")

Following our last update, “Too Cheap To Ignore,” and an expectation reset in early December 2023, Anglo American (OTCQX:AAUKF, OTCQX:NGLOY) reported its FY 2023 results and the just-released Q1 production report.

For our new readers, Anglo-American is one of the world’s most prominent diversified mining players. The company is headquartered in London and listed on the JSE (South Africa Stock Exchange) and the FTSE (UK Stock Exchange). The company’s main commodities are copper, iron ore, thermal, and met coal, as well as diamonds and PGMs (Balanced Approach To Earnings Diversification). Here at the Lab, we have a long-standing buy rating thanks to 1) the Quellaveco copper mine expansion located in Peru, 2) the company’s risk/reward attractiveness due to recent stock underperformance, and 3) the Woodsmith polyhalite project in the United Kingdom.

Q1 Production Results and Earnings Changes

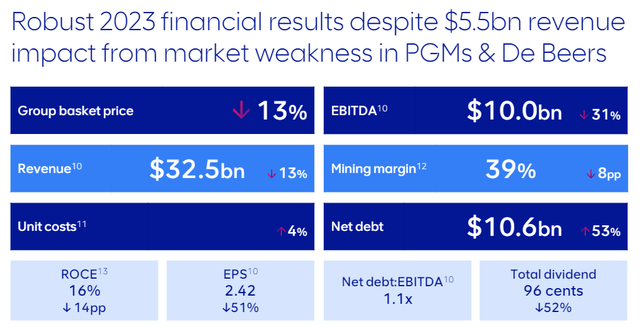

In our previous estimates, we forecasted a 2023 EBITDA of $10 billion with a net debt of $11 billion. Our estimates, aligned with Anglo American’s payout, show a DPS set at $0.95 for 2024. Looking at the final company’s FY 2023 results, we were very accurate (Fig 1). We were slightly above net debt evolution and forecasted a 1-cent lower dividend per share.

Anglo American FY 2023 Financial Results in a Snap

Source: Anglo American FY 2023 results presentation – Fig 1

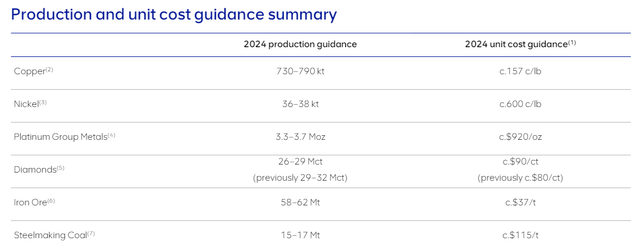

Here at the Lab, we positively view Anglo American Q1 performance (Fig 2); guidance was left unchanged, excluding DeBeers. In detail, below are the latest commodity MIX sub-results:

- Copper: Quellaveco Expansion Is Delivering, and copper production increased by 11%. Shipments were in line with our estimates. The company’s 2024 unit cost guidance remains approximately 157c/lb, and the Quellaveco mine is expected to reach a production of roughly 600 kta per year;

- The steelmaking coal division increased its output by 7%, supported by Capcoal and Aquila operations;

- Iron ore production was flat. Anglo-American had logistics constraints that offset Kumba output; however, the company recorded a solid performance from the Minas-Rio mine;

- Going to the negative parts, diamond and Platinum Group Metals (PGMs) output decreased by 23% and 7%, respectively. In our previous report, we anticipated a diamond market normalization after H2 2023. We reported our pessimistic assumption and decreased the Diamond division book value to $6 billion. This is a production report; therefore, we do not have any balance sheet figures; however, the company increased the Diamand Unit Cost guidance by $10/ct from $80/ct to $90/ct. In addition, we believe Anglo will limit the production to market down inventory levels.

Anglo American production and cost guidance

Source: Anglo American Q1 Production Report – Fig 2

Copper and coal are well-performing, with unit cost guidance unchanged ex-diamonds. Given the recent copper price development, we anticipate positive Q2 and Q3 results. According to our estimates, considering a higher cost of diamonds, the division EBITDA might be impacted by approximately $766 million; however, adjusting our future estimates on a higher copper price, we increase our copper EBITDA division by $800 million. Therefore, the two one-offs almost counterbalance thanks to the Anglo-American diversified earnings approach. Looking at the numbers, in our estimates, Anglo-American’s copper operations account for nearly 40% of the company’s total EBITDA.

As mentioned, “this segment is worth approximately $21 billion with a $35k/t annual capacity. In number, this is about 72% of Anglo’s current market cap.” Q1 copper production release will positively impact the company’s earnings growth and consensus forward estimates. In addition, there was an unexpected tightening in the global copper mine supply. In Q1 2024, First Quantum’s mine was closed, and around 4 million tonnes of capacity was removed. This is coupled with a growing Chinese copper demand, particularly for EV production and green energy transition.

For this reason, even considering higher costs for Diamonds and higher realized price in Copper, we confirm an Anglo-American 2024 EBITDA of $10.6 billion, with operational performance upside supported by CAPEX savings and complexity reduction.

Valuation

In our numbers, considering the dividend payment, the company is already ex-dividend by mid-March, and we arrive at a year-end net debt of $11.2 billion. Compared to our estimates, the company trades at 3.6x EV/EBITDA from a valuation standpoint. This is lower than the Anglo-American historical five-year average of 4.9x. Today, we confirmed our £28 per share overweight target, supported by an EV/EBITDA of 4.5x.

Risks

Downside risks include FX and commodity price changes. In addition, the sector is exposed to financial, political, and operational risks. Ninety percent of the company’s mines are located in Emerging Markets such as South Africa, Chile/Peru, Brazil, and Botswana/Namibia. As a reference, Ghana ordered miners to sell 20% of refined gold to its Central bank. We also see execution risks on the Woodsmith fertilizer project, with an indicative annual CAPEX of $1 billion until 2027.

Conclusion

Despite accounting for lower earnings on the Anglo Diamonds division, the company has upside potential for copper price realization. On a long-term expectation, this is mainly supported by higher product demand. In the short term, Anglo will likely be facilitated by the closure of the Panama mine. The company’s valuation is attractive, and following the Q1 production report, we confirm our buy rating.

Editor’s Note: This article discusses one or more securities that do not trade on a major U.S. exchange. Please be aware of the risks associated with these stocks.

Read the full article here

Q1 2024 Earnings Call Transcript")