")

")

")

Li Auto (NASDAQ:LI) is commonly touted as the closest rival for Tesla (TSLA) in mainland China. This is because both companies compete in China’s premium EV segment. Despite the two companies being somewhat comparable, the performance of their stock wildly differs. Unlike the latter, LI stock has underperformed the broader market. However, I believe there is an opportunity for investors willing to take the risk.

Looking at Li Auto’s Business

China has risen in recent years to become a dominant force in the electric vehicle (“EV”) industry. As climate change becomes a more important issue, there is demand for EVs from both consumers and the government. Over 50% of all cars sold in China are EVs, and the share of made-in-China vehicles in Europe is expected to hit 25.3% in 2024. With a large domestic market and the potential for export-led dominance, it might be wise for investors to gain some exposure to Chinese EV stocks.

Among the listed EV companies, Li Auto is one of my favorites. As mentioned, Li Auto can be considered Tesla’s closest rival, as the company also focuses on the “premium segment”. The company has posted decent numbers against the backdrop of a slowdown in overall EV sales (more on this later).

In April, the company delivered 25,787 vehicles, up 0.4% compared to the same time last year. The company also recently launched the Li L6, the company’s cheapest model yet priced under RMB300,000 or $34,500 and targeted at young families. The cheaper model would allow Li Auto to reach more customers. This combined with the company’s premium image could bode well for sales.

The Li L6 has seen positive reactions following its April debut. According to Xiang Li, Chairman and CEO of Li Auto; “Li L6, our first model priced under RMB300,000, has garnered widespread popularity among young families following its April debut. We will commence large-scale deliveries in May“

Li Auto is Cheap

Apart from being well positioned in the market, Li Auto’s stock is also cheaper relative to its Chinese EV peers. In 2024, according to data gathered by Seeking Alpha, Li Auto is expected to earn $1.77 per share, on revenues of $26.7 billion. In 2025, EPS estimates are at $2.43 per share a growth of 37% against revenues of $36.5 billion. Om 2026 EPS estimates are $3.18 per share with revenues jumping to $43.4 billion. These earnings estimates are from 14 analysts for 2024 and 2025 and 11 analysts for 2026. At the average 2026 EPS of $3.18 per share, Li Auto’s stock at current prices is estimated to be trading at a valuation of 8.79x 2026 P/E. The range of 2026 EPS estimates ranges from a low of $1.73 per share to a high of $4.87 per share. This gives us a P/E range of 16.1x to 5.74x 2026 earnings.

These estimate ranges demonstrate how bullish analysts are on Li Auto and how much they believe that the company can maintain its momentum. It also demonstrates that the stock is trading at cheap valuations for a growth stock. Even at the worst-case scenario of analysts’ 2026 EPS estimates, Li Auto is still trading at a 16.1x P/E ratio.

Earnings Estimate (Seeking Alpha)

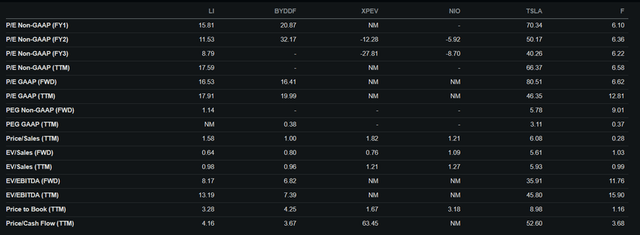

Currently on a TTM basis, Li Auto is trading at a P/E ratio of 17.6x, which is not too far off from the sector median of 14.4x. The company is trading similarly to fellow giant BYD (OTCPK:BYDDF) which has a forward P/E of 16.4x vs Li Auto’s 16.5x. Most of the company’s Chinese rivals have not been profitable on a trailing twelve-month basis, which is why I am looking at forward earnings. This already puts Li Auto a step up above the pack. The company is also a lot cheaper than its US rival Tesla (TSLA) which is trading at an astronomical value of 46.3x TTM earnings. Considering how Li Auto and BYD are giving Tesla a difficult time in the important China market, in my view this valuation gap shouldn’t be this wide.

Relative Valuation (Seeking Alpha)

The other thing I usually check is the health of a company’s balance sheet, just to make sure it isn’t overburdened with debt. Li Auto has $246.1 million in long-term debt and capital leases of $518.2 giving it a total of $764.3 million. This is against total cash and short-term investments of $14.5 billion, which well covers the company’s long-term debt. Total Assets of the company are $20.2 billion vs total liabilities of $11.6 billion. Therefore, I believe that there is nothing to worry about regarding the balance sheet of Li Auto and that the company has enough liquidity should the ongoing EV price war worsen.

China Slowing EV Growth And Risks

The biggest risk facing Li Auto and something that could cause it to miss analysts’ estimates is the potential slowdown in EV and general auto vehicle sales in China. In March, EV sales in China rose by 10.5% compared to the same time last year. However, this was driven by deep discounts and other financing options to boost sales. While this headline figure may not seem so bad, the fact of the matter is the rate of growth is slowing. According to the Reuters article:

For January-March, sales totalled 1.03 million EVs, up 14.7% on year and the slowest quarterly growth since the second quarter of 2023, the data from the China Passenger Car Association (CPCA) showed“

The slowing growth is coming at a pretty bad time, as there is a glut of EVs and EV manufacturers in China. This potential oversupply has triggered an escalating price war. Just recently, in response to Tesla’s price cuts, Li Auto has slashed the prices of some of its most popular models. The Li Mega has seen its price reduced by 30,000 yuan or $4142.

China’s top economic planner, the National Development and Reform Commission (NDRC), has already warned that competition in the EV market will be fierce in the foreseeable future. In my view, that seems to be agreed upon by experts, many of the smaller EV companies will not make it. Thus, we will soon see a consolidation in the industry as the smaller players die off and/or are acquired by the “bigger fish”. Already more than a dozen once-popular carmakers have exited the market, such as WM Motor, Byton, Aiways, and Levdeo.

According to Shanghai-based YouTube, automotive industry commentator Mark Rainford from “Inside China Auto.”:

The price war is likely to rage on further into this year, though it’s hard to imagine prices can come down much further than they already have. The deals available to Chinese car buyers are now very attractive, but some brands will not be able to sustain these discounts forever. They’re going to need deep pockets and smart marketing to take enough business,”

Crisis Meets Opportunity

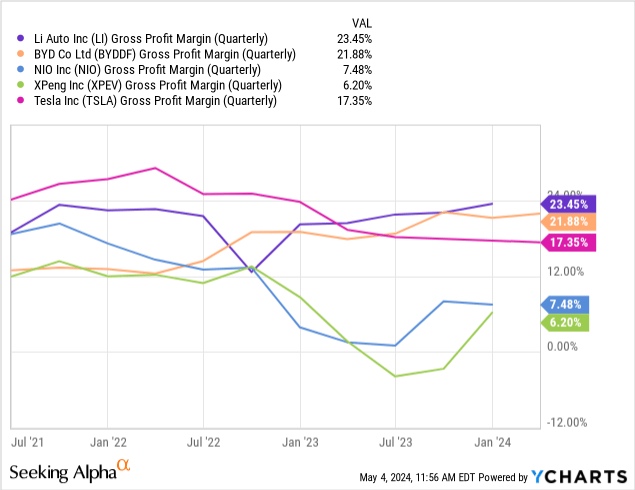

There is an old Chinese proverb that states, “In every crisis lies the seed of opportunity”. I believe that this is the case for Li Auto and the overall Chinese EV sector. Once the price war is over, in the long-term there will be only a handful of players that will survive. In the short term, we can expect margins to remain relatively tight. Based on the last quarter, Li Auto has comparable gross margins to its peers at 23.4%. The company’s gross margins are higher than other smaller players in the Chinese EV market, namely XPeng (XPEV) and Nio (NIO).

However, the end result would be a handful of established, dominant players. In this market with only a handful of players once the oversupply issue is cleared out. I expect gross margins to return to their long-term averages.

I also expect this consolidation to result in Chinese car manufacturers being “ultra-lean” in their operations. This will continue to push China’s dominance in the EV market. Currently, Chinese EVs already make up the majority, or 60% of worldwide sales. Therefore, geopolitical considerations aside, Chinese EVs have a good shot at dominating international markets as well.

Conclusion

Given its fast-growing nature and relatively stable balance sheet, I believe that Li Auto could be among the remaining “survivors” of this difficult period. The company is decently valued at these levels and is growing rapidly. The risks for buyers of LI stock though are the geopolitical risks that come with investing in Chinese companies. However putting that aside, I believe the risk-to-reward dynamic is favorable for Li Auto’s stock.

Read the full article here

")

")

")

")

")