is most important to understand, is that if we have a portfolio of 12-30 stocks on top of a few ETFs, then we are systematically diversified. So, with diversification easy to attain, we then need to manage the rest of our risk and profit potential through security selection. That is, the stocks and ETFs that we pick specifically.

Since all investing is “relative investing,” that is, compared to what we could risk and profit from elsewhere, we want to always be seeking to upgrade our portfolio. The potential downfall is that people tend to overtrade or undertrade.

I would posit this. You should only trade when your thesis on an investment is wrong or the thesis has changed. And, that is where I want to start today in discussing the streaming stocks.

Assessing The Streamers

Originally, I thought that the streamers would right size, do well after a retrenching and then consolidate through M&A. However, that process is taking longer and has proven to be more expensive than originally thought.

My thesis on Paramount broke and Buffett already bailed. I’m right behind him.

Further, we have not seen any inclination from “big tech” to bid companies like Warner Brothers or Paramount up in order to beef up their libraries and studio capabilities. There are likely regulatory reasons why that is so, but also, it is big tech’s nature to simply crush their competition. A scorpion is still a scorpion.

Remember always, content is king, and at some point, there’s enough consolidation to drive the industry higher, aka, an industry with fewer players.

Comcast

The company went slow on streaming and has the best finances of the big companies. You’d think CEO Roberts would want to acquire something and Warner has been the rumor. If Comcast does acquire Warner, they could bundle all of the Peacock and Universal content under Warner’s Max making it a “must have” super app.

Remember, Comcast just got paid off by Disney for their share of Hulu, so I do expect them to acquire something. Paramount has also been rumored, though not as strongly due to regulatory issues.

The risk here is that the market just doesn’t like whatever Comcast does. Indeed, the market has a hard time getting excited about Comcast at all. I do want to buy it, but I want it at a deep discount as growth will never be “lock down” big ever again. The future of streaming growth is international expansion and that will take a generation.

Disney

Disney is a big ship to turn, but they do have great assets, including very undervalued real estate. I think Iger is doing the right things, but, again, it’s a big ship.

Disney needs to keep themselves together, except for some small non-core divestitures. ESPN is worth a ton. So is ABC. Hulu is becoming a “must have” super app. Their studios are gold. Their content library is immense and profitable. The Parks print money.

The problem for them, like everyone else, is that there is just too much content right now and there needs to be consolidation. Disney does not have to buy anything, they just have to wait for Paramount and Warner to be acquired very preferably buy other media companies reducing the amount of content and spend, as well as, concentrating ad revenues to fewer players.

Private equity wants to break the company up because they see the underlying value. Their sum of the parts valuation offers them a fast gain versus the work of bringing the revenues and profits back up to pre-Covid levels.

I am looking for the final value opportunity to buy Disney. I think it is coming.

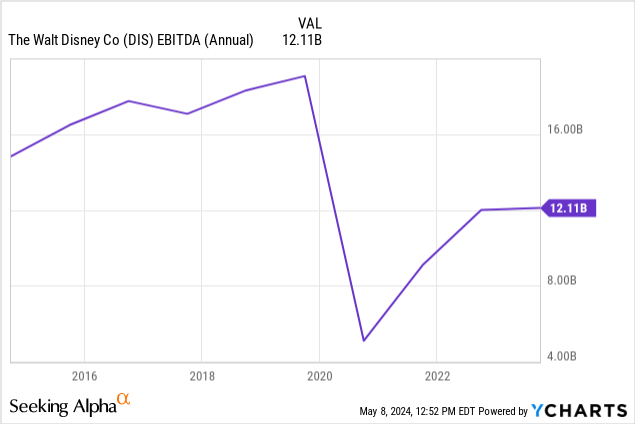

By my estimation, the “bottom fishing” price on Disney is somewhere around $160 billion dollars of market cap or a share price in the $80s. That comes from a fairly standard 10x ratio on EBITDA.

I am basing my valuation on Disney reclaiming the $16 billion per year in EBITDA in the next few years. Shorts can argue that the bottom fishing is around $120 billion in market cap and say the stock should possibly be in the $60s.

However, there is more than EBITDA. Private equity sniffing around should offer a clue. Very often, private equity firms do a sum of the parts analysis and selling a lot of assets of Disney could generate a big short-term return. Selling those assets might injure or shrink the company permanently though.

My opinion is that Disney is best off shedding only some non-core assets, such as the TV stations, and developing some of their land. The real estate is probably where private equity is looking most.

According to the Reedy Creek Improvement District documents, there is about 1300 acres of developable, but undeveloped land at Disney World. There is about the same that is agricultural. That’s a potential 2600 acres for development.

The rest of Disney’s roughly 25,000 acres is either already developed, cannot be developed due to being wetlands or conservancy, or is slated for resource management. Some might argue there is another 800 to 1700 acres of the roughly 3400 acres set aside for resource management that could be developed.

Ultimately, a good entry price for Disney depends on your assessment of the business reaching around $16 billion per year in EBITDA again and what is the value of the land potential. I would be a buyer in the $80s and a “back up the truck buyer” in the $60s.

Netflix

Netflix has been the best run streamer out there for years and only Apple seems like a direct threat due to its penetration through handset sales. The company grew massively during Covid, but growth has slowed, though Netflix is now very profitable unlike most of their peers. Netflix’s earnings, which count under communications, were excellent and beat handily.

Netflix more than hinted at more difficult growth ahead by announcing they would not be reporting certain new subscriber metrics going forward. The company is moving internationally to provide more local content which comes with capex expenses.

There is a recent Bloomberg documentary that covers what Netflix is doing in Latin America and abroad. It makes clear how hard the road will be. It also shows how big the international market is, demonstrating that billions more people having access to local Netflix content is a big prize.

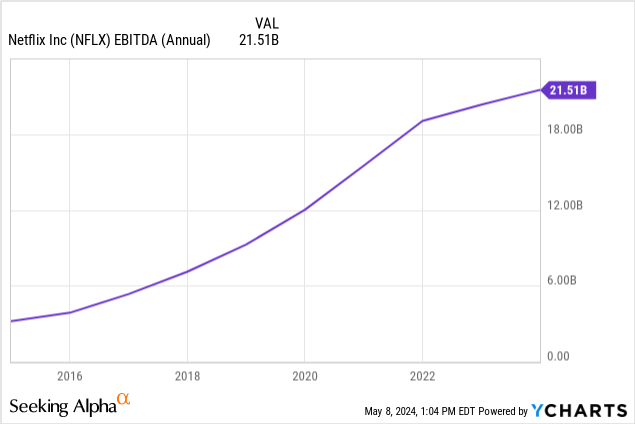

Netflix’s EBITDA is approaching $22 billion, but you can see the curve up has bent showing growth is not as robust. Hence the big international expansion which will not be easy.

Netflix does not have the real estate or ancillary businesses that Disney does. So, with EBITDA around $22 billion and based on their growth rate remaining around the past year’s 10%, Netflix is about fairly valued to slightly overvalued. This is about the price level I sold in late 2021.

Netflix does not have the library Disney has either. I think that is a good reason to pursue Paramount again as was rumored a couple years ago. We’ll see if they enter the bidding.

I think Netflix succeeds longer term as management is truly impressive, but I expect potholes along the way. I need a big stock correction to buy the stock outside ETF exposure. If I could get Netflix for a market cap around $220 billion or 10x EBITDA, corresponding to about $500 per share, I would nibble back in. Any overshoot into the $400s would be a deep value opportunity in my opinion.

Paramount

Shari Redstone is clearly super interested in selling Paramount for the highest price for her voting shares. The rest of us with non-voting shares, well, there have been concerns by major shareholders they will not see value in some deals.

Yes, there will be a takeover. No, it won’t be as high as the value of the assets.

That means the bigger opportunity could be in who acquires Paramount. It’s a pretty good likelihood in my opinion that the market narrators help the traders punish whoever buys Paramount. They’ll talk about the recent history being bad and whatever other mud they can sling against the wall. But, that’ll be the time to buy.

It still makes sense to me that a big streamer that doesn’t have news and only limited sports would want Paramount. That opens up a potential big tech, think Apple (AAPL) or Google (GOOG) (GOOGL), takeover, or Netflix which was a rumor a couple years ago.

I do not think that the Sony (SONY) and Apollo (APO) deal happens as there are restrictions on foreign ownership. And, frankly, I just don’t think Apollo will pay what Paramount is really worth, that’s not the private equity M.O.

Whoever does end up with Paramount gets CBS news and sports, a super deep library and Star Trek. Folks, Star Trek is likely worth as much as Star Wars, and Lucas got a billion dollars for that a decade ago. I’ll be watching who acquires Paramount closely.

Warner Discovery

“David Zaslav, president and CEO of Warner Bros. Discovery, had a 2023 pay package worth $49.7 million, up 26.5% from the year prior, according to the company’s 2024 proxy statement filed Friday. Zaslav’s compensation totaled $39.3 million in 2022, after he received an astonishing $246.6 million (which included $203 million in stock-option grants) in 2021.

For 2023, Zaslav had a base salary of $3 million, stock awards valued at $23.1 million, a cash bonus of $22 million and $1.6 million in other compensation (including $705,182 for personal security services and $767,908 for his personal use of the company’s private jet).” Variety coverage of Warner.

I open with that because I think the executive compensation is hurting Warner’s underlying value. I do not believe that shareholder interests are aligned with current management.

So far, since CEO Zaslav started cutting expenses, he has opted to not release finished movies and shows, and is now about to potentially lose NBA rights. Those NBA rights represent a large portion of the value of TNT.

A well run Warner would be worth a fortune over time in my opinion. Alas, I believe Zaslav alienated many of the best creative minds. The team from HBO, which are among the highest regarded in the world, are now mostly gone. With them, they took the story telling skills that created some of the most iconic shows in TV history.

For certain, the library and franchises are valuable. Batman, Wonder Woman, Superman. The next generation of DC could be epic with the right direction and stories. Harry Potter is still churning out movies on how to tame your beasts. Barbie hangs out with Ken at Warner. Lord of the Rings. Looney Tunes. Game of Thrones… It’s a long list.

Alas, without a change in direction, possibly new management, I think Zaslav can strip even more value from Warner.

I do think there could be a change of direction soon though. Why? Because Zaslav’s next payday has to do with a change of control bonus. According to a Warner proxy statement, Zaslav can receive up to $182 million if the company is sold.

With the company stripped down to the bare bones, selling Warner becomes easier, though the price will be much lower than what shareholders would have received otherwise.

Even though I feel like I can do better with my money on certain micro cap and small-cap investments I have been making, I very well could buy Warner back soon though. Again, why?

Me buying back Warner will be entirely based on the potential for merger arbitrage. If a company like Apple, Alphabet or Comcast buys Warner, it becomes a math equation whether or not to buy the Warner shares. I expect I will be doing that math between very soon and next year.

My Trading Plan

All that considered, I am reducing my streamer holdings to zero because I think I can make more money in other assets, at least for the short-term.

My trading plan is as follows:

- Sell Warner Brothers Discovery (WBD) immediately and take the loss (and tax loss where applicable) on my $14.95 cost basis. I have also had covered calls expire twice along the way for a couple bucks.

- Remember, I do think the company will be acquired, however, I think the best we could do is roughly break even in the teens. You can wait for that, but, it might take a long time.

- Sell Paramount (PARA) using options or an outright sell in the middle teens. My cost basis is $13.72 after a little trim already. I also have had covered calls expire twice for a couple bucks.

- I have $14 May covered calls sold on Paramount that probably just expire. If they do expire, I will likely sell the next mini-rally on buyout speculation.

- Comcast (CMCSA) sell immediately for about a breakeven.

- It’s ok to hold, but, I think there is significant risk that the market narrates dislike for whatever they do whether that is nothing, something or buy Warner or Paramount. If they do have a correction on overemotional market sentiment and trader narratives, I’d likely buy Comcast back for the more secure business on industry consolidation, dividend and future growth internationally.

- Disney (DIS) and I have flirted, but only dated briefly. The turnaround is slow, management has a tough road and private equity still might succeed in tricking enough investors to strip the company. I’d buy in the $80s on the value of the assets and hold my nose at that point.

- Netflix (NFLX) is clearly the best company in the bunch, but, it’s never cheap. So, I could only hope to get it around fair on a broad market correction. I would need a price around $500, but preferably somewhere in the $400s, to buy.

I am going to use the proceeds to invest into the microcaps I discussed recently: 7 Microcaps To Buy Ahead Of Possible Russell 2000 Inclusion

Editor’s Note: This article discusses one or more securities that do not trade on a major U.S. exchange. Please be aware of the risks associated with these stocks.

Read the full article here

")

")

")

")