Q3 2024 Earnings Call Transcript")

")

Co-authored with Hidden Opportunities.

“E pluribus unum” is the traditional motto of the United States, appearing on the nation’s Great Seal. It is Latin for “out of many, one,” symbolizing the unity of the diverse states and people of America, coming together to form a single nation. Since the beginning of the nation in 1776, America has been seen as a land of opportunity.

“In its brief 232 years of existence, however, there has been no incubator for unleashing human potential like America. If you look at what was here in 1776 and you look at what’s here now, this country has done an incredible job in terms of the deployment of resources and human ingenuity. The idea of people unleashing their potential … It’s absolutely a miracle.

Despite some severe interruptions, our country’s economic progress has been breathtaking. Our unwavering conclusion: Never bet against America.” – Warren Buffett.

America is built on the pillars of capitalism, and Mr. Buffett considers the entire system to be a goose that lays golden eggs. In a capitalist system, the market is driven by consumer demands and competition, which often leads to better products and services at lower prices. Mr. Buffett continues to emphasize that we are just getting started with what capitalism can do. Let us now review two picks that form the basis of the American economy but are structurally set up to put dollars into your pocket.

Pick #1: EPD – Yield 7.1%

The midstream industry plays a vital role in the energy supply chain by ensuring the safe, and cost-effective movement and storage of essential energy commodities. Midstream has an enormous economic impact not only on individuals and particular companies, but for the entire nation and has a profound impact on global trade and commerce.

Enterprise Products Partners L.P. (EPD) is the largest American midstream company by market cap. It is one of the best-managed MLPs in the industry, with 25 consecutive years of distribution growth and $53.2 billion returned to unitholders via distributions & unit buybacks since 1998.

The energy midstream business is in consolidation mode, with a significant uptick in dealmaking in recent quarters. While some companies are looking to cut costs, others seek more scalable access to attractive oil and gas-producing regions such as the largest U.S. oil shale patch, the Permian Basin, and export facilities on the U.S. Gulf Coast.

Note: EPD is a Master Limited Partnership that issues a Schedule K-1 to investors.

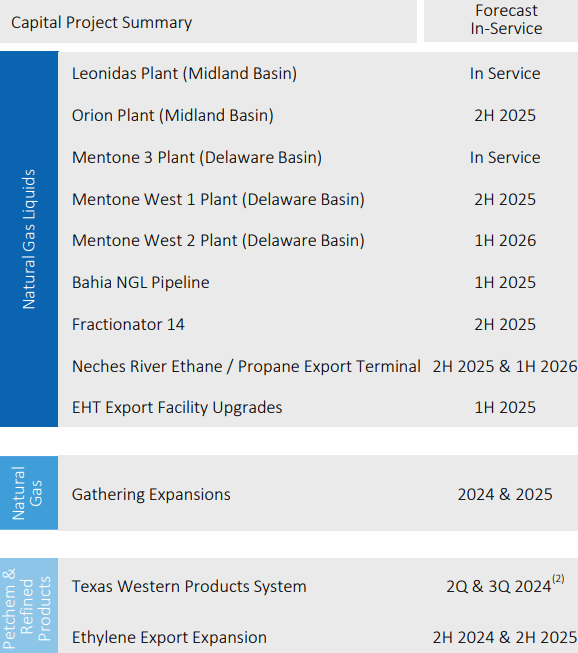

During the first quarter, EPD reported a Distributable Cash Flow of $1.9 billion (flat YoY), delivering a 1.7x coverage for its distribution. The partnership retained $786 million of this DCF. During the quarter, EPD repurchased ~$40 million of its common units on the open market, utilizing a total of 48% of its $2 billion unit buyback program. EPD made capital investments of $1.1 billion, including $875 million for growth capital projects and $180 million for sustaining capital expenditures. The partnership has several projects coming into service in the next 12–18 months, providing excellent tailwinds for continued DCF and distribution growth. Source.

May 2024 Investor Presentation

EPD expects annual growth Capex between $3.25-3.75 billion for FY 2024. The company maintains a strong A3-rated balance sheet with excellent liquidity of approximately $4.5 billion (including unrestricted cash and available borrowing capacity under its revolving credit facilities), positioning it well to accretively acquire suitable targets as the opportunity arises.

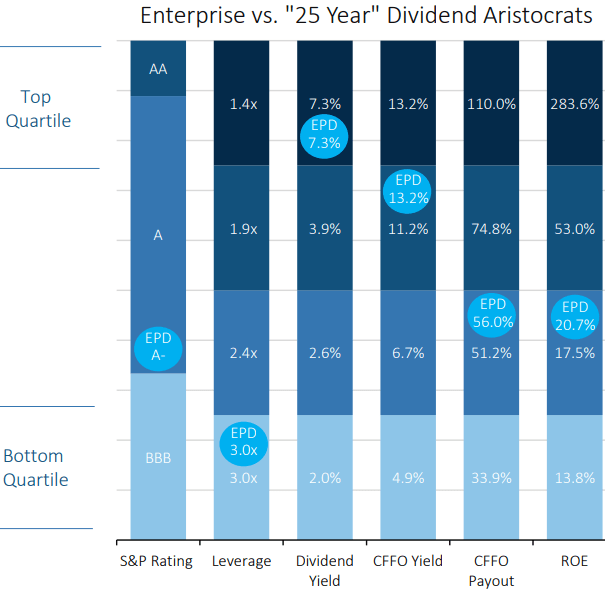

EPD is not just another Dividend Aristocrat, it is la Crème de la crème. Among companies in the aristocrat club, EPD stands tall among the highest yield, lowest leverage levels, and CFFO payout and ROE in the top quartiles.

May 2024 Investor Presentation

With multi-year fee-based contracts with credit-worthy companies, high asset utilization, and excess free cash flow after distributions, we expect EPD to be a strong participant in the growing energy export business while being a meaningful contender in the M&A race to maintain and improve its competitive positioning.

Pick #2: CCD – Yield 10.3%

The NYSE and NASDAQ together comprise a $40 trillion market cap with 6,100 listed companies, almost six times the size of the closest competitor, the Shanghai Stock Exchange, and with more than twice the number of listed companies as the Tokyo Stock Exchange. U.S. markets are highly sought after for innovation and growth from world-class companies.

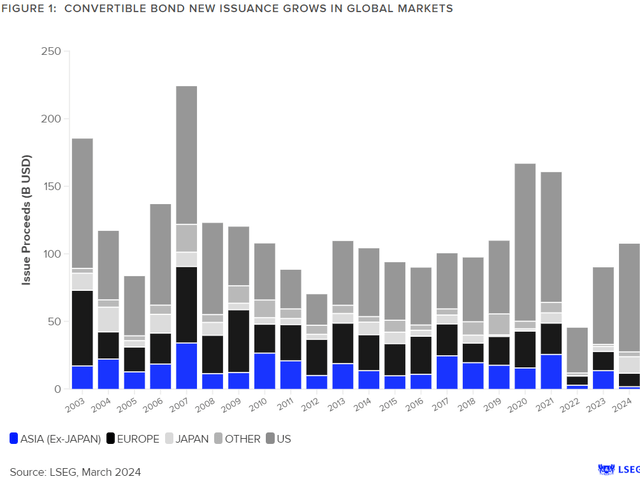

Amid rising interest rates in 2023, the issuance of convertible bonds soared, and the trend is continuing in 2024. Global convertible debt issuance in 2023 exceeded $90 billion, and the U.S. market dominated in this asset class, with issuances worth $57 billion. In Q1 2024, $25.2 billion in new convertibles were issued globally, and the United States led the group with $20.8 billion, Japan raised $2.9 billion, Europe launched $1.1 billion, and Asia ex-Japan introduced $400 million.

LSEG

These new convertible issues offer attractive terms, including higher coupons and lower conversion premiums. Top issuers come from a wide range of industries, including AI firms like MicroStrategy and Super Micro Computer, ride-share contender Lyft, fintech superstar SoFi Technologies, and clean energy producers NextEra Energy (NEE) and Kosmos Energy. U.K.-based financial data provider, LSEG estimates between $100 and $110 billion of global convertible issuances to occur this year, creating a tremendous opportunity in this inaccessible asset class via CEFs.

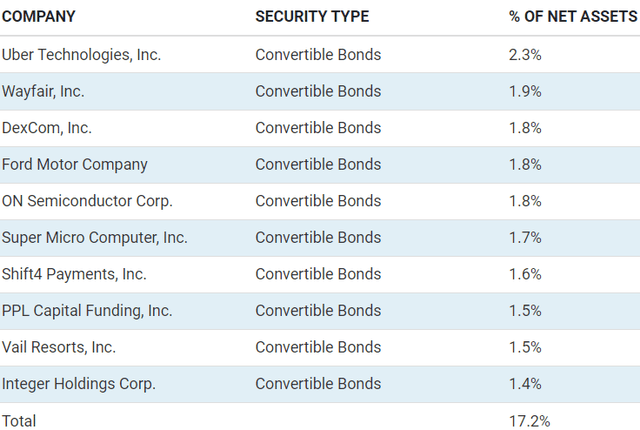

Calamos Dynamic Convertible and Income Fund (CCD) is highly diversified across 602 holdings, primarily convertible debt, some corporate bonds, and preferred stock. ~57% of the fund’s assets are deployed across securities issued by Information Technology, Healthcare, and Consumer Discretionary companies. Notably, 95% of the CEF’s exposure is in securities issued by American corporations. Source.

Calamos Website

There is much discussion about CCD’s distributions for the first half of FY 2024 being 80% ROC (Return of Capital) and 20% short term capital gains. Let us dive a bit deeper. Since its inception in March 2015, CCD has distributed a total of $18.17/share, and ~48% was ROC ($8.725). The CEF’s IPO price was $24.50/share.

“The best measure of whether a fund has earned its distributions is the change in its NAV net of distributions. Regardless of how distributions are characterized if a fund’s NAV increases, the fund earns its distribution. If not, the fund did not earn its distribution – the economic concept of return of principal.” – Return of Capital Demystified, Eaton Vance.

If CCD was having destructive ROC, its current NAV would be much less than 15.97 (24.50–8.725). However, since the most recent NAV reported was close to $19, we see that CCD is earning its distributions.

CCD pays $0.195/month, calculating to a 10.3% annualized yield. While the CEF trades at a 19% premium to NAV, it is important to note that convertibles are illiquid instruments typically inaccessible to retail investors. As such, the valuation of illiquid securities is typically conservative and subjective and may involve some degree of estimation and judgment.

Convertibles are a hot security class in current market conditions and will likely see further acceleration in issuances if the U.S. economy plunges into a recession. As a basket of instruments that can deliver positive returns in good times and shield investors when markets are miserable, CCD presents an attractive investment opportunity to collect big yields while waiting for the economy to figure out its next steps.

Conclusion

Every business or even country has good and challenging times. It is a cycle, and the robust and well-managed institutions overcome their challenges and thrive over the long term. America is a nation built on ideals of resilience, innovation, and the unwavering belief in progress, which continue to enable it to navigate and flourish through the ebbs and flows of history. Millions of individuals globally either seek to move to the United States to harness the power of the American Dream, pursue business with American organizations, or invest in the American economy. Notably, the U.S. is a top destination for foreign direct investment. As Mr. Buffett says, it is never wise to bet against the American economy, the engine of wealth and prosperity.

With EPD, you get access to a well-managed firm operating the largest network of energy pipeline, storage, and processing infrastructure, pursuing a business that cements America’s position as a leader in energy exports. With CCD, you get access to a highly sought-after means to raise capital amidst high borrowing costs and generally weaker valuations amidst an economic slowdown. Together, they enrich my passive income stream, but these are just two among over 45 dividend-paying holdings in our Investing Group’s model portfolio.

Our Investing Group taps into this massive wealth generator with a diversified approach to collect regular paychecks in the form of large, growing dividends. We call this approach The Income Method, our secret to leading a stress-free retirement.

Read the full article here

Q3 2024 Earnings Call Transcript")

")