")

")

")

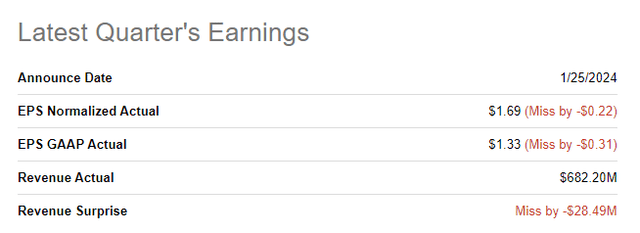

Western Alliance Bancorporation (NYSE:WAL) submitted its earnings card for the fourth-quarter on Friday and the regional bank slightly missed consensus estimates on both the top and the bottom line. The earnings report showed continual deposit gains and declining outstanding borrowings which have been a way for Western Alliance to grow its net interest income. With the Federal Reserve set to pivot in terms of benchmark interest rates in FY 2024 and short-term borrowings greatly reduced since Q1’23, I believe Western Alliance is set for headwinds in net interest income. Given that the bank’s price-to-book ratio has now almost fully revalued to its pre-crisis valuation, I believe the risk profile at this point is no longer attractive.

Previous rating

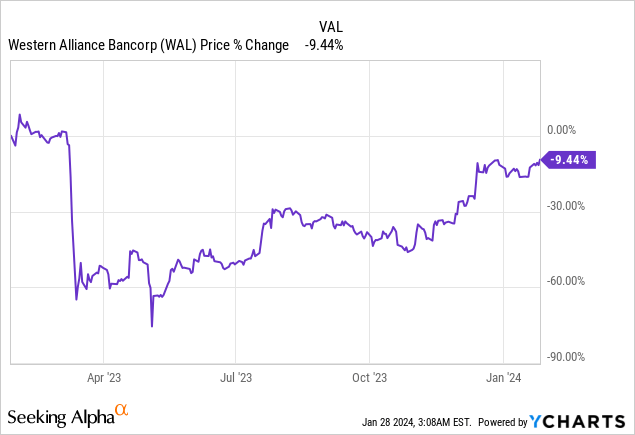

I started a position in Western Alliance after the collapse of Silicon Valley Bank — A 30%-Discounted Regional Bank Bargain — because I thought that the regional bank was uniquely positioned to benefit from a recovery in deposit balances, especially after the Federal Reserve stepped in and effectively backstopped deposits last year. My last rating on WAL was buy. Western Alliance, despite growing its deposits and reducing expensive short-term borrowings, now appears to be fully revalued, however, and I am changing my rating, after a 66% increase in the share price, to hold.

Western Alliance’s Q4’23 earnings takeaway: deposits up, borrowings down

Regional bank Western Alliance reported slightly weaker than expected earnings for its fourth quarter. The bank reported adjusted EPS of $1.69 per share which was $0.22 per share less than expected. Revenues came in at $28.5M below the average estimate.

Seeking Alpha

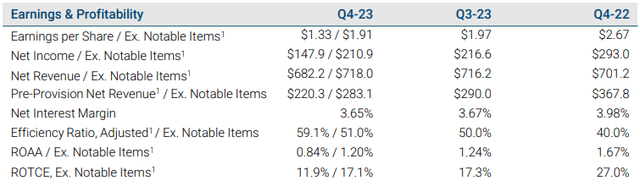

Overall, Western Alliance’s Q4’23 earnings card was not bad, despite the EPS and top-line miss. The regional lender achieved a fairly stable net interest margin and delivered an adjusted net income of $210.9M in the fourth quarter. What affected Western Alliance’s earnings in Q4’23 was the FDIC special assessment fee, in relation to the regional banking crisis in FY 2023, which lowered earnings by $66.3M. This was a one-time charge and should not be repeated in FY 2024.

Western Alliance

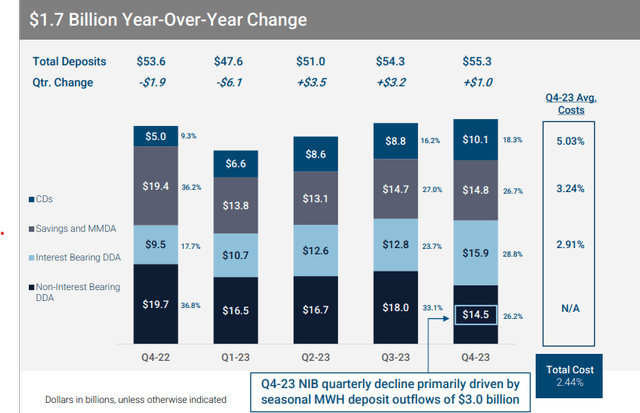

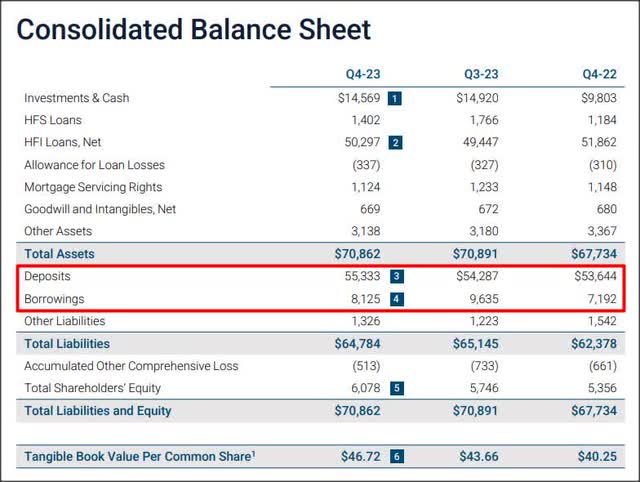

One major key takeaway from Western Alliance’s fourth-quarter earnings release was that the company continued to make progress in growing its deposits. The lender’s deposit balance now exceeds the pre-crisis level of Q4 2022 and it had $55.3B in total deposits on its balance sheet as of the end of the December-quarter, showing a $1.0B change Q/Q. The restoration of the deposit base was a key reason behind me initiating a position in the regional lender last year.

Western Alliance

At the same time that deposits went up, Western Alliance made continued progress in lowering its short-term borrowings. Western Alliance’s short-term borrowings ballooned upward to $16.7B in the first quarter of FY 2023 (+9.6B Q/Q) which was a direct consequence of the regional banking crisis that was triggered by the collapse of Silicon Valley Bank. However, the regional bank has made massive progress in terms of reducing these short-term borrowings which included funds from the Federal Reserve’s Bank Term Funding Program. At the end of Q4’23, these borrowings declined to $8.1B, showing a decline of $1.5B Q/Q. In 2024, I expect Western Alliance to further lower its outstanding borrowings to ~$7.0B (the pre-crisis level).

Western Alliance

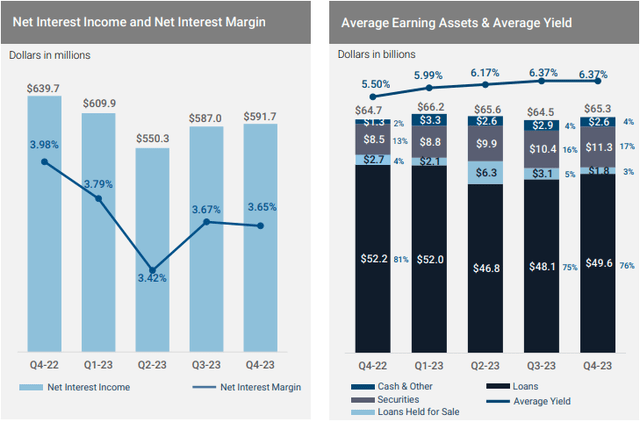

Although formidable pressure has emerged on banks’ net interest income and margin levels in recent quarters, in expectation of falling benchmark interest rates in FY 2024, Western Alliance’s net interest income increased quarter over quarter to $591.7M, showing an increase of $4.7M (+1% Q/Q). The increase in net interest income occurred chiefly due to Western Alliance removing, as just discussed, a high-cost funding source (loans under the Bank Term Funding Program) from its balance sheet. At the same time, Western Alliance benefited from a higher amount of interest-earning assets on its balance sheet which increased $0.8M in Q4’23 to $65.3M.

Western Alliance

Western Alliance is now likely trading at fair value

I recommended Western Alliance, the first time, in March 2022 as a direct bet on recovering investor sentiment and the possibility of a deposit base restoration. One key element of my early buy recommendation was that the lender’s valuation dropped way below its pre-crisis valuation last year, offering a contrarian opportunity at the time.

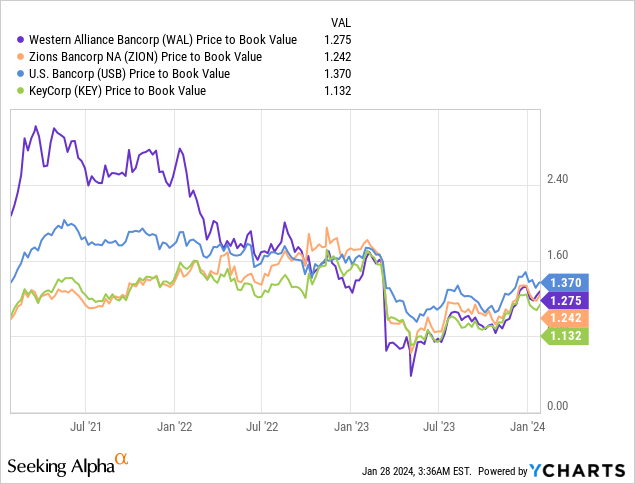

With shares of Western Alliance now almost having fully recovered to their pre-crisis valuation level, I believe Western Alliance no longer offers an asymmetric return profile. In July 2023, when investor sentiment started to recover after unprecedented Fed actions, the average 1-year P/B ratio was 1.25X which I said is a valuation range I am looking forward to return to (my fair value P/B ratio).

With a current book value premium of 28%, shares have achieved my valuation goal. As per Western Alliance’s latest earnings card, the regional lender had a book value of $52.81 per share at the end of Q4’23. Applying a 25% premium to this book value calculates to a fair value of $66. With the share price now being $67, I consider WAL fully priced and respond with a rating change to hold.

Risks with Western Alliance

The biggest risk that I see for Western Alliance in the short term is a cyclical contraction in its net interest income/margin which is going to be a weight for the regional bank’s valuation. Going forward, I see a risk of falling net interest income for Western Alliance, not only because the Federal Reserve is set to cut interest rates this year, but also because a driver of the bank’s NII growth has been the reduction in short-term borrowings. With borrowings close to being reduced to the Q4’22 level, I see little upside in Western Alliance’s net interest margin in FY 2024.

Final thoughts

Western Alliance submitted a strong earnings sheet for the fourth quarter, despite an EPS and top-line miss, which showed deposit growth momentum, but also declining short-term borrowings which have been a lever for the bank to grow its net interest income. Given that the Federal Reserve has guided for a pivot in its interest rates for 2024, Western Alliance should be expected to see growing pressure on its net interest income in FY 2024. The bank’s shares have soared 66% since my last coverage and since they have reached my fair value P/B ratio, I believe the upside here is limited.

Read the full article here

")

")