")

")

")

(NYSE:BABA)")

")

I last wrote about Woodside Energy (NYSE:WDS) in May, when I upgraded the company on its valuation discount compared to international E&P peers. Since my article, Woodside’s share price has been slowly recovering until it announced on July 22nd that Woodside is acquiring Tellurian (TELL) for $1.2 billion in cash, including debt.

Combined with a negative cost update on the Scarborough project, investors punished Woodside’s shares heavily, sending it down 5% on July 23rd (Figure 1).

Figure 1 – Investors punished WDS shares on rising risks (Seeking Alpha)

Does the acquisition of Tellurian change my views on Woodside and is it still worth a buy?

In my opinion, Woodside is one of the few companies globally with the credibility and expertise to bring Tellurian’s Driftwood LNG to fruition. While the acquisition of Driftwood significantly increases Woodside’s financial risks, it also has large potential rewards, as Driftwood could catapult Woodside to be one of the largest LNG companies in the world.

Looking longer term, I continue to view Woodside as an excellent play on the LNG investment theme and would use the current stock weakness to accumulate shares.

Brief Company Overview

For those not familiar, Woodside Energy Group is Australia’s largest independent E&P company with a global portfolio of assets, including offshore LNG in Australia, oil in the Gulf of Mexico, and other exploration & development projects around the world.

Woodside first came to my attention when it acquired the petroleum assets of BHP Group (BHP) in 2021, roughly doubling the company’s production to roughly 187 MMboe in 2023. In the process, Woodside also expanded its U.S. investor base, as Woodside paid for the acquisition of BHP’s energy assets by issuing 915 million shares to BHP, which then transferred those shares to investors as a share dividend.

Deal Junkie Or Long-Term Vision?

Under chief executive Meg O’Neill, Woodside has been on an M&A spree in the last few years, keeping Aussie investment bankers busy. After completing the BHP energy acquisition, Woodside tried to acquire Santos Limited (ASX:STO), another large Australian independent E&P, in 2023. However, the two companies could not agree on valuations and the deal ultimately fell apart.

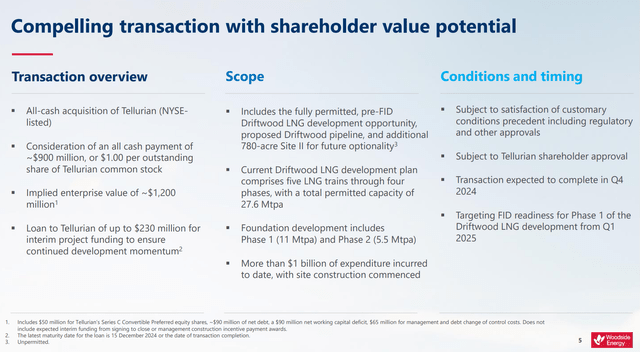

Barely 5 months after Woodside and Santos canceled their merger talks, Woodside announced on July 22nd (Australia time) that the company was acquiring Tellurian and its Driftwood LNG project. According to the company’s press release, WDS is acquiring all of the shares of TELL for $1.00 / share or ~$900 million in cash, plus the assumption of Tellurian’s debts (Figure 2).

Figure 2 – WDS/TELL acquisition overview (WDS investor presentation)

In addition, Woodside would loan up to $230 million to Tellurian for operating purposes until the transaction closes, sometime in Q4.

So who is Tellurian and is the Driftwood LNG project any good?

Driftwood Is A Great Project Stuck In An Under-Capitalized Vehicle

Tellurian is an LNG developer founded by Charif Souki, the charismatic but volatile natural gas pioneer. Mr. Souki was the co-founder and former CEO of Cheniere Energy (LNG), the first American LNG exporter. After a spat with corporate raider Carl Icahn, Mr. Souki left Cheniere and started Tellurian to develop the Driftwood LNG project.

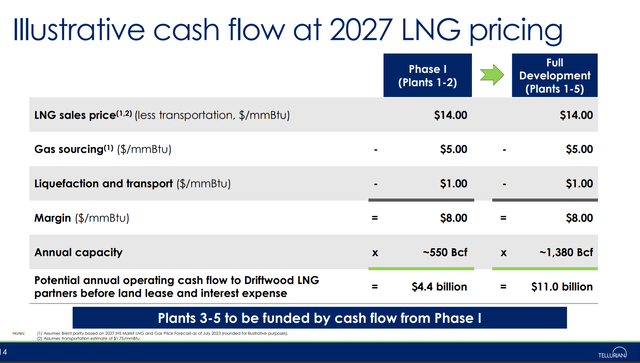

According to Tellurian’s historical presentations, the Driftwood LNG project is fully permitted for up to 27.6 million tpa in LNG export capacity. Assuming $14 /mmBtu pricing, Driftwood was envisioned to generate up to $11 billion in annual operating cash flows, assuming all 5 plants were constructed (Figure 3).

Figure 3 – Driftwood illustrative economics (TELL investor presentation)

However, the main issue with Tellurian and the Driftwood LNG project was the company’s lack of capital and inability to develop the Driftwood project on time.

Although the company had spent ~$1 billion developing Phase 1 of Driftwood, up to December 2023, the project was only ~30% complete. Furthermore, due to repeated delays and cost overruns, offtake partners like Gunvor canceled their contracts with Tellurian, leaving the company in limbo and the project’s future in doubt. Ultimately, this led to the ouster of Mr. Souki as the CEO and Chairman of Tellurian in December 2023.

Woodside Energy saw a great asset (Driftwood) sitting idle in a bad capital structure and pounced.

Combined Entity Will Be An LNG Behemoth

Driftwood is a logical acquisition for Woodside Energy, as Woodside is one of the few companies globally with the credibility and expertise to construct and operate complex LNG projects like Driftwood. Woodside has been operating offshore LNG projects in Australia since the 1980s with its North West Shelf project and is currently constructing the Scarborough LNG project.

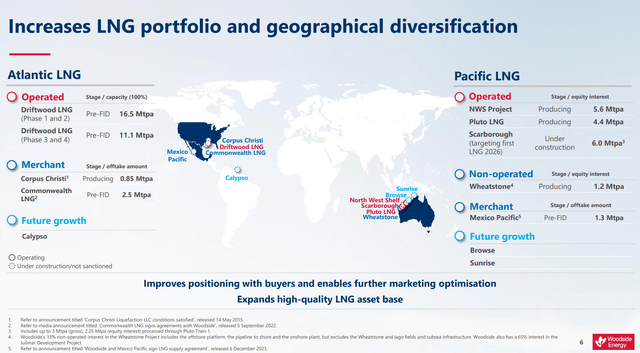

Combined, the addition of Driftwood could push Woodside’s LNG capacity to over 40 Mtpa (if Driftwood is fully developed) (Figure 4).

Figure 4 – Combined Woodside would be an LNG behemoth (WDS investor presentation)

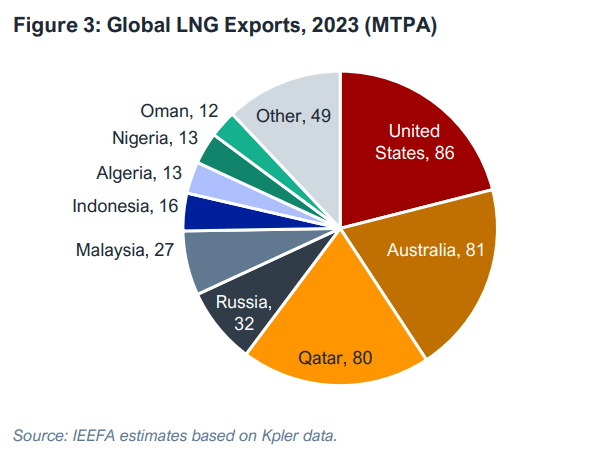

This would make Woodside one of the largest LNG producers in the world, on par with sovereign nations like Qatar and Russia (Figure 5)!

Figure 5 – Global LNG exports by country, 2023 (IEEFA)

Capital Is A Key Risk

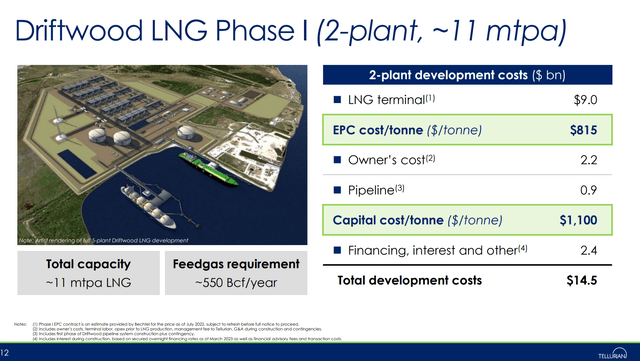

However, the addition of Driftwood is also increasing Woodside’s financial risk. This is because just Phase 1 alone was last estimated to cost $14.5 billion in August 2023 (Figure 6).

Figure 6 – Capital cost for Driftwood Phase 1 (Tellurian investor presentation)

Although Tellurian has claimed that most of the groundwork is complete, it is unclear how much additional capital needs to be spent. According to Woodside’s CEO on the M&A conference call, Woodside expects capital expenditures of $900-$960 / ton of LNG capacity, or an additional ~$10 billion that needs to be spent on Phase 1.

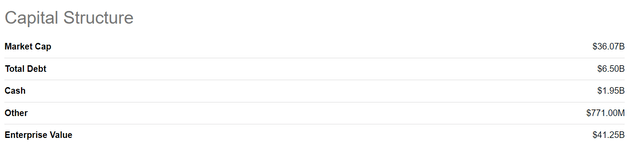

Even for a company of Woodside’s size, with an enterprise value of $41 billion, it is questionable whether Woodside can manage the full capital expenditures of Driftwood alone (Figure 7).

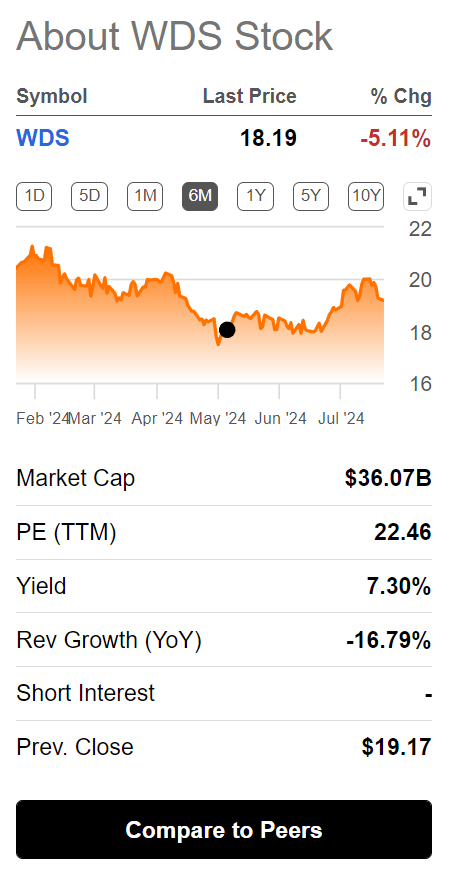

Figure 7 – WDS enterprise value (Seeking Alpha)

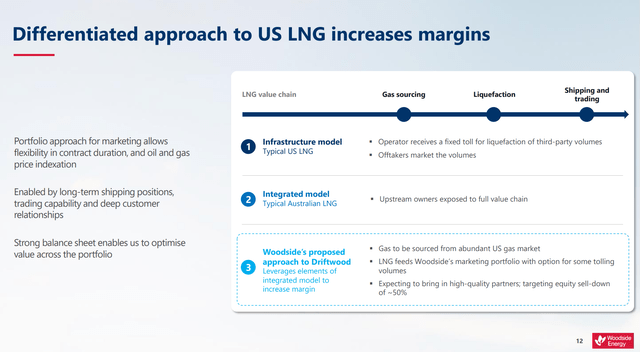

That is why Woodside has indicated that it expects to eventually bring in high-quality partners to take up to 50% of the equity in the Driftwood project, similar to how Woodside has financed its other projects historically (Figure 8).

Figure 8 – Woodside plans to bring in equity partners for Driftwood (WDS investor presentation)

Another risk is the potential dilution of Woodside’s capital returns. Historically, Woodside has targeted 12% internal rates of returns (“IRR”) when considering large-scale projects like Driftwood. Higher IRRs have favored the Australian integrated model, where the operator also owns the hydrocarbons being liquefied. However, the typical U.S. LNG project follows an infrastructure model where the operator receives a fixed toll fee from third-party volumes, which leads to lower risks but lower IRRs.

Woodside believes it can develop Driftwood on a hybrid model where gas is sourced from abundant U.S. supplies with limited use of tolling volumes. At this point, it is unclear how Woodside aims to achieve this ‘hybrid model’ and investors will have to wait for further clarity from management.

Is The Dividend Safe?

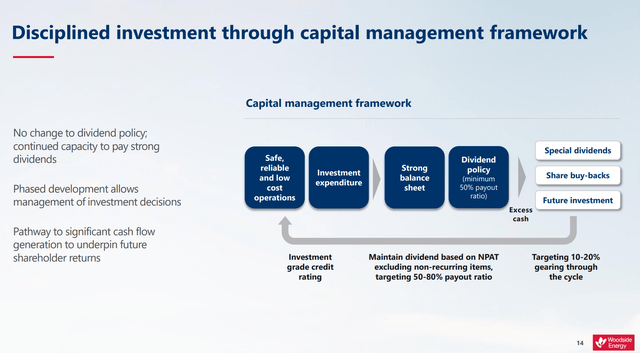

Historically, Woodside has a corporate policy of paying 50-80% of net profit after tax (“NPAT”) to shareholders as its dividend. However, in the last few years, this figure has been closer to 80% (Figure 9). Most recently, Woodside’s dividend amounted to $1.40 in the trailing 12-months, or a trailing 7.3%.

Figure 9 – WDS dividend policy (WDS investor presentation)

Given the demands on the company’s capital in the coming years to fund both Scarborough and Driftwood, investors may question whether Woodside’s dividend is safe.

Although management acknowledged that a strong dividend payout is an important element of Woodside’s investment case, they stopped short of promising to keep the dividend ‘safe’.

In my opinion, if push comes to shove and commodity prices show weakness in the coming quarters/years, investors should be prepared for a reduction in Woodside’s dividend in order to complete the construction of Scarborough and Driftwood without using excessive debts.

Scarborough Cost Overrun A Small Negative

Speaking of the Scarborough project, Woodside also disclosed a $500 million increase in the cost of the project on July 23rd. While this is a relatively small overrun in the grand scheme of things, it does highlight the inherent risks with multi-billion dollar capital projects.

Conclusion

For now, I remain constructive on Woodside. The acquisition of the Driftwood LNG project, while risky, could also cement Woodside’s position as the go-to stock for the LNG investment theme in the coming years.

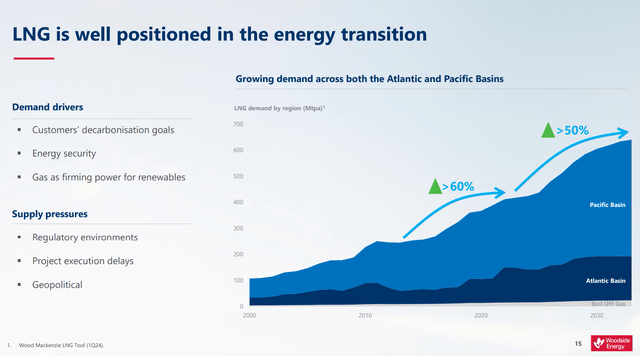

If we follow Ms. O’Neill’s vision, Woodside’s Scarborough (2026) and Driftwood (estimated 2029) LNG projects could come online just as demand for LNG surges across the globe over the coming decade (Figure 10).

Figure 10 – LNG is a transition fuel that is expected to see demand surge in the coming decade (WDS investor presentation)

I maintain my buy rating on WDS stock.

Read the full article here

")

")

")

(NYSE:BABA)")