Q3 2024 Earnings Call Transcript")

")

Introduction

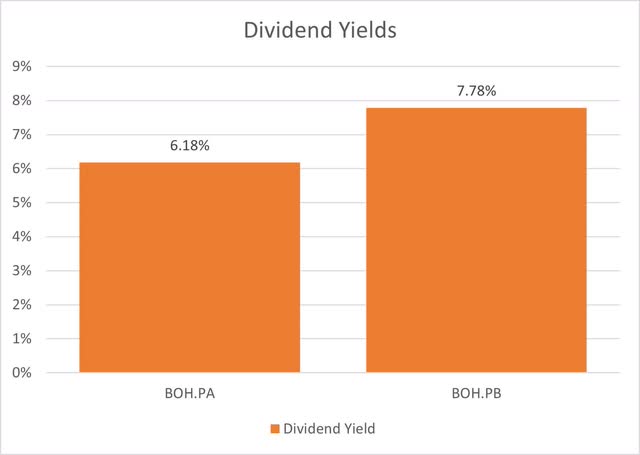

Bank of Hawaii (NYSE:BOH) is a regional bank and serves as Hawaii’s second oldest bank. The bank does have a presence outside of the island state with branches in the American southwest. Bank of Hawaii also had a single preferred share (BOH.PA) that offered an uninspiring yield of just over 6%. Recently, the bank announced the issuance of a second preferred share (BOH.PB) with an 8% dividend. Since its IPO, the shares have traded at a premium, but I believe the new preferred shares are still attractive with a 7.8% yield.

Microsoft Excel API

Bank of Hawaii Financial Results

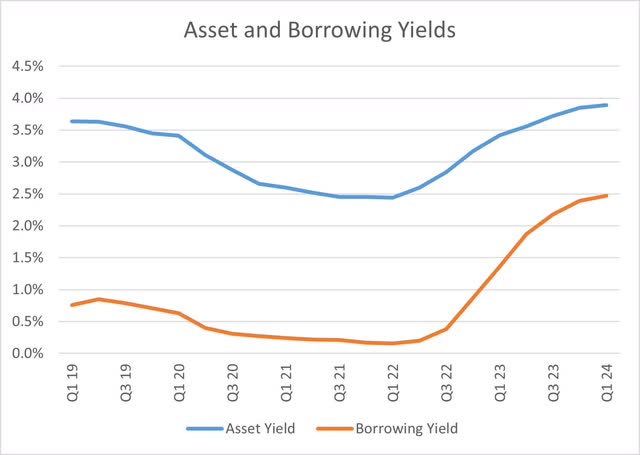

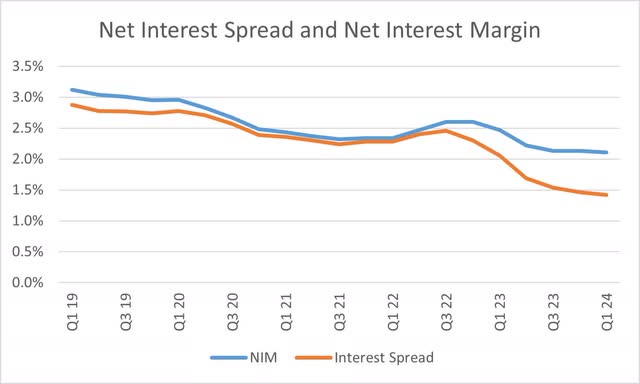

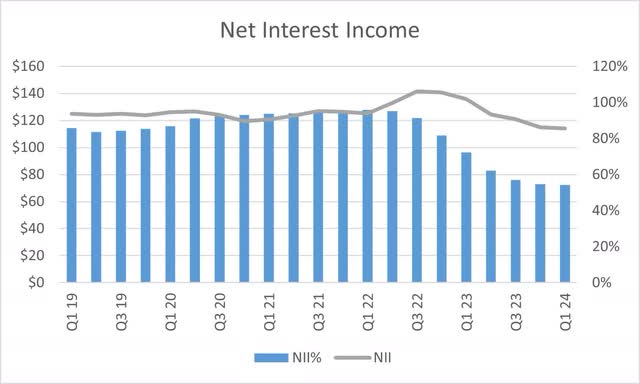

The recent rise in interest rates led to regional banks trying to maintain their earnings with the changing rate environment and Bank of Hawaii was no different. As rates rose, the bank’s asset yields rose, but borrowing costs rose at a faster pace. The squeeze has led to a drop in the net interest spread. While some banks have managed to efficiently allocate capital and stabilize their net interest margins, Bank of Hawaii is still seeing a net interest margin decline, albeit much slower in recent quarters.

Bank Financials

Bank Financials

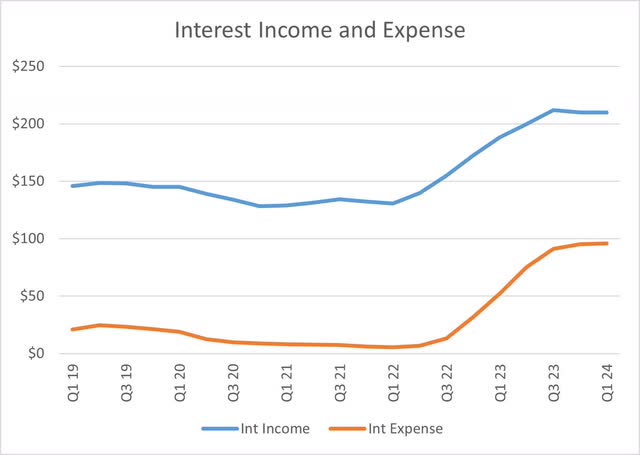

When it comes to overall earnings, the bank is seeing the resistance on the yield side is clearly bleeding through. Over the last couple of quarters, the bank’s interest income growth has stalled even with higher interest rates. This combined with higher interest expense, has led to five consecutive quarters of net interest income (interest income less interest expense) declines. While many regional banks have generated net interest income above their pandemic or pre-pandemic levels, Bank of Hawaii is not one of those banks.

Bank Financials

Bank Financials

Loans and Deposits- A Sign of Conservative Capital Management

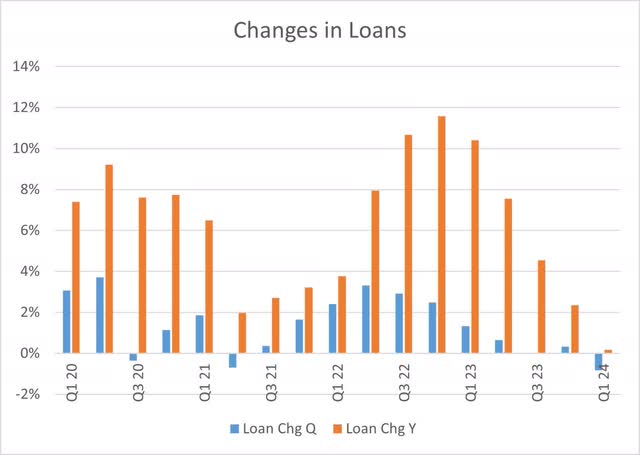

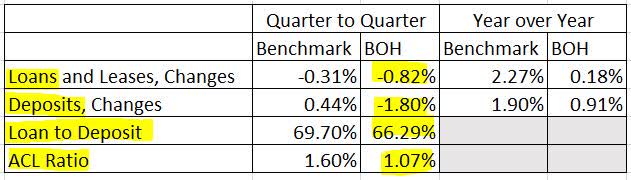

With respect to the health of the bank, I find the management of the bank’s lending and deposit growth to be a positive development. During the pandemic, many bank balance sheets grew north of 20%, which made things more difficult when the fight for deposits started in late 2022. Fortunately, Bank of Hawaii’s lending growth has been conservative over the past few years and is currently flat on a year over year basis.

Bank Financials

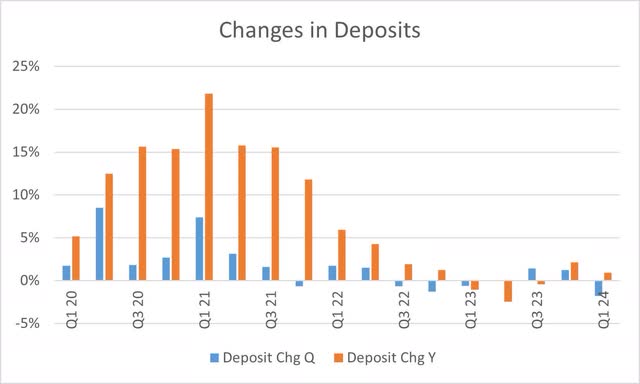

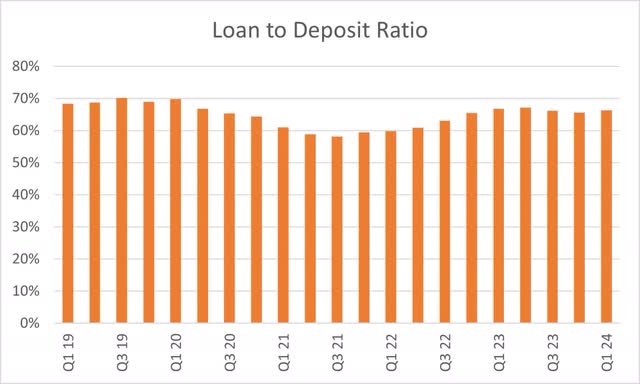

On the deposit side, the Bank of Hawaii has not been immune to the challenges of retaining depositors in the regional banking space. Deposits dropped in the first quarter and have declined in four out of the last seven quarters. The tame growth in both loans and deposits continues to help the bank’s modest loan to deposit ratio, which sits under 70% and under the average for all commercial banks. The advantage to a conservative loan to deposit ratio is that the bank is not dependent on external financing and can grow its lending in the future without necessarily growing its deposits.

Bank Financials

Bank Financials

Bank Financials & Federal Reserve Weekly Commercial Bank Data

Risks to Bank of Hawaii

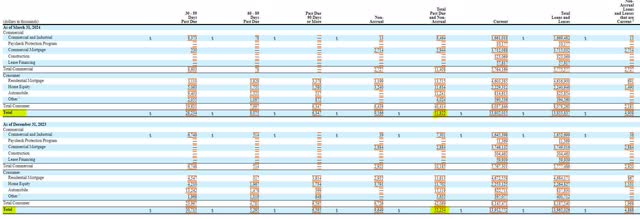

For Bank of Hawaii, I believe that investors need to watch the bank’s loan concentration carefully. As it stands, the residential real estate market is the bank’s largest exposure with approximately half of the bank’s loans tied into residential mortgage and home equity loans. The next largest loan concentration is commercial real estate mortgages which account for $3.7 billion of the $13.8 billion loan portfolio. While the commercial real estate market is facing self-explanatory headwinds, changes in the labor market and broader economy can create challenges in the performance of the bank’s residential real estate mortgages.

SEC 10-Q

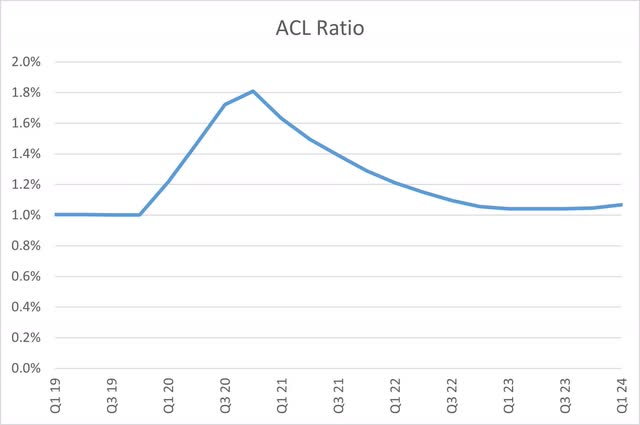

Fortunately, the Bank of Hawaii’s loan performance is currently very strong. In the first quarter, the bank identified $52 million in loans as either delinquent or on nonaccrual status, which is less than 0.5% of total loans. Despite the strength of the bank’s loan performance, investors should be mindful of the fact that the bank’s allowance for credit losses is sitting at around 1% of gross loans, which is well below the 1.6% industry average. Should loan performance begin to slip, there’s little buffer between loan performance and earnings.

SEC 10-Q

Bank Financials

Another risk facing the Bank of Hawaii is the number of uninsured deposits. Despite declining by more than $250 million in the first quarter, the bank is still carrying more than $8.6 billion in uninsured deposits, which accounts for more than 40 percent of the bank’s total deposits. Fortunately, the bank has sufficient liquidity to cover their uninsured deposits with $9.4 billion in borrowing capacity between the Federal Reserve and FHLB. But investors should be reminded that if liquidity is needed, it would undermine earnings.

SEC 10-Q

SEC 10-Q

Conclusion

The Bank of Hawaii’s low net interest margin combined with its soft buffer for loan losses are the primary reasons I am not advocating an investment in the bank’s common shares. Investors seeking value should take notice that Bank of Hawaii’s common shares are trading at 16 times earnings, which is expensive considering JPMorgan Chase is trading at 12 times earnings. The Series A preferred shares offer a dividend yield below most of the bank’s peers. The Series B preferred shares offer an attractive 7.8% yield with a call date that is five years away and are the best option for income investors.

Read the full article here

Q3 2024 Earnings Call Transcript")

")