")

")

")

Shares of H&E Equipment Services (NASDAQ:HEES) have been a meaningful underperformer, trading roughly flat over the past year. Since I recommended shares in October, they have done better, gaining about 11%, about 2% ahead of the S&P 500’s return. They have though continued to lag United Rentals (URI), likely on concerns about its large growth spending and increased profits from used equipment sales. I view these concerns as overstated, and continue to expect shares to push toward $55, which is why I am reiterating a buy recommendation.

Seeking Alpha

In the company’s third quarter, H&E grew revenue by 24% to $401 million while adjusted EBITDA rose by 36% to $189 million. EPS rose by nearly 30% to $1.35. Its fleet size grew by 28% with utilization dropping by 3.3% to 70%, which is why revenue growth lagged in fleet growth. Sequentially though, utilization rose by 70bp from 69.3%.

This strong level of growth has been a two-edged sword for H&E. Clearly, the top and bottom-line growth has been strong, a positive, as H&E has been able to push more equipment rental into a strong market. However, this growth has been funded via borrowing with H&E outspending cash flow to grow its fleet. At the same time, utilization is lower than a year ago, which has led to some concern that H&E is outgrowing the market. Alongside the last quarter, management raised its 2023 growth cap-ex spending guidance to $650-700 million from $600-650 million given elevated customer demand and improved availability of equipment, suggesting it is doubling down on this strategy.

Through nine months, HEES’s operating cash flow has been $277 million. Excluding working capital, it has generated $398 million. This has resulted in a free cash outflow of $176 million this year as it has invested $472 million in its fleet, up nearly 50% from $323 million last year. There are several reasons why I view this investment as appropriate and not endangering shareholder value. First, H&E’s EBITDA has been rising more quickly than its debt load. Leverage remains modest with debt/EBITDA at 2.1x, slightly lower than 1, 2, and 3 years ago when leverage had been as high as 2.5x. Even with free cash outflows, H&E is a bigger company today with less financial leverage. By building scale, it has actually de-risked its financial profile relative to several years ago.

One danger for companies with free cash outflows is reliance on debt financing. Now, with interest rates having come down from their highs, this is less of a concern than several months ago. Nonetheless, I would note that of its $1.4 billion in debt, $1.25 billion is in unsecured notes that do not mature until 2028, leaving it with no material refinancing or interest rate risk. From a capital allocation and financial prudence standpoint, H&E’s growth plans are causing no problems.

Now, just because a company has the financial flexibility to invest large sums does not mean that it should. There is likely some concern that if there is a downturn in demand for equipment, this fleet expansion will prove unwise, essentially equivalent to buying at the top of the market. I do not view that as likely the case here, either.

Lower utilization has been a focus, but it is important to note that utilization can be too high. A business with 100% utilization likely has more demand than supply, meaning it is leaving money on the table. Investors would want to see it grow capacity and have overall utilization fall somewhat.

That is where I think H&E sits. Last year, given the surge in construction activity and battered supply chains, it ran exceptionally high utilization, which is now returning to normal levels. Now, if we see utilization continue to fall, that would be a concern for me and a risk for investors to monitor. Fortunately, we saw utilization rise sequentially in Q3, in keeping with my view of things stabilizing at a healthier, normal level.

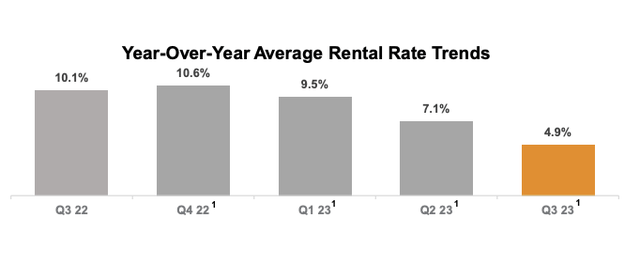

Beyond utilization, the price of rentals is a good indicator of demand. Rental rates rose by 4.9% from last year, continuing their slowing, but the quarterly rate stabilized at 1.2% from 1.1% in Q2. 10%+ inflation is not sustainable, but the fact pricing is still moving at 5% annually sequentially is a sign of robust ongoing demand. Importantly, management expects incremental improvement in rental rates in Q4.

H&E Equipment

All of this argues for ongoing demand that enables H&E to expand its fleet. I think it is also important to emphasize that H&E is not simply adding fleet to its existing markets, which increases its saturation risk. It is expanding into new locations and populating those branches with fleet. Through September, H&E opened 12 branches, well on track for its 12-15 branch guidance. It expects to do another 15 locations next year. Consistent with this strategy, in December, H&E did a bolt-on acquisition of Precision Rentals, helping to deepen its network in the high-growth Phoenix and Denver markets.

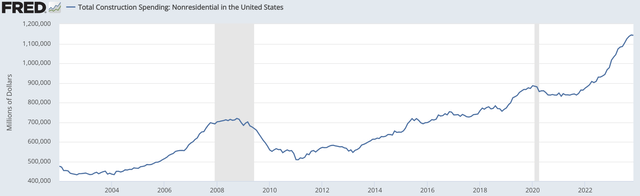

Of course, equipment rental demand can be tied to economic activity. About 69% of its revenue is in nonresidential construction. As you can see below, activity here has boomed. This is driven in large part by government policy as spending in the bipartisan infrastructure bill, inflation reduction act, and CHIPs act has ramped up, from both direct government spending and private sector incentives.

St. Louis Federal Reserve

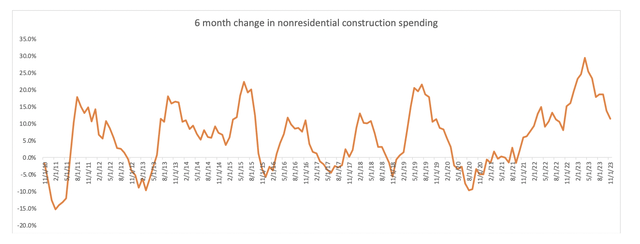

A few months ago, nonresidential construction was rising at a 30% annualized pace as these government programs began ramping up. Of course, such a pace of growth cannot be sustained for an economy as large as developed as ours, and it has slowed all the way down to 11%. While these government programs will continue for several years, that continuation simply supports the level of spending, not further growth from this level.

St. Louis Federal Reserve, my own calculation

My view is that given the multiyear nature of these government programs, nonresidential spending is likely to be less cyclical than it has been historically and that it should persist around current levels with the pace of growth continuing to slow. Given H&E’s small size and expansion into new geographies, I believe that backdrop is strong enough to support its recent fleet expansion and continued double-digit growth. I would be concerned if we saw construction spending begin to fall, but between government support and a soft landing appearing more likely, this does not appear to be the central case.

One other headwind for shares has likely been a concern about the quality of earnings. In Q3, gross margins expanded by 20bp to 47%, aided by favorable mix and ongoing strength in the resale market. Used equipment gross profit of $31 million was up from $11 million last year. That extra $20 million is about $0.40 cents of EPS. Now, margins were 480bp higher, helping to drive some of this increase. However, the majority of the gain was driven by the fact used sales rose by 2.5x. With utilization normalizing, H&E has returned to selling a normal share of equipment. As such, I do not think this level of profits is unsustainable.

As supply chains have improved, we now see equipment manufacturers delivering more products than they have orders for, unlikely 2021-2022 when deliveries were low, and backlogs grow. As new equipment has been hard to find, used prices have been strong. With supply chains normal, used prices could be weaker, reducing this source of profitability.

St. Louis Federal Reserve

While this is a risk to EPS, this would actually be beneficial for HEES’s cash flow in all likelihood. H&E is investing 4x as much in new equipment as it is making from selling used equipment. A decline in the prices of equipment will make its growth efforts less costly and likely increase the returns on this invested capital. As a company expands its fleet, weaker equipment prices are likely a net positive as any headwind from lower used prices is offset by better margins on new purchases over time.

Finally, it is important to again emphasize this cash outflow is voluntary, due to this growth spending. H&E can quickly curtail cap-ex, age its fleet, and generate cash flow. Its fleet age is just 41 months vs the 49-month industry average. Last quarter, the units it sold were on average 75 months old, speaking to the potential capacity to age its fleet. However, with its growth plans, management expects to be 2-3 years away from consistently positive free cash flow.

I recently downgraded United Rentals to a “hold” from “buy,” given its free cash flow yield has contracted to 6.5%, which I view as a full valuation given a nonresidential construction sector likely to stay strong but grow more slowly. When I last wrote bout HEES, I argued it had about $400-450 million in operating cash flow capacity at its existing fleet size, even assuming a modest drop in rental rates, which would translate to about $150 million in free cash flow if it simply kept its fleet size constant.

Given management commentary that rental rates are improving in Q4 and likely in 2024, that $150 million estimate is likely low by $15-25 million.

That provides a 9-10% sustaining free cash flow yield, which I believe is pricing in a risk that H&E is overinvesting. In 2024, as we see nonresidential spending hold up and H&E deliver solid utilization results, these fears should dissipate. That should enable its shares to move to $55-58, or about an 8% free cash flow yield. Against this backdrop of elevated construction spending, H&E screens attractive vs larger peers like URI, given its cheaper valuation and better expansion opportunities, given its smaller size. With leverage muted, this growth spending is not overly ambitious, and I would remain long shares.

Read the full article here

")

")

Q2 2024 Earnings Call Transcript")