")

")

")

Summary

Following my coverage of Zoom Video Communications (NASDAQ:ZM), for which I recommended a hold rating as I did not see any signs of growth recovery in the near term due to weaker demand from SMBs (due to them shutting down) and sales cycle normalization, this post is to provide an update on my thoughts on the business and stock. I remain on the sidelines (hold-rated) for ZM as the macro situation is still unfavorable towards ZM. I acknowledge the underlying growth drivers—Zoom Phone and Zoom Contact Center—that ZM has, and they are certainly doing well. However, until headline growth starts to show better numbers, I just don’t see how the stock will work in the near term (the stock pretty much sidelined for the past 12 months).

Investment thesis

While management has raised its FY24 guidance, from the recent 3Q24 performance, I can tell that ZM is still facing headwinds from the macroclimate. Revenue growth continues to decelerate for the 8th straight quarter, growing only by 4.9% in 3Q24. In addition, the reason behind the weak total deferred revenue guide (-6% to -8%) is another crucial piece of evidence that customers are still holding back on spending. Specifically, customers are trying to manage their cash to take advantage of an environment with high interest rates, which is why billing frequencies on enterprise deals are decreasing.

For Q4, we expect deferred revenue to be down 6% to 8% year-over-year, partially driven by shorter billing frequencies on Enterprise deals arising from the high interest rate environment. 3Q24 earnings call

I might be oversensitive on this, but the bigger implication from this is that it suggests enterprises are not in a hurry to adopt ZM’s product offerings (they clearly value cash interest more than investing in growth-oriented ZM products). An additional factor contributing to the weak deferred revenue guide, which indicates a weak spending environment, is the fact that contract renewals are being received with lower sales value.

we anticipate that as we get through the end of this year, we’ve moved through most of those transitions where organizations have done their own reductions and are aligning their licenses to that. 3Q24 earnings call

This is because customers are downsizing their contracts due to layoffs. Aside from the obvious impact that this will have on growth, my concern is that there might be more contract renewal headwinds coming ahead – ZM is going to see peak contract renewal season in 1CQ2024 which, based on the recent trends, suggests that these contracts are going to be renewed at lower value as businesses have lesser need after the layoffs.

So the other thing, as a reminder, right, we’re going to have a big renewal cycle in Q1, and then that’s the peak. 3Q24 earnings call

. If my assumption is right, near-term renewals should be negative for growth due to the downsized contracts. This contract renewal headwind should also continue to pressure the NRR (net retention rate) for Enterprise customers (which declined from 109% in 2Q24 to 105% in 3Q24). The news that Fed is going to cut rate in 2024 is surely positive for ZM as the cost of doing business is now lesser, which means businesses can now afford to hire more employees for growth. However, I don’t think the impact will be immediate as businesses are likely to remain cautious and hold on to cash (ensure a strong balance sheet) until the economy outlook is clearer.

So anywhere from one just kind of five years. So average ends up being around 3. So I mean the reality is we know that the majority had the opportunity to renew in FY24. 26th Needham Growth Conference

That said, there are 3 aspects of ZM business that I think have potential to help ZM cushion this macroclimate: Zoom Phone and Zoom Contact Center. Zoom Phone is still a significant growth driver for the company, which is strategically concentrating on upselling Zoom platforms with bundled products. For context, management reported a 330% year-over-year increase in the number of Zoom One bundle users, including phone users. Bundling works very well for ZM because it significantly elevates the customer experience as a whole (the bundle includes features like a whiteboard, scheduler, phone, and chat). The overall impact is that it helps improve customer retention and push ZM deeper into the operational workflow processes of its customer base. Humans are habitual creatures; the more they use ZM, the more familiar they are, and the less likely they are to switch solution providers. Zoom Phone should continue to see traction as ZM has the intention to roll out a down-market phone offering, further lowering the adoption barrier. As for Zoom Contact Center, as of 3Q24, it has reached around 700 customers, which is 40% sequential growth (200 additions from 2Q23), and Zoom Virtual Agent customers nearly doubled quarter over quarter. I believe ZM’s decision to roll out this product is timely, as a lot of companies are looking to reduce costs (especially with the high wage environment), and one apparent way is to outsource contact centers. And the reason ZM is able to win market share, in my opinion, is because it has a large customer base that is already using some of its products. This makes it easy for ZM to bundle everything together at a lower price to encourage customers to use them.

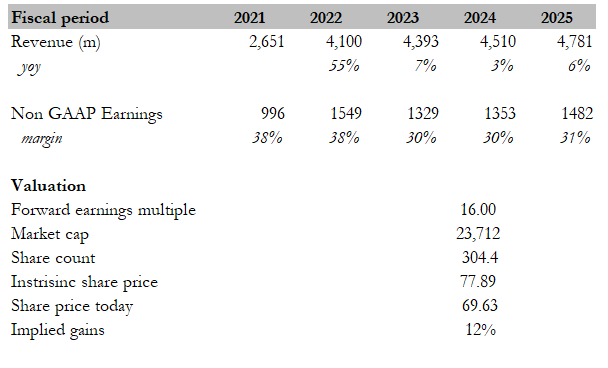

Valuation

Own calculation

My target price for ZM, based on my model, is ~$78. My revised assumptions are as follows:

- FY24 should grow by 3% instead of my prior 2%, reflecting management’s FY24 new guidance.

- FY25 growth is adjusted upwards by 100 bps to reflect the 100 bps better-than-expected performance. I continue to expect growth recovery in FY25 as the macro situation should stabilize, and ZM has two growth-driving products.

- Earnings margins remain flat in FY24 as growth is modest, but FY25 should see some form of margin expansion as revenue growth recovers.

My valuation methodology for ZM is still to compare ZM against the broader market (SPX index) because there are not enough listed peers that are direct competitors. The ratio between ZM and the SPX index has seen a downtrend ever since ZM growth started to slow, touching 0.73x today. As I expect growth to recover back to mid-single-digits, this ratio should see some form of recovery too. The last time ZM was growing at mid-single digits, the ratio was around 0.8x. Attaching that 0.8x to the current SPX multiple (20x forward PE), ZM should trade at 16x.

Risk

Whatever product growth drivers ZM has today may not impact the stock price at all if the overall macro situation gets worse. This is because the market is going to price in further demand deterioration, which will further erode deferred revenue growth, cause further NRR compression as contract renewals come up, and ultimately impact headline growth figures.

Conclusion

My hold recommendation stays for ZM. While Zoom Phone and Zoom Contact Center show promise, the macroeconomic climate remains a significant burden. In particular, the weak total deferred revenue guide and contract renewals with lower sales value and downsized contracts are indicators of weak growth in the near-term.

Read the full article here

")

")

Stock: A Quantum-Ready Company")

")