")

")

")

Thesis

Chipotle Mexican Grill (NYSE:CMG) is one of the best-run companies in the restaurant category that significantly outperformed the market. Over the last year, CMG’s stock has risen by more than 55% with its multiples expanding and fundamentals growing. Even though in my opinion, CMG is expected to grow over the longer term due to profitable expansion, investments in new technologies, robotics and AI, the company trades at high price multiples. I rate CMG stock a hold at this level.

Introduction and Performance

CMG became one of the most popular fast-casual restaurant chains, known for its Mexican-inspired cuisine. The chain is relatively young as it was founded in 1993 and as of 31 March 2024 had a total of 3,479 restaurants in the United States, Canada, the United Kingdom, France, United Arab Emirates and Germany. Some of its favourite menu items include burritos, bowls, tacos, and salads and CMG is well known for its super customisation. Their emphasis is on using a few, fresh and high-quality ingredients.

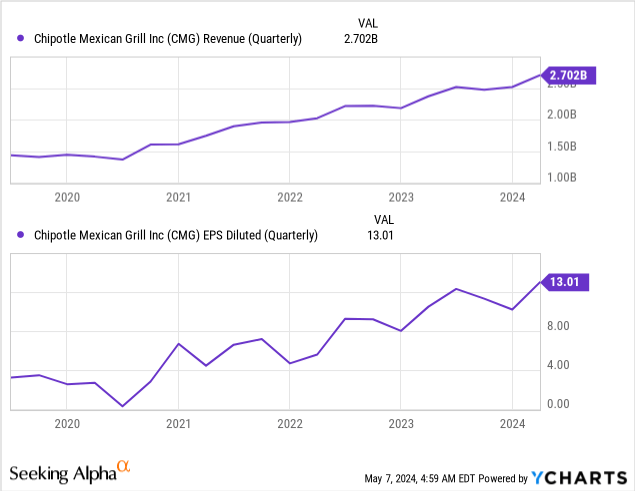

CMG has seen strong growth in their fundamentals and restaurant locations over the years. The Q1 2024 results announced on the 24th of April 2024 was another stellar quarter for the company with no signs that the company is slowing down. Year on year the top-line grew by 14% to $2.7bn, comparable restaurant sales increased by 7%, operating margin improved to 16.3% and diluted earnings per share grew by an impressive 23.9% to $13.1. The good results were a combination of new restaurant openings, a 5% growth in transactions, restaurant margins increasing by 190 basis points year on year and share buybacks.

As we can see below, this was not a one-off or unique quarter. Following the COVID-19 pandemic and the associated lockdowns, management has done a great job in increasing both the top and bottom lines over the years. The total growth over the last 5 years was 88% and 304% for revenue and diluted earnings per share, respectively.

I have looked into a couple of other restaurant chains recently, Texas Roadhouse Inc. (TXRH) and Wingstop Inc. (WING). I found out that well-run restaurant companies can outperform the overall market, which, in my opinion, a lot of people find surprising. If you want to check my opinions on TXRH and WING, check here and here. In my opinion, CMG is a very well-run restaurant chain and has the potential to continue to outperform the market.

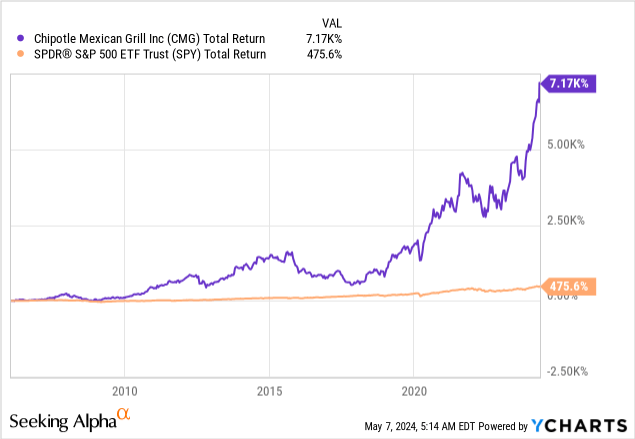

As we can see below, CMG has significantly outperformed the market since the company went public back in 2006. CMG had a total return that was 15 times more than the overall market.

In my opinion, CMG’s performance will continue to outperform the market due to investments in new technologies, robotics and AI, but as I discuss below, investors should be looking for opportunistic periods to invest in the company as the price multiples are trading at high levels.

Sustainable Growth and Good Execution

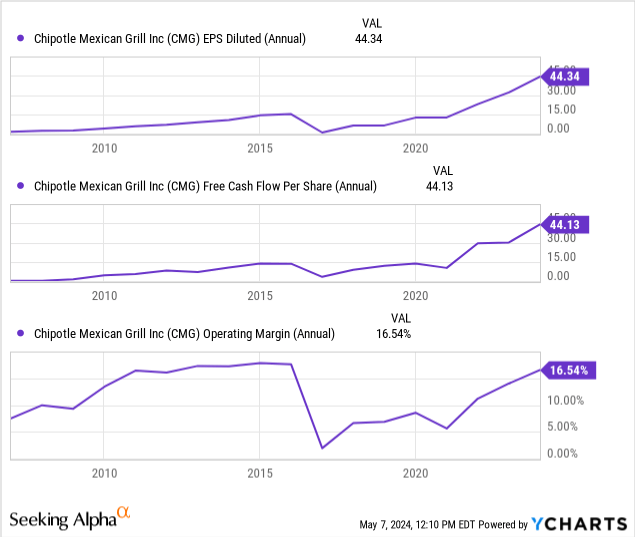

When I look at such a superior total return outperformance relative to the market, I like to go back in time to understand how the underlying business fundamentals have evolved. Below, I included what I consider to be important metrics from 2006 (when the company went public) and 2023 for CMG.

| 2006 | 2023 | |

| Number of restaurants | 581 | 3437 |

| Operating margin | 8% | 16% |

| Diluted EPS | $1.3 | $44.3 |

| Free cash flow per share | -$0.2 | $44.1 |

Since CMG went public the number of restaurants has increased by 5.9 times, operating margin has doubled, diluted earnings per share increased by 34.1 times and free cash flow per share went from -$0.2 to $44.1. To help with visualising the trajectory of these statistics over this period, see the charts on diluted earnings per share and free cash flow per share below.

The increase in restaurants led to scalability benefits for the company, increasing operating margins which then led to increases in free cash flow and diluted earnings per share leading to stellar shareholder returns. Management over time has demonstrated its ability to execute well.

Looking at CMG today, in my opinion, there are still multiple levers that management is already using to continue to grow the business. These include Chipotlanes, robotics and AI.

Chipotlanes

Chipotlanes is another way for CMG’s management to tap into existing and new customers, as these are their pick-up or drive-through type of serving customers. Management is focusing on this to ensure that customers get what they need and has proven to be margin-friendly.

In 2023, out of the 271 new restaurants, 238 had a Chipotlane. Management also said they expect more than 80% of their new restaurants will have a Chipotlane. Why is this important? This ensures that the customers looking for this kind of service have a better overall experience with CMG, and restaurants can manage their pick-up order flow better. In 2023, around 37% of sales went through their digital channels, which include Chipotlane. This compares with 2018 digital sales accounting for 11%. Digital sales are growing and Chipotlanes can facilitate this service and improve the company’s margins.

In addition, during the Q1 2024 earnings call management was clear that this kind of drive-through (the digital version) is the only drive-through they are interested in as it provides the best way to customise orders, has no waiting times, offers more accurate orders and good order management for the restaurants. This kind of service through Chipotlanes ensures customer satisfaction and productivity gains for the business.

Technological Innovations

Chipotlanes have a digital element in it, but I refer to technological innovations as the adaptation of robotics and AI within CMG restaurants. In my opinion, CMG will benefit from AI and robotics in the future. AI and robotics combined with restaurant chains might sound extreme or wishful thinking for many investors, as these are often linked to tech companies. As I discuss below, CMG has already made moves in this area and the possible upside on these investments are significant for the business.

People are very well familiar with Chipotle’s guacamole, and CMG was expected to go through 100 million pounds of avocado in 2023. The process of preparing avocados, as you can imagine, is labour intensive. Well, CMG partnered with Vebu to create the Autocado. Autocado is expected that its application could end up reducing the guacamole preparation time by 50% and is expected to improve the avocado yield from precision processing. If successful and widely used, this will end up saving the company millions. Autocado will offer both productivity gains and direct cost savings from avocado consumption.

In addition, CMG invested in a digital makeline aiming to automate bowl and salad making. Essentially, CMG is hoping to have the ordering and making of these orders automated. A customer will order through the digital channels and if the order is a bowl or a salad, then the digital makeline will prepare the orders. The significance of this is huge for CMG’s business, as around 65% of CMG’s digital orders are bowls and salads. If this is successful and widely adopted in the company, it will lead to greater productivity as fewer workers will be needed to prepare these orders and better customer satisfaction as the accuracy of these orders will improve.

Overall, CMG embraces technological innovation and adoption in their restaurants and is experimenting with a lot of new technologies, robotics and AI within their restaurants and in their supply chains. The above are just two examples, but there are countless more. The size of CMG and its scale allows it to explore these avenues and, if successful, I expect the productivity and hence operating margins to improve for the business. In my opinion, Chipotlanes, robotics and AI will continue to have a positive impact on CMG well into the future.

Relative Valuation

Personally, the only issue I have with CMG is its current valuation. As I discuss below, given the recent stock performance, in my opinion, CMG is relatively overvalued.

| CMG | TXRH | WING | SBUX | Rank | |

| P/E GAAP (FWD) | 57.7 | 28.3 | 116.6 | 20.2 | 2nd |

| EV/EBIT (FWD) | 46.5 | 25.1 | 79.4 | 18.0 | 2nd |

| P/Cash Flow (FWD) | 41.8 | 17.3 | 84.4 | 15.6 | 2nd |

| Return on common equity (TTM) | 44.4% | 29.3% | NA | NA | 1st |

As we can see above, CMG is relatively overvalued. On all forward price multiples, CMG is the second most expensive company amongst its peers and offers the best return on common equity. Even though Wingstop Inc. is more expensive, as I discussed here, I consider WING to be significantly overvalued.

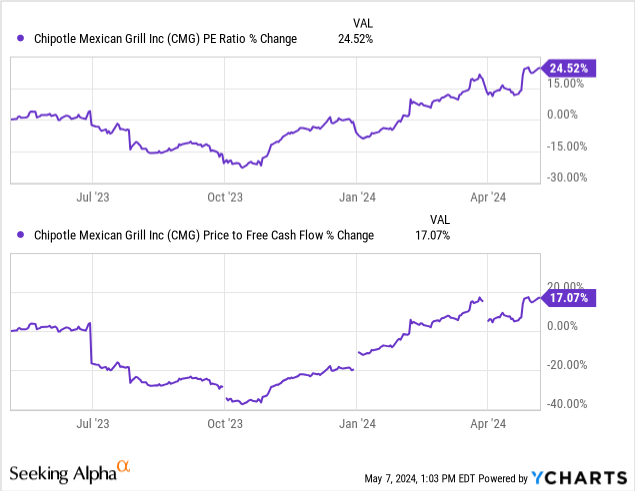

In addition, as we can see below, the price-to-earnings per share multiple and price-to-free cash flow multiple have both increased over the last year. The price-to-earnings per share multiple increased by 25% and the price-to-free cash flow multiple increased by 17%.

Given the relative valuation and recent price multiple expansions, in my opinion, CMG is relatively overvalued and has no significant margin of safety at this level.

Risk

As I discussed above, CMG historically has had very strong business performance, which is reflected in the total return performance. In my opinion, Chipotlanes, robotics and AI are great initiatives to help the company improve margins, capture more customers and further grow its fundamentals.

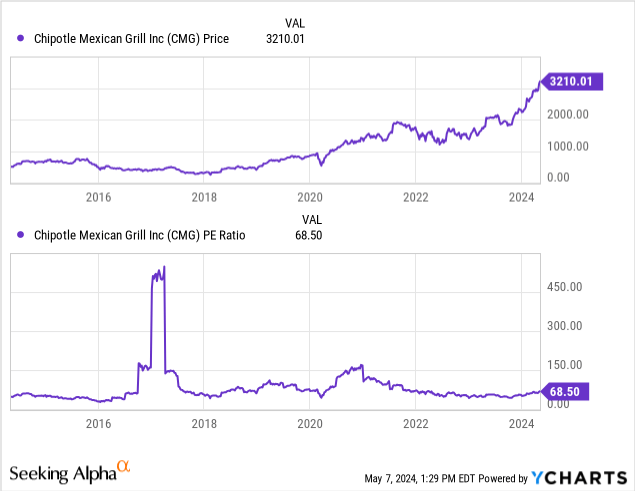

However, in my opinion, recent stock performance and current price multiples do not provide any margin of safety. Even though CMG has a great business, I rate CMG a hold due to no margin of safety. The main risk for this thesis is that CMG outpaces the market’s growth expectation and eventually grows into its price multiples. As per below, CMG did trade at relatively higher price multiples and had a strong stock price performance at the same time.

Hence, my approach with CMG is to invest opportunistically when and if the stock price falls. I am comfortable waiting for a better margin of safety opportunity down the line. However, there is a high risk this pullback never comes, and the stock continues to rise further.

Conclusion

CMG has significantly outperformed the market since it went public. In my opinion, CMG has the potential to continue to outperform, but investors need to be more opportunistic in investing in the company given the current high price multiples the company is trading today. CMG will benefit from Chipotlanes, robotics and AI and is overall relatively overvalued. I rate CMG a hold.

Read the full article here

")

")

")

")

")