")

")

(NASDAQ:ZS)")

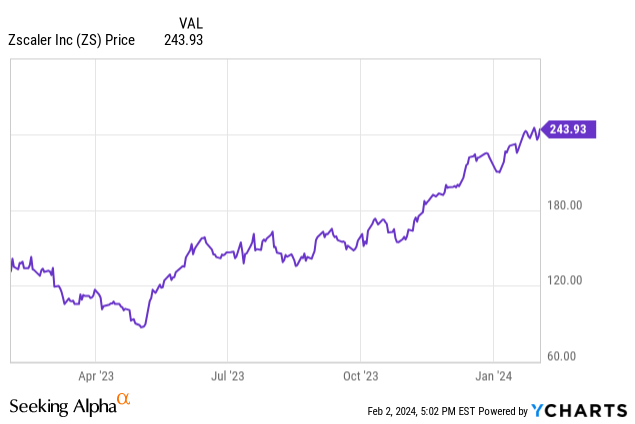

Though many tech stocks have lost their luster in the wake of the post-pandemic era, Zscaler (NASDAQ:ZS) has long remained a Wall Street favorite. This cybersecurity company – one of the leading vendors that secures cloud-based applications from cyber threats – has seen its share price surge nearly double over the past year, and in the year to date, Zscaler is up 15% already.

Given the strong gains this stock has enjoyed in recent times, it’s a great time for investors to re-assess the risk-to-value proposition here.

Zscaler’s steam is running out, especially at such a high share price

I last wrote a bullish article on Zscaler in September, when the stock was trading closer to $150 per share. Though I’ve enjoyed the massive gains in my position since then, I’m now dropping my rating on the stock to neutral.

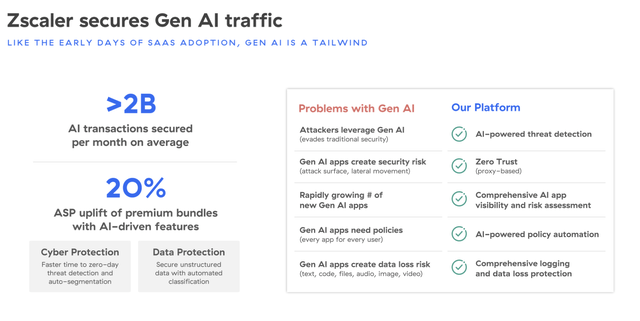

To back up here: a lot of the recent enthusiasm in Zscaler’s stock is driven by the company’s continuation of ~40% y/y revenue growth rates, backed up nascent opportunities in generative AI technology.

Zscaler’s thesis is that many enterprise organizations are beginning to explore generative AI technologies and giving them access to internal applications and databases, leaving them exposed to potential data breaches. The slide below showcases how Zscaler addresses some of these threats:

Zscaler AI offerings (Zscaler Q1 earnings deck)

In my view, however, Zscaler’s recent rally already bakes in a lot of this upside. The next big catalyst for Zscaler is its fiscal Q2 (January quarter) earnings release on February 29.

On top of expected deceleration in top-line growth throughout the remainder of FY24, I’d recommend locking in gains here and moving to the sidelines before Zscaler posts what I believe to be a deflating, “sell the news” earnings cycle.

Valuation update: too rich for decelerating growth

At current share prices near $245, Zscaler trades at a market cap of $36.19 billion. After we net off the $2.32 billion of cash and $1.13 billion of convertible debt on Zscaler’s most recent balance sheet, the company’s resulting enterprise value is $35.00 billion.

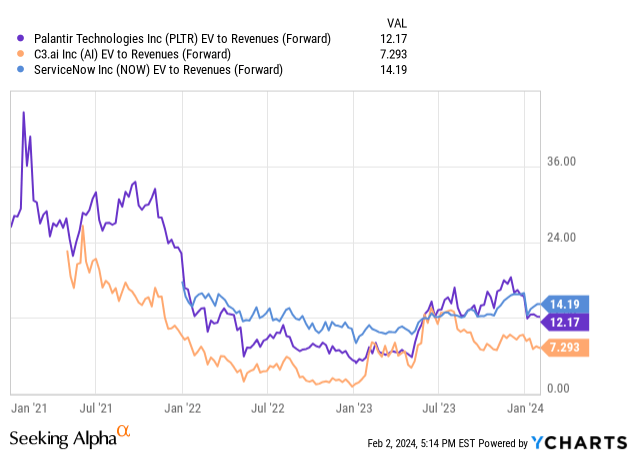

Meanwhile, for next fiscal year FY25 (the year for Zscaler ending in July 2025), Wall Street analysts are expecting the company to generate $2.62 billion in revenue, representing a deceleration to 25% y/y growth. This puts Zscaler’s valuation at an astounding 13.4x EV/FY25 revenue.

This multiple vaults Zscaler near the top of several high-growth, mid/large-cap software peers that are also riding gen AI tailwinds:

While I don’t necessarily think there is substantial downside for Zscaler given the company still delivers incredibly impressive fundamentals (an amazing balance of growth + margin, with a “Rule of 40” score near 60), I think the recent rally gives us a great chance to take profits and wait until Zscaler sinks back down closer to a 10x FY25 revenue multiple – implying a $185 price target and ~25% downside from current levels.

Most metrics pointing to deceleration

Zscaler’s huge valuation multiple, meanwhile, relies heavily on its ability to sustain premium growth rates. The company, meanwhile, is becoming a victim of its own scale – and growth rates will come down.

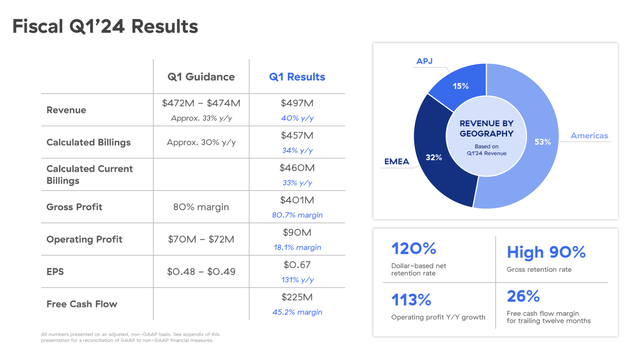

In Q1, Zscaler was still able to grow revenue at a 40% y/y pace, as shown in the snapshot below:

Zscaler Q1 highlights and billings deceleration (Zscaler Q1 earnings deck)

But at the same time, current billings growth decelerated to 33% y/y (from 38% y/y in Q4). And as seasoned software investors are aware, billings is a better representation of a company’s longer-term growth trajectory as it captures deals signed in the quarter that won’t be recognized as revenue until later quarters.

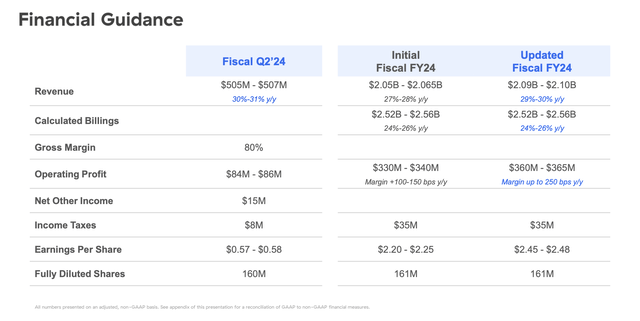

Zscaler’s own guidance for Q2, meanwhile, indicates that top-line growth will decelerate to the low 30s by next quarter:

Zscaler Q2 guidance (Zscaler Q1 earnings deck)

It’s worth noting as well that while Zscaler boosted its FY24 revenue outlook, it held its full-year billings guidance flat. Challenged on this aspect on the Q&A portion of the Q1 earnings call, CFO Remo Canessa answered as follows:

Great question. So I mean the guide that we gave is solely related to basically the go-to-market with our new sales leadership on board. We feel it’s prudent to do that. When you take a look at close rates for Q2 this year versus last year, we’re being a little more conservative with our close rates this Q2.

From a market – overall market perspective, the macro still remains challenging, but we feel that things – that there’s more of an acceptance to Zero Trust, there’s more of an understanding of our platform. So we feel good.”

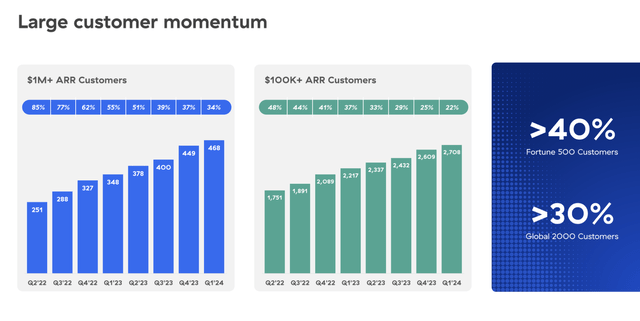

It’s worth noting as well that Zscaler’s growth in large customer counts is also decelerating.

Zscaler customer trends (Zscaler Q1 earnings deck)

In the $1M+ ARR bucket, growth slowed down to 34% y/y, from 37% y/y in Q4. The company added only 19 net-new >$1M customers in the most recent quarter, versus 49 in Q4 and 22 in Q3. Similarly, in the >$100k bucket, growth slowed from 25% y/y in Q4 to 22% y/y in Q1.

Margins remain healthy, of course – Zscaler’s pro forma operating margin of 18% in Q1 rose 6 points y/y from 12% in the prior-year quarter, and stacked on top of a 40% y/y revenue growth rate still puts the company well above the “Rule of 40”. But I do think enthusiasm for Zscaler will compress as growth rates come down.

Key takeaways

In my view, Zscaler has reached a near-term crest (and in fact, I’m concerned about recent records on the broader market indices as a whole). With the stock market expensive in the wake of still-high interest rates, I’d be nervous about continuing to hold onto Zscaler shares at such a premium valuation. It’s time to take gains here and move to the sidelines.

Read the full article here

")

")

")