")

Q4 2024 Earnings Call Transcript")

")

")

Zentalis Pharma (NASDAQ:ZNTL) took the strategic decision of shelving its oral SERD and EGFR inhibitors because, one, Radius and Menarini’s first oral SERD was soon to be approved, and two, the EGFR market is highly competitive. It focused on ZN-c3 and ZN-d5; d5 has commercial competition in its mechanism of action but not in its target indication. C3 is the lead candidate, and AstraZeneca’s exit from the WEE1 space – even if not the entire synthetic lethality space – has left ZNTL as the market leader, although with claimed differences with AZN’s drug that could potentially help ZNTL.

I covered Zentalis Pharma many moons ago – Nov 18, 2020, to be precise – and a lot has changed at the company, except that it is still a clinical stage company. Four years ago, its lead candidate was ZN-c5, an oral selective estrogen receptor degrader in phase 1/2 for metastatic breast cancer. Today, its lead candidate is ZN-c3, or Azenosertib, an inhibitor of WEE1, a protein tyrosine kinase, which, in 2020, was in a Phase 1/2 trial targeting advanced solid tumors. Today, its lead program is platinum sensitive ovarian cancer, 1st line setting. Like I said, a lot has changed. ZN-d5, which used to show up as a phase 1/2 asset in AML or B-cell lymphoma as well as breast cancer, shows as a phase 1 asset in AML.

What happened with ZN-c5? In 2021, about mid-year, I note this asset producing thoroughly underwhelming data, with a clinical benefit rate of 40% and an ORR of 0% in early-stage trials for advanced or metastatic breast cancer. At that same time, azenosertib in its early ovarian cancer studies produced 5 partial responses in an early trial. This seems to have triggered a move away from ZN-c5 to ZN-c3, also known as azenosertib, the WEE1 inhibitor.

Cancer cells use WEE1 and another kinase to protect themselves against DNA damage. Therefore, inhibiting WEE1 in cancer cells in combination with DNA damaging agents makes these agents more cytotoxic, resulting in quicker apoptosis (cell death) of cancer cells. This concept is a form of synthetic lethality. This can not only inhibit tumor growth but potentially also stop the disease from progressing. The market leader in WEE1 inhibition is AstraZeneca’s adavosertib, which has gone through mid-stage trials and shown some promise. According to ZNTL, ZN-c3 “has advantages over other investigational therapies with superior solubility, selectivity, and PK properties.”

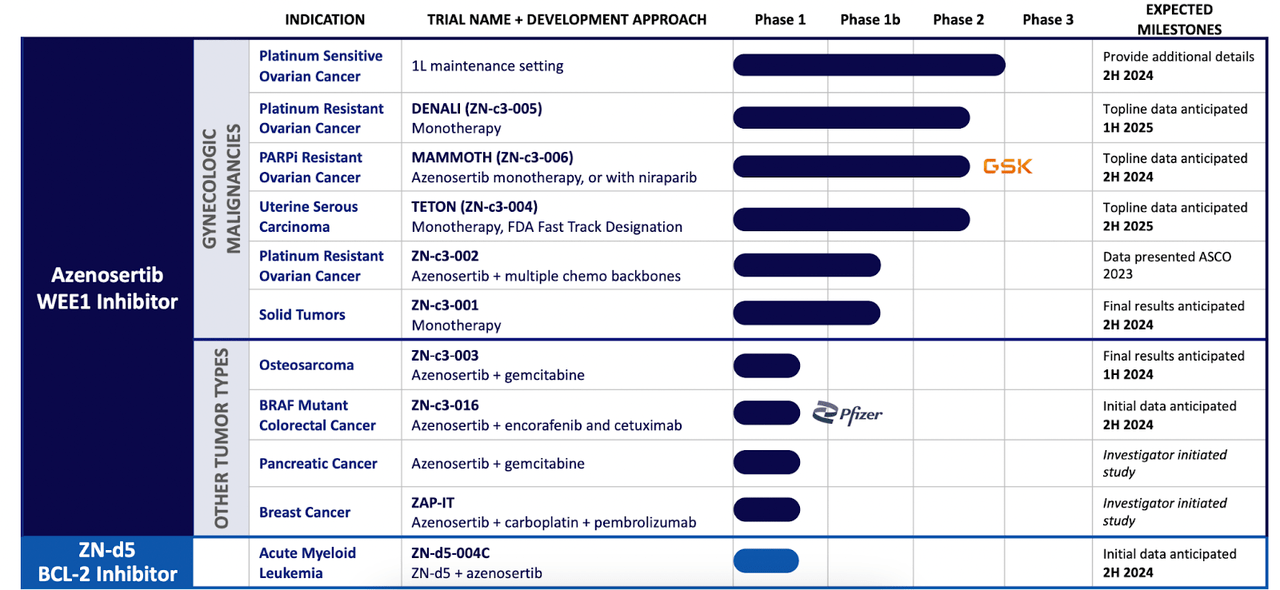

ZNTL PIPELINE (ZNTL WEBSITE)

Azenosertib is being run through 6 programs targeting various gynecologic cancers. These include platinum sensitive and platinum resistant ovarian cancers, the latter as both monotherapy and with multiple chemo backbones; uterine serous carcinoma, and as monotherapy in a basket of solid tumors. There are multiple data readouts planned in 2024. The company expects the first NDA in 2026. They have partnerships with GSK and Pfizer, although these are clinical partnerships.

About the GSK partnership begun in 2021:

Under the terms, Zentalis will be responsible for conducting the study, while GSK provides all required doses of niraparib. Zentalis retains full ownership of ZN-c3.

There is a large unmet need in treating advanced ovarian cancers with single agent chemotherapy. According to the company, two factors cause this unmet need:

-

Approximately 80% of women with advanced stage disease who respond to first-line chemotherapy will relapse

-

Single agent chemotherapy response for heavily pretreated platinum resistant/refractory ovarian cancer is 10-15%3

The above is stated for advanced ovarian cancer only. What we see here is that chemotherapy creates an unmet need in this cancer in both first line setting and as a single agent. If WEE1 inhibition can make chemo more effective, that would be a rather solid way to address an unmet need. The same is also true of uterine serous cancer, a highly fatal type of endometrial cancer, where too, single agent chemotherapy needs a boost.

I was wondering how a modality like azenosertib that works best with another DNA damaging agent would work as a monotherapy. The answer, as the company indicates, lies in the inherent genomic instability of certain cancers like ovarian and uterine serous carcinoma. Here, an outside DNA damaging agent like a chemo is not even needed because here cancer cells use WEE1 to protect against naturally occurring DNA damage. Even monotherapy WEE1 inhibition can prevent cancer cells from addressing DNA damage, which will then accumulate and cause apoptosis.

While azenosertib was being tested, it had its ups and downs. In 2022, after an early data drop on efficacy from a phase 1b trial in ovarian cancer using multiple chemo backbones, there was a 30% drop in the stock price after underwhelming ORR in the broad population. What the market ignored is the fact that in the paclitaxel combo group – in this heavily pretreated patient population – the ORR was a whopping 62.5%. There were also various cytopenia related adverse events, but one should not forget that these are associated with chemotherapy as well, especially in advanced stage disease.

This was borne out next year when the company released updated phase 1 data that showed:

When azenosertib was given with paclitaxel, the ORR was 50% and mPFS was 7.4 months. When given with carboplatin, the results were, respectively, 35.7% and 10.4 months.

Thus, azenosertib works well with both chemos. However, it definitely does not work with other chemo regimens, bringing the average down to just 37%.

We discussed the inconsequential GSK deal earlier. In mid-2022, Pfizer entered into a more substantial – although still very small – $25mn equity partnership with ZNTL in order to develop azenosertib. Zentalis retained full economic ownership and control of ZN-c3, though. In Q1 2023, the two companies started a “phase 1/2 dose escalation study of ZN-c3 in combination with encorafenib (sold as Braftovi by Pfizer), and cetuximab (marketed as Erbitux by Eli Lilly) – known as BEACON regimen – to treat patients with BRAF V600E-mutated metastatic colorectal cancer (mCRC).”

Another quick update is that, earlier, ZNTL had a somewhat shorter timeline for its phase 3 trial when they had plans to test azenosertib plus chemo in second line platinum sensitive ovarian cancer, or PSOC. Late last year, they moved away from that indication to 1st line maintenance therapy for PSOC, so the phase 3 trial, which was planned for early this year, will now be pushed to early 2025, with an NDA expected sometime in 2026.

Financials

ZNTL has a market cap of $820mn and a cash balance of $517mn. Research and development (R&D) expenses for the quarter ended September 30, 2023, were $46.8 million, while general and administrative (G&A) expenses for the quarter ended September 30, 2023, were $16.0 million. At that rate, the company has a cash runway of 8 quarters, or into early 2026. The company is well funded through data catalysts, and there should be no reason to dilute from a position of weakness in the stock price.

Bottom Line

ZNTL’s situation is a perfect example of “where angels fear to tread,” the “angel” in this case, obviously, being AstraZeneca, which let go of its own WEE1 program, instead choosing to go for ATR inhibition, a technology with a similar mechanism but with – AZN hopes – less side effects. ZNTL, on the other hand, says its molecule will have a better safety profile than AZN’s. All told, this is a “show me” situation and we will have to wait for data. There are one or two data catalysts this year, notably 3 topline data, one each for monotherapy, chemo and PARPi combos, which will help us figure out ZNTL better. Until then, a careful waiting approach sounds good to me.

Read the full article here

")

Q4 2024 Earnings Call Transcript")

")

")

")