")

Fast food sales have been struggling for some time, as American consumers find themselves increasingly price sensitive and companies try to lure them back with special bargain meals after inflation convinced so many of them to change their spending habits.

Today, we’ll be looking at one of the biggest players in the American fast food market, The Wendy’s Company (NASDAQ:WEN), with an eye on their nearly 6% dividend yield. It’s nice when a recognizable brand pays out such a solid dividend. A particular focus will be on whether this dividend is sustainable, because if it is, it could be worth adding to an income portfolio.

Understanding Wendy’s

Wendy’s is the second largest hamburger-based fast food restaurant chain, or what they call “quick-service” in their SEC filings, in the United States. The basic setup of their restaurants should be immediately familiar to most people, without the need to go into a deep introduction of the sort of business they’re in.

The company is heavily North America-based, with over 6,000 restaurants in the United States. They have been trying to grow their presence overseas, with 1,210 restaurants in 32 foreign countries.

Those foreign sites are almost exclusively franchisees, with only a handful of company-run restaurants in the UK. Franchisees are a big deal in the United States as well, with just over 400 stores in their home country being operated by Wendy’s itself. Globally, 95% of all Wendy’s restaurants are operated by franchisees.

The company says it views its two key sources for growth as growing same-store sales and expanding its global footprint. With a limited presence overseas so far, the expansion of those sites could be a big opportunity, though it will cost money to establish more Wendy’s outlets all over the world.

High Debt: Looking at the Balance Sheet

|

Cash and Equivalents |

$498 million |

|

Total Current Assets |

$867 million |

|

Total Assets |

$5.19 billion |

|

Total Current Liabilities |

$425 million |

|

Long-Term Debt |

$2.73 billion |

|

Total Liabilities |

$4.90 billion |

|

Total Shareholder Equity |

$294 million |

(source: most recent 10-Q from SEC)

The most noteworthy part of Wendy’s balance sheet is the $2.73 billion in long-term debt. For a company that has total revenue of about $2 billion in sales per year, that’s an extreme amount of leverage, and the pricing is indicative of a company that would be experiencing substantial growth.

The price/book value of the stock at current prices is 12.45. That, again, is quite a premium, but really it is inevitable with so many of the company’s assets offset by debt.

The Risks

For me, the biggest risk, but by no means the only one, is the substantial debt. Just paying interest on the debt is going to be very limiting to Wendy’s working capital, and may end up hamstringing opportunities to expand their number of stores overseas, which by extension could be limiting their most obvious sources of growth.

Domestically, the risks to the company comes in no small part in the form of intense competition from other fast food outlets. In a time where consumers are more price sensitive and less inclined to heavily frequent fast food restaurants, Wendy’s may be forced to lower prices or at least limit price increases in the near future.

That could make them even more sensitive to the global and domestic economy. A weakened economy could be a further drag on sales, and new inflationary pressure could force them to face the prospect of having to increase prices, just at a time when it is least advantageous.

Inflation could make the costs of commodities increase, which could again force the company’s costs up, and force them to try to pass on the costs to their customers.

Operations and the Chances of Growth

|

2021 |

2022 |

2023 |

2024 (Q1) |

|

|

Revenues |

$1.9 billion |

$2.1 billion |

$2.2 billion |

$535 million |

|

Operating Profits |

$367 million |

$353 million |

$382 million |

$81 million |

|

Interest Expenses |

($109 million) |

($122 million) |

($124 million) |

($30 million) |

|

Diluted EPS |

89¢ |

82¢ |

97¢ |

20¢ |

(source: 10-K from SEC)

As you can see, annual revenue has been slowly increasing, and the estimates are suggesting that’s going to continue, with FY2024 revenue coming in at $2.25 billion and FY 2025 revenue estimated to be $2.34 billion. It’s growth, but not the level of growth which to me would justify the company at these substantial multiples to book value.

Once again, the high company debt is a big drag on the bottom line, with interest expenses usually coming in at around a third of the operating profits of the company. That’s going to continue going forward, with the estimates for earnings at $1.00 and $1.09, respectively.

Most recent earnings give us a P/E ratio of 18.36, and with the small growth, we have to look forward to according to the estimates, a forward P/E ratio would be 17.81. Those aren’t terrible ratios, but they aren’t really the sort of value play I would like to see.

The High Payout Rate

Wendy’s has been increasing its dividend in recent years, going from 12¢ per quarter in the second half of 2021, up to 12.5¢ in 2022, and 25¢ from 2023 on. This gives us a current yield of 5.61%, which would be really nice if it proved to be sustainable.

And that, I think, is a big question mark. We’re looking at a payout ratio in excess of 100%, which should immediately be a red flag. Now, the cash on hand would allow them to continue keeping up the payment if they so choose, but doing so would be hugely detrimental to their ability to invest in overseas growth. I don’t see them keeping the dividend up where it is, at least not indefinitely going forward.

Q2 Earnings

In the next couple of weeks, Wendy’s is going to be coming out with its second quarter earnings. The estimates are $577 million in revenue and earnings per share of 28¢. Recently, the estimates on earnings have been spot on, give or take a penny or two, so while the news is generally predicting industry weakness, I would expect the earnings to come in roughly in line with what we’re being told.

Conclusion

A dependable brand with a 5.61% dividend yield would be exactly the sort of thing I’d normally be looking for. That said, I just don’t have confidence in their ability to maintain the dividend and keep investing in their slow rate of growth.

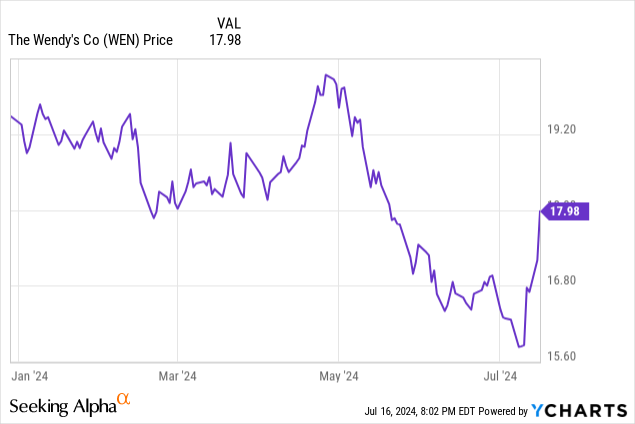

The company has recently bounced off of its 52-week low, but I’m not really sure that the financial justify a recovery, even the modest recovery we’re seeing. I would say Wendy’s is a hold, at best.

If the company was sub $16 per share again, it might be worth reconsidering, though even there with that bringing the dividend yield even higher, I just don’t see that dividend as safe enough for an income play.

Without that income play, I just don’t see where we can justify paying these multiples. If there was a price that was more appealing, I would need to consider where they’re going to find the balance between dividend payout and funding company growth.

Read the full article here