Q3 2024 Earnings Call Transcript")

")

Iridium Communications (NASDAQ:IRDM) is a provider of LEO (Low Earth Orbit) satellite communications that has traditionally focused on voice and SMS but has more recently expanded into areas like data, ADS-B, and satellite-based time synchronization and location services. Iridium’s business is growing at a healthy pace and generating strong cash flows, although some of this is because its constellation was only fairly recently replaced, resulting in a CapEx holiday. While Iridium’s fundamentals appear to justify a high valuation, there is a question of what the pending surge in supply from companies like SpaceX and AST SpaceMobile (ASTS) will do to the market. Iridium believes that its offering is differentiated but it seems reasonable to expect a meaningful negative impact in coming years.

Market

Communications industry sectors include:

- Mobile satellite services – provide customers with voice and data connectivity using ground facilities and a network of satellites. Mobile satellite services are more focused on voice and data services.

- Fixed satellite services – typically use GEO satellites to provide customers with broadband communications links between fixed points on the earth’s surface. Use cases include video and high-speed data customers and international telephone markets.

- Terrestrial services – use a network of land-based equipment to provide wireless or wireline connectivity.

Iridium is a provider of mobile satellite services. While this is a potentially large market, adoption has been limited by cost and capacity constraints. For example, there was an estimated 5.4 billion mobile subscribers globally in 2022, who could be customers at the right price point and with sufficient network capacity.

Satellites may be geostationary (orbiting approximately 22,300 miles above the equator), medium earth orbit (6,400-10,000 miles elevation) or low earth orbit (300-1,000 miles elevation). Iridium’s satellites operate in low earth orbit, which lowers transmission delays and reduces antenna and power requirements. Because of their equatorial orbit, GEO satellites provide limited coverage of regions closer to the earth’s poles.

Mobile satellite service providers include Globalstar, ORBCOMM, SpaceX’s Starlink and OneWeb. Fixed satellite service providers include Intelsat, Eutelsat and SES. Iridium’s main competitors are Viasat, Globalstar, ORBCOMM, and Thuraya. Competition is based on coverage, quality, mobility and pricing.

Operators like Globalstar and ORBCOMM route traffic directly to ground stations in the same region as the satellite, meaning that they are only able to provide real-time connectivity when a ground station is in view of a satellite. This is referred to as a “bent pipe” architecture and limits coverage to areas where the operator has been able to build ground infrastructure. Iridium’s satellites use a crosslink architecture where traffic can be routed between satellites before transmission to the ground, enabling broader coverage.

Iridium’s satellites utilize L-band spectrum which is more resistant to weather interference than the K-band spectrum used by companies like Starlink and OneWeb. Iridium’s L-band spectrum is also globally coordinated by the International Telecommunications Union, simplifying the provision of global services.

Viasat operates a fleet of GEO satellites and is the leading provider of satellite communications services to the maritime sector. Viasat also offers land-based and aviation communications services.

Globalstar operates a fleet of LEO satellites that utilize a “bent pipe” architecture, limiting its geographic coverage. This architecture enables on ground upgrades though. Globalstar is perhaps most notable for its partnership with Apple to provide newer iPhones with the ability to connect to satellites for SOS services.

ORBCOMM also operates a fleet of LEO satellites with a “bent pipe” architecture. ORBCOMM does not offer voice or high-speed data service, choosing instead to focus on low-cost data and IoT services.

New entrants to the satellite communications market include Starlink, OneWeb and AST SpaceMobile. Starlink and OneWeb are primarily focused on commodity broadband services, which Iridium believes is often complementary to its service. Investment in direct-to-device offerings is increasing though, which will be competitive with Iridium.

In the data space, Iridium is avoiding competing with commodity broadband players in the VSAT industry. A VSAT (very small aperture terminal) is a 2-way satellite ground station with a small dish antenna that relies on GEO satellites. Iridium believes that its service complements VSAT and other K-band broadband services as it is less susceptible to inclement weather and can operate in some areas where VSAT services are restricted.

Iridium

Iridium is a provider of voice and data satellite communication services that has been operating for the past 25 years. Iridium’s constellation consists of 66 LEO satellites that operate as a cross-linked network. This minimizes the need for local ground infrastructure and allows Iridium to provide a reliable service in areas not covered by terrestrial wireless and wireline networks.

Iridium holds licenses to use 8.725 MHz of contiguous spectrum in the L-band, which operates at 1.6 GHz, and enabling two-way communication between its devices and satellites. Iridium is also authorized to use 200 MHz of K-Band (23 GHz) spectrum for satellite-to-satellite communications, and 400 MHz of Ka-Band spectrum (19.4 GHz to 19.6 GHz and 29.1 GHz to 29.3 GHz) for two-way communication between its satellites and ground stations.

Iridium replaced its entire satellite constellation in 2019. The new satellites support products with higher data speeds and also host the Aireon system, a global air traffic surveillance system leveraging Automatic Dependent Surveillance-Broadcast (“ADS-B”) receivers.

Iridium has recently started to pursue a direct-to-device service for premium smartphones that would allow Narrowband Internet of Things and two-way messaging and SOS capabilities. Iridium’s satellites do not have the capacity to offer broadband to smartphones. Eventually, the service will be expanded to other devices, like watches, tablets, laptops and vehicles. Iridium is referring to this effort as Project Stardust.

Qualcomm and Iridium had been working together to bring satellite-based connectivity to android smartphones. Qualcomm ended the partnership in late 2023 though, despite already successfully developing a chip. The decision appears to have been driven by a lack of traction with smartphone manufacturers, with price likely a contributing factor. There also appears to have been a reluctance to commit to a proprietary solution. Iridium is now taking a standards-based approach which requires coordination across organizations. The new approach won’t require any specialized hardware. Rather, satellite-connectivity will be enabled through a firmware update by chip makers.

Iridium is currently working with a number of companies to understand their requirements so that they can be incorporated into the planned service. The company anticipates testing to begin in 2025, with a service launched in 2026. Given that Iridium is only offering messaging and SOS capabilities and needs cooperation from device manufacturers, it seems reasonable to question whether the service will be successful. On the plus side, Iridium’s L-band capabilities enable a simple global rollout.

Iridium is also offering broadband, midband and narrowband data through its Certus service. Iridium Certus is designed to support a variety of cost points, antenna types and data speeds up to 704 Kbps. Certus is often used as a companion service to VSAT services in maritime applications, a use case that will be strengthened when Iridium adds support for GMDSS (an internationally recognized distress and radio communication safety system) later this year. Iridium believes data and telematic solutions are its largest growth opportunity and plans on introducing new applications and devices which leverage the Certus platform. This appears to be based around IoT applications with modest data requirements.

Iridium formed Aireon in 2011 and continues to hold a meaningful equity stake in the company. Aireon provides surveillance and other services to ANSPs, amongst other customers. Iridium receives a fee for hosting the ADS-B receivers on its satellites, along with a data service fee for the delivery of air traffic surveillance data. The hosting fee totals 4200 million over the useful life of Iridium’s satellites (now 17.5 years). Power and data service fees are approximately $23.5 million per year. It is worthwhile noting that Spire Global (SPIR) is in the process of introducing a competing service.

Iridium also has an agreement with L3Harris Technologies where L3Harris pays Iridium to allocate the remaining hosted payload capacity to its customers and data service fees on behalf of these customers. L3Harris is the manufacturer of the Aireon hosted payload

Iridium recently acquired Satelles, making it a leader in satellite-based time synchronization and location services, which complement and protect GPS and other GNSS systems. The prevalence of GPS jamming and location spoofing is increasing, driven by rising geopolitical tensions. Iridium’s expanding Positioning, Navigation and Timing solutions can cost-effectively reduce these vulnerabilities and provide an alternative to GPS reliance. Iridium’s STL signal is around 1,000 times stronger than GPS, allowing it to penetrate hard-to-reach areas with only a receiver and small antenna. This is expected to address customer challenges in areas like maritime, aviation, the UAV market, protecting energy grids, and cybersecurity. Iridium expects STL to generate over $100 million service revenue annually by 2030, with additional revenue coming from equipment sales and engineering services.

Iridium provides voice and data communications services to businesses, the US and foreign governments, non-governmental organizations, and consumers. Products and services are distributed through a wholesale network, encompassing around 100 service providers, 300 value-added resellers, and 85 value-added manufacturers.

Iridium believes that its commercial business will be the primary source of long-term growth. Iridium serves customers in a range of industries, including emergency services, maritime, aviation, utilities, oil and gas, mining, recreation, forestry, heavy equipment, construction, railways and other transportation.

The US government is Iridium’s largest customer, contributing approximately 25% of the company’s revenue in 2023. This does not include revenue from the sale of equipment through third-party distributors, or airtime services provided through the company’s commercial gateway, as Iridium lacks visibility into these activities.

Iridium also provides engineering and support services to the US government under a Space Development Agency contract. As a sub-contractor to General Dynamics Mission Systems, Iridium is building ground entry points and operations centers for the Proliferated Warfighter Space Architecture and providing network operations and systems integration services for SDA satellites.

Financial Analysis

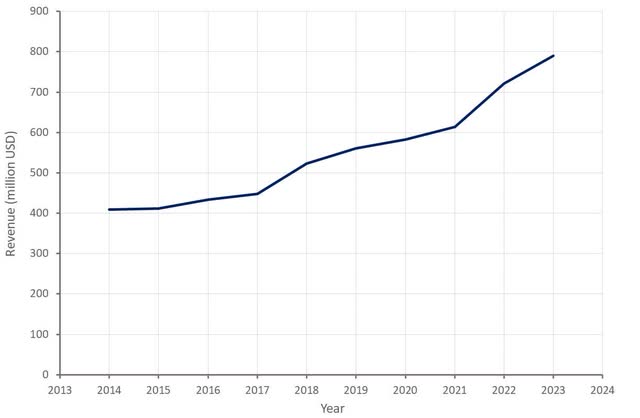

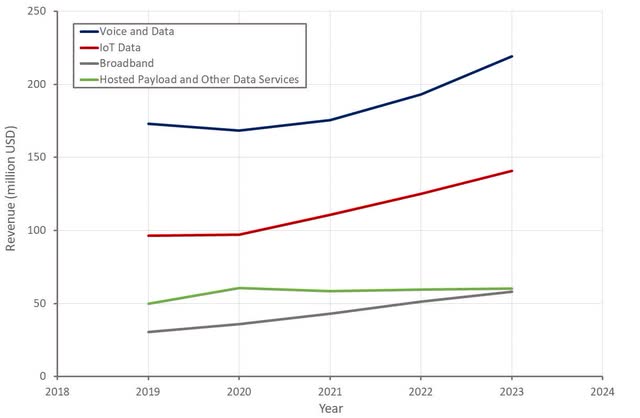

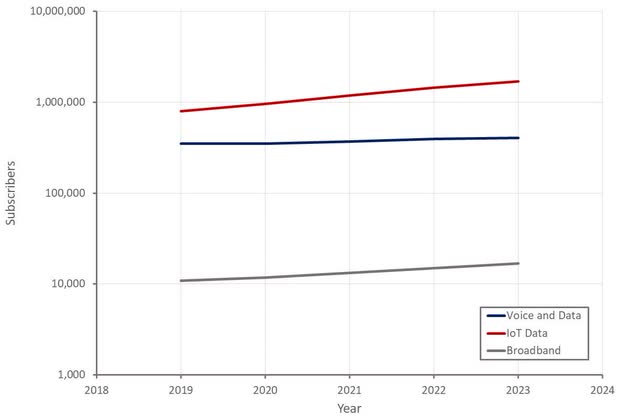

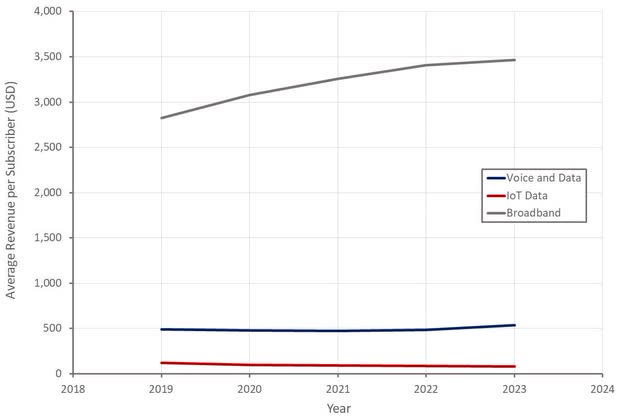

Iridium’s business is expanding at a healthy pace, with solid growth across most of its segments. Service revenue growth is being driven by a growing user base, which recently passed 2,279,000 subscribers, with 15% CAGR over the past five years. IoT data subscribers have grown at a 21% CAGR over the last five years, and now represent about 80% of Iridium’s commercial customer base. Iridium is also seeing solid growth in its broadband subscriber base, although the absolute number is relatively low. Broadband has A large and increasing average revenue per subscriber though.

Figure 1: Iridium Revenue (source: Created by author using data from Iridium) Figure 2: Iridium Revenue by Segment (source: Created by author using data from Iridium) Figure 3: Iridium Subscribers (source: Created by author using data from Iridium) Figure 4: Iridium Average Revenue per Subscriber (source: Created by author using data from Iridium)

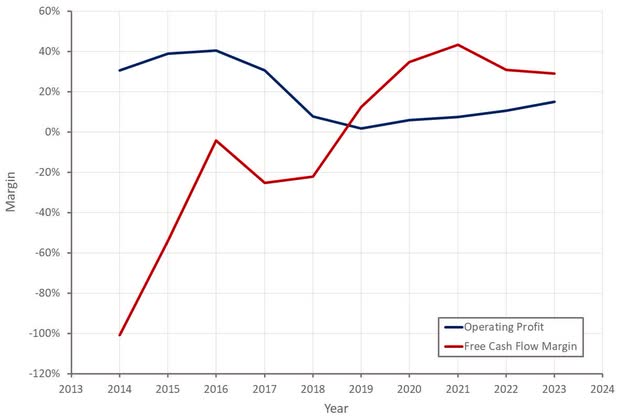

Iridium’s service is characterized by low incremental cost, supporting high margins at scale. While the company’s profit margins and cash flows have fluctuated significantly over the years, I believe an operating margin of around 30% is reasonable in the current environment. There could also be a boost from expansion of the customer base and the introduction of new, higher value-add services.

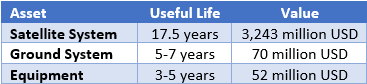

Iridium recently increased the estimated useful life of its satellites by five years based on performance data, which supports limited capital requirements in coming years. These costs should not be ignored though, Iridium has a capital-intensive business, even if capital requirements are only periodic. This change reduced Iridium’s depreciation expense by $27.8 million in 2023 and decreased hosted payload and other service revenue by approximately $2.3 million.

Table 1: Iridium PP&E – December 2023 (source: Created by author using data from Iridium)

Longer term, Iridium’s margins could be pressured from an increased supply of satellite communication services from companies like SpaceX and AST SpaceMobile. While Iridium believes its service is differentiated, it seems likely there will be some impact. In a worst-case scenario, the high fixed cost / low margin cost structure of the industry could create a race to the bottom on pricing.

Figure 5: Iridium Profit Margins (source: Created by author using data from Iridium)

Conclusion

Iridium has a mature business that offers investors solid growth and strong free cash flows. The company’s revenue multiple has compressed to roughly 6 over the past 12 months, its lowest level since 2018. From a cash flow perspective, the stock is looking particularly attractive, although CapEx cannot be ignored, even if cash outflows will be limited for many years to come. With Iridium returning capital to shareholders through quarterly dividend payments and share repurchases, the share price should find support at some stage, although I wouldn’t be surprised if this doesn’t occur until the low 20s.

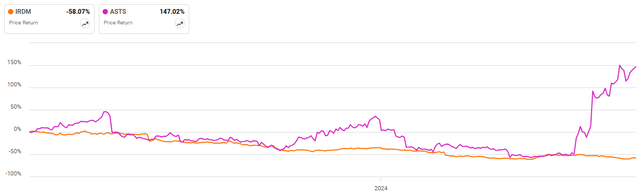

With AST’s business progressing, an argument could potentially be made that the competitive threat to Iridium’s business is increasing. Share price movements of the two companies give little indication that AST’s progress is weighing on Iridium though. While I believe that competition will become more of an issue, the market is likely to be supply constrained for the foreseeable future. Iridium’s service is proven, and its focus on high value use cases probably insulates it from competition somewhat in the near term.

Figure 6: Iridium Share Price Performance (source: Seeking Alpha)

Read the full article here

Q3 2024 Earnings Call Transcript")

")