Q3 2024 Earnings Call Transcript")

")

Summary

At this point, NVIDIA (NASDAQ:NVDA) needs no introduction. We are largely value-oriented investors and tend to stay away from situations with tremendous hype and high-flying valuations. But, alas, we’re biting.

NVIDIA invented the graphics processing unit (“GPU”), hardware originally geared towards serving as the graphics engine in PCs. It has recently extended the application of its GPUs to AI, VR, and high-performance computing (“HPC”). It is also building a platform strategy around connecting its hardware, system software, programmable algorithms, libraries, systems, and services to add value in its key markets (i.e., gaming, automotive, datacenter (“DC”), professional visualization, PC OEMs, and embedded applications). It is undoubtedly the premier AI-driven growth story within the semiconductor space, and, arguably, the broader tech industry.

Despite its dominant position and unprecedented recent financial performance, we feel it prudent to wait this one out, and give the shares a Hold. We see the shares as priced to perfection and the long-term growth potential of critical end-markets (i.e., AI/ML, VR, and automotive) as untested and uncertain. We acknowledge that these markets are almost certainly going to be fast growers for the foreseeable future, but questions remain about the sustainability of the current pace of growth.

NVDA Share Price (1Y) (CapIQ)

Earnings Update

Datacenters

In the FQ1, NVDA posted DC revenue of ~$22.6Bn, +23% QoQ and +427% YoY, exceeding the Street’s expectations. The bulk of this result was attributable to DC compute revenues of ~$19.4Bn, which grew 29% QoQ (478% YoY), while networking revenue of ~$3.2Bn declined 5% QoQ (still +242% YoY).

Management noted that these results were driven by strong demand for its HGX platform due to the aggressive ramp of Training and Inference for LLM and GenAI infrastructure. While all customer segments contributed to the segment’s growth, it was led by Enterprise & Consumer Internet companies with large cloud platforms (n.b., these customers represent ~40% of DC revenues).

NVDA is sampling H200 in Q1 and is on track to begin shipments in Q2. Its supply for H100s grew, though it continues to be constrained for H200. Blackwell is in full production, with its ramp expected to start in Q3, which would enable material revenues to be realized this year from the launch. Overall, demand for H200s and Blackwell remains well ahead of the available supply, a trend that is expected to persist. Following the official debut of Blackwell, management noted that it had lined up availability at >100 OEM and ODM for its launch (n.b., +2x Hopper at the time of this product’s introduction).

Within networking, results were largely driven by InfiniBand, though this business was modestly weaker in the quarter due to the timing of supply, while demand remained well above capacity. Management noted that its initial shipments of the Spectrum-X product line (Ethernet) are expected to open a new market for the company and could be a multi-billion-dollar product within a year. The segment is expected to return to sequential growth in Q2.

Gaming

Gaming revenues (~$2.6Bn) declined ~8% QoQ, but were up 18% YoY, driven by strong consumer demand for the GeForce RTX GPUs. Management noted it sees channel inventory levels normalizing and expects a return to sequential growth for the next quarter. The ProVis segment ($427MM revenue) declined ~8% QoQ, but was up 45% YoY. Desktop workstation GPU sales were weak, though management noted a normalization of channel inventory levels.

Auto & Embedded

Auto & Embedded revenues grew 17% QoQ and 11% YoY, driven by the continued adoption of its self-driving platforms. Management noted increased adoption of its products by BYD, XPENG, GAC’s AION Hyper Nuro, and others for the DRIVE Thor platform, which now features Blackwell GPU architecture. Lucid and IM Motors are also reportedly using DRIVE Orin to power their automated driving systems.

Timing the mass adoption of this technology is incredibly difficult, if not impossible, though we believe NVDA is positioned as a leader in the space and a likely beneficiary if it plays out.

Valuation

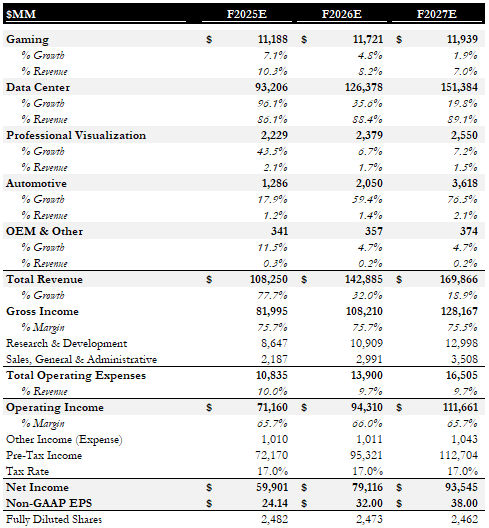

Our base case $115 price target (n.b., ~15% implied downside) is based on a ~36x P/E on our 2026E EPS estimate of $32/share (see table below). We believe NVDA deserves a premium multiple, given its strong competitive positioning for DC growth driven by cloud and AI, gaming, autonomous vehicles, and an expanding ecosystem of products and applications (n.b., NVDA 3-year revenue CAGR through the LTM period is ~61% vs ~26% for AMD).

Our bull case price target of $135 is based on higher 2026E earnings driven by greater DC and AI GPU demand as enterprises find new AI use-cases to justify their spend and continued market share dominance. Other products serving automotive could offer additional support.

Our bear case price target of $82.5 is based on a reduction in earnings growth momentum as customers integrate and digest their significant GPU investments, souring investor sentiment as competitive pressure from AMD mounts.

Base Case EPS Forecast (Empyrean)

Risks & Catalysts

We see 4 key risks facing NVDA:

Premium Valuation

NVDA trades at a premium multiple to its peers. If growth were to slow, its multiple could revert closer to peers, negatively affecting its share price

Early-Stage Growth Cycle & Competitive Threats

NVDA’s future growth is dependent on early-stage tech trends in its DC and automotive businesses. Increasing competition in these applications could slow its growth prospects. For example, at the recent Computex 2024 event, AMD provided an update on its Instinct accelerator roadmap, which contemplates an acceleration of product in the cadence of product introductions to once per year, following NVDA’s move (n.b., previous cycle was 2 years). AMD’s next accelerator, the MI325X, which is expected to become available in Q4 ’24, will have increased memory capacity (n.b., 288GB for HBM3e vs. 141GB for NVDA’s H200) and memory bandwidth (n.b., 6TB/s vs. H200 at 4.8TB/s). Following the MI325X, AMD expects to launch the MI350 series in 2025. The MI350 series is expected to provide a ~35x increase in AI inference performance, and will be positioned to compete against NVDA’s B-Series platforms. And in ’26, AMD is expected to launch the MI400 series, which will be based on its next-gen CDNA architecture, “Next”, to compete against NVDA’s recently announced R-Series platforms.

Changing Consumer Preferences in Gaming

The gaming segment could be affected by changing consumer preferences. If NVDA were to fall out of favor with gamers, its business could be affected.

Cyclicality

The semiconductor industry is well known for boom/bust inventory cycles. A macro-driven inventory correction could have material negative implications for NVDA.

Given the nature of the risks described above, we see little room for these to move in a favorable direction to become positive catalysts. For example, to cast the premium valuation risk as a positive catalyst, one would have to underwrite further multiple expansion – something which seems highly speculative at this point.

Conclusion

While we acknowledge that price momentum and fundamentals favor NVDA, we believe the stock’s valuation is reasonably fair. Given our conservative investment philosophy, we are rating the shares a Hold.

Read the full article here

Q3 2024 Earnings Call Transcript")

")