Q2 2024 Earnings Call Transcript")

")

Alibaba (NYSE:BABA) (OTCPK:BABAF) stock has failed to show a strong bullish momentum over the last few quarters. Despite the rock-bottom valuation, the stock has failed to impress Wall Street. The recent quarterly earnings show a possible silver lining which can turn the sentiment toward the stock. In the recent quarter, Alibaba reported 45% YoY revenue growth in its International Digital Commerce Group. The revenue increased from RMB 18.9 billion in the year-ago quarter to RMB 27.5 billion in the recent quarter. On the other hand, consolidated revenue growth was only 7%. In the previous article, the potential improvement in cloud business was mentioned. Alibaba has reported 45% YoY EBITA growth in the cloud segment, which increases the annualized EBITA to $800 million.

Over the last two years, International commerce revenue has almost doubled, from RMB 14 billion in the March-ending quarter of 2022 to RMB 27.5 billion in the recent quarter. This has increased the revenue share of this segment from 6.5% to 13%. At the current growth rate, international commerce should contribute close to 25% of the total revenue by the end of 2025. Rapid growth in international business is a good hedge against the current geopolitical tensions. It also gives the company a good growth runway to expand in different geographies.

The loss in International Commerce segment doubled from RMB 2.1 billion in the year-ago quarter to RMB 4 billion in the recent quarter. However, this increase in loss is mostly due to higher investment rate in its international operations. A higher international revenue base helps increase the footprint of Alibaba’s profitable cloud business. With the massive cash reserves available to the company, it has a big advantage in several international regions where it is competing with smaller competitors. Alibaba stock is quite cheap when we look at the fundamentals and the strong growth potential in the international business, which reduces the domestic risk and increases the diversification.

International commerce can change the sentiment

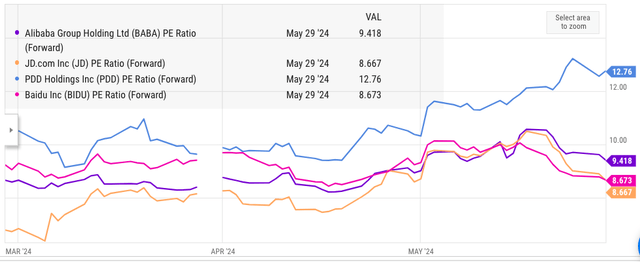

YCharts

Figure: Comparison of Alibaba’s PE ratio with other Chinese stocks. Source: YCharts

We can see from the above chart that Alibaba along with other major Chinese stocks have a very low forward pe ratio. In comparison, US tech companies like Apple (AAPL), Alphabet (GOOG), and Meta (META) have a forward pe ratio of 25 to 30. At its peak, Alibaba’s PE ratio was close to 30 during the second half of 2020. A rapid international expansion could boost Alibaba’s forward pe multiple to above 20. Higher profitability in cloud, local services, and other segments should also help in improving the EPS trajectory, giving the stock a strong upside potential.

The current bearish sentiment towards Alibaba and other Chinese stocks is largely due to geopolitical tensions. However, Alibaba’s international commerce business has the potential to change the sentiment towards the stock. Over the last two years, the revenue base of this segment has doubled, which has increased the revenue share of this business to 13%. Almost 65% of the overall YoY revenue growth in the recent quarter came from Alibaba’s international commerce business. This shows the importance of this segment for the company.

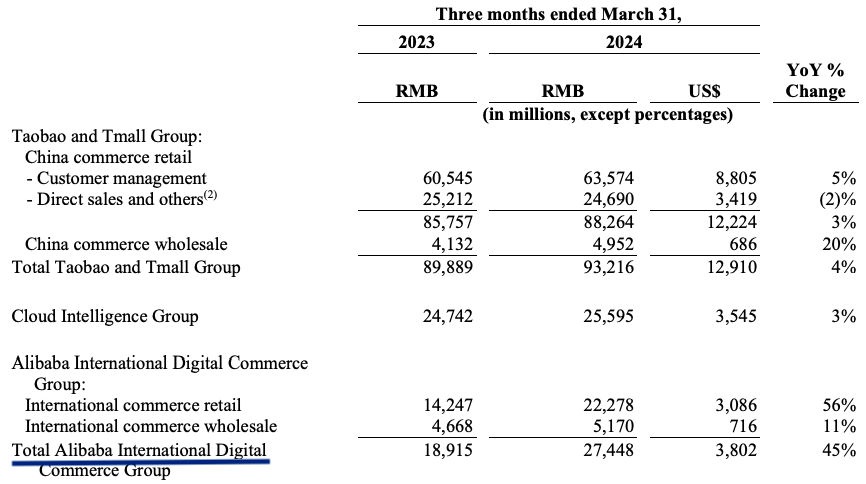

Alibaba Filings

Figure: Rapid growth in International Commerce business. Source: Alibaba Filings

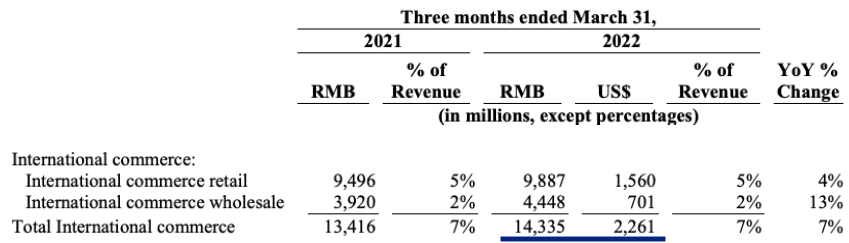

Alibaba Filings

Figure: Alibaba’s international commerce group two years back. Source: Alibaba Filings

We can see from the above image that Alibaba has delivered rapid growth in its international business over the last two years.

Alibaba has a big stake in several international e-commerce companies. One of the most successful is Turkey’s leading e-commerce company Trendyol in which Alibaba has over 85% stake. Trendyol had received $16.5 billion valuation back in 2021. In 2023, Alibaba announced another $2 billion investment in this company to expand its business in the region. Alibaba has also injected over $600 million into Lazada as it battles competitors in Southeast Asia.

These investments come at the cost of higher losses. Alibaba’s losses in international business have doubled in the last year and have increased to $566 million in the recent quarter. The international segment is now the biggest loss-making segment for the company.

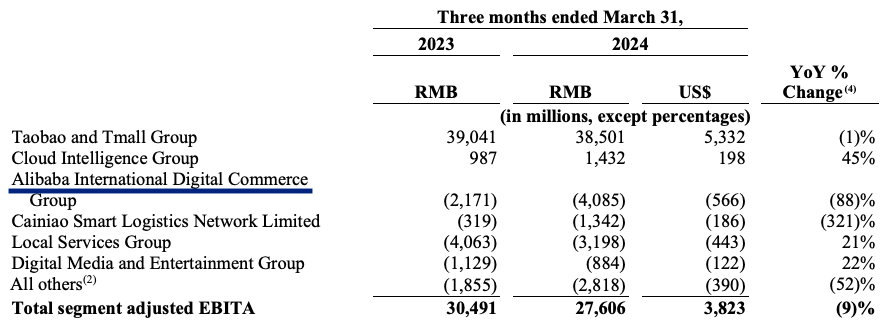

Alibaba Filings

Figure: Alibaba’s EBITA in international commerce and other segments. Source: Alibaba Filings

However, Alibaba has deep cash reserves, and it can easily burn more cash than most international competitors. We have recently seen the management announce another big buyback program of $25 billion. This shows that Alibaba can easily absorb the current annualized loss rate of $2 billion in the international segment.

Road to 25% revenue share

It is very important for Alibaba to diversify its revenue base. This allows the company to hedge against some of the geopolitical risks and also helps build a longer growth runway. The e-commerce business in China is quite mature, and it would be difficult at Alibaba’s scale to deliver double-digit growth in China. On the other hand, many international regions where Alibaba is expanding are relatively underpenetrated in terms of e-commerce. They also have lower competition, which helps Alibaba gain a higher market share.

Alibaba has been able to report 40%-50% YoY revenue growth in the international commerce segment for the last few quarters. If Alibaba can continue to deliver the current growth momentum in international commerce, then this segment should have a revenue share of 25% by the end of 2025. This could lead to a massive shift in how Alibaba is perceived by Wall Street. It should be noted that International Commerce segment shows the revenue from only e-commerce operations. Alibaba has a thriving cloud business in many international locations. Hence, the overall revenue from international operations is bigger than the core international commerce group of the company.

Moving away from geopolitical tensions

Recently, Geneva Investor published a thesis that states that Alibaba is simply uninvestable due to geopolitical tensions. The risk in Alibaba and other Chinese stocks has certainly increased due to the recent tensions. However, investors need to look closely at the risk-return dynamics in the current situation. Bloomberg has recently published an article which states that any invasion of Taiwan will likely have a bigger impact on global economy compared to the Great Recession of 2007-2008. If there is an escalation, investors would need to reassess their entire portfolio and not Alibaba or any single stock held by them.

As an example, Apple received 16% of its total revenue from China and any escalation will certainly hurt its sales in the region as well as the entire supply chain. There are a vast number of companies that rely on supply chain from Taiwan and China. Any major disruption will likely cause a massive pullback across many sectors.

As mentioned above, the recent growth of international commerce should also be a good hedge, as Alibaba is seen more as a global business instead of a China-centric company.

Risks to the thesis

Alibaba is expanding rapidly in international regions. However, it is possible that it might face pushback from regulators in several regions. We have already seen new EU rules regarding data protection and anti-dumping rules, which are mostly aimed at Chinese companies. India has also taken a tough stance against Chinese companies after a border dispute between the neighbors. This has led to Alibaba selling its stakes in a number of startups in India and reducing its presence.

While Southeast Asian countries, Turkey, Latin America, and several other regions are more eager to attract investments from Alibaba and other Chinese companies, this trend could certainly change according to geopolitical relations. We have already seen how geopolitical tensions can cause rapid deterioration of business opportunities.

If Alibaba fails to maintain the current growth trajectory in international commerce, it will lead to a big change in the projected revenue share of this segment. Alibaba is on pace to reach 25% revenue share for its international commerce business by the end of 2025. However, investors would need to closely watch the geopolitical trends and growth trends of Alibaba in different segments in the next few quarters.

Impact on Alibaba stock

Alibaba’s management has taken several steps to improve the growth momentum in international business. It has a massive cash pile and free cash flow which can be used to support the international investments. Alibaba is also investing heavily in rewarding investors through cash buybacks and dividends. The company bought back $4.8 billion worth of stock in the first quarter. This equates to about 2.5% of outstanding stock in a single quarter, or 10% on an annualized basis. In addition to this, the company has a healthy dividend yield. The current buyback program and free cash flow can sustain these buybacks for a number of quarters. We should see a rapid EPS growth trajectory over the next few quarters, which should be a tailwind for the stock sentiment.

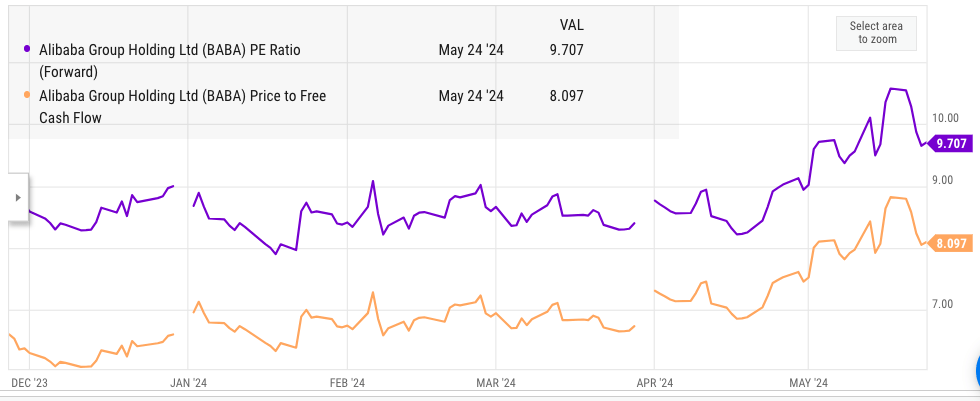

YCharts

Figure: Alibaba’s forward PE ratio and Price to FCF ratio. Source: YCharts

Alibaba’s forward PE ratio and price-to-FCF ratio are less than 10. The company has strong fundamentals and it is showing rapid geographic diversification. If the current trend of higher YoY international growth continues for the next few quarters, Wall Street could gain a much better favorable view of the company and its future growth potential.

Investors looking for a modestly priced stock with a good moat can take a look at Alibaba. While there are certainly geopolitical risks associated with Alibaba, the company has strong fundamentals and is showing rapid geographic diversification, making its current valuation look attractive.

Investor Takeaway

Alibaba is rapidly expanding in international regions. It has doubled the international revenue in the last two years and the revenue share of this segment is now at 13%. At the current growth trend, international commerce segment could have a revenue share of 25% by the end of 2025. This should provide the company with a good hedge against geopolitical tensions and also a better growth runway.

The massive investments in international regions have led to a higher loss in this segment. However, Alibaba has deep cash reserves, and it could sustain this burn rate in order to gain higher market share in key international regions. The stock is quite cheap because of the regulatory and geopolitical headwinds. But we could see a much more diversified company over the next few quarters, which can help improve the sentiment around the stock and drive a good bullish rally.

Read the full article here

Q2 2024 Earnings Call Transcript")

")