")

")

")

On 01/08/2024, Volkswagen (OTCPK:VWAGY)(OTCPK:VLKAF)(OTCPK:VWAPY) released its Q2 update. Here at the Lab, this year, we have already reported the company’s FY 2023 results and the Chinese Capital Market Day, presenting supportive in-house development and local partnerships investments. Indeed, our buy rating was supported by 1) lower CAPEX thanks to new collaborations (or Rivian case with new equity stake investment), 2) ongoing cost-saving measures, and 3) a solid balance sheet with a negative stub value on a sum-of-the-part basis. For this reason, our team also has coverage of Dr. Ing. h.c. F. Porsche AG (OTCPK:DRPRY)(OTCPK:DRPRF) (or P911) with a buy rating target (2024 A Year Of Groundwork).

Q2 Earnings

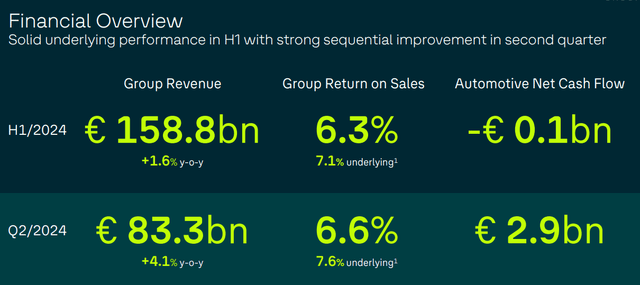

The company reported a small beat at the operating profit margin level. In detail, Volkswagen reached 7.6%, excluding all non-recurring items, which accounted for minus €0.9 billion. Including these one-offs, the operating margin came in at 6.6%, slightly ahead of the consensus expectation set at 6.4% (Fig 1). Going up to the P&L analysis, Volkswagen volumes were down by 3% on a yearly level, which had an impact on all segments. Still, in the Q2 analysis, we see volume up with a price down, mainly due to intensifying competition and Audi product changeovers. The group revenue came in at €83 billion, an increase of 4% every year. During the quarter, fair value impacts outside hedge accounting amounted to €0.4 billion. In addition, we report a positive effect of €720 million in R&D capitalization and higher fixed and other costs, for a total of €-2.2 billion. This was due to wage inflation and D&A, including €1.0 billion of restructuring costs. As reported above, the underlying margin would have reached 7.6% without these impacts. On a positive note, the company’s free cash flow reached €2.9 billion, above the consensus expectation of €2.1 billion. This was driven by good sales performance.

Volkswagen H1 results

Source: Volkswagen Q2 results – Fig 1

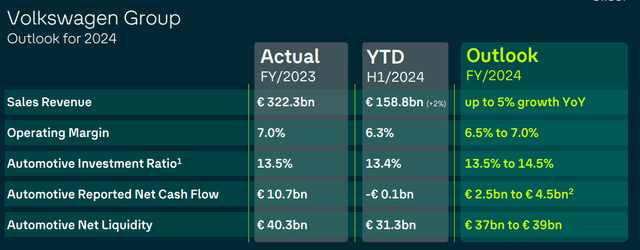

In July, the company cut its 2024 Fiscal Year outlook for operating margin and net cash flow. This was due to further restructuring measures with an industrial plant closure in Brussels. Volkswagen reported a preference to deliberately prioritize sustainable value creation over higher volumes. After the Q2 results, the leadership team guided towards the lower end of the KPI ranges. In our upside view, we note that Wall Street consensus is already at the lower end of the KPI (revenue and operating margin). Therefore, we are not anticipating stock price volatility or downgrades based on the implied consensus estimates.

Volkswagen Outlook

Fig 2

Our Upside to Consider

- Volkswagen remains under pressure but is improving sequentially. In our view, the Brussels plant closure suggests a step in the right direction. Further efficiency measures after the performance program are expected to address the company’s European cost problem. That said, without considering the negative one-off, the company’s operating margin stood at 7.6%, below peers (Stellantis reached 7.8% and Renault’s 8.1%), but is progressing well;

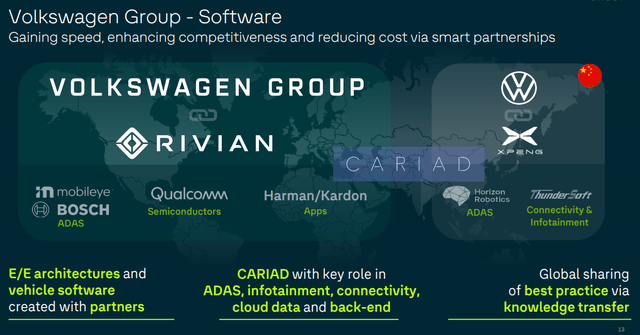

- Here at the Lab, Volkswagen confirmed the peak of investments in the current fiscal year. Therefore, we anticipate lower CAPEX in the following years. Including the latest partnerships, investment needs for the planning round from 2025 to 2029 will decrease by approximately €5 billion to €165 billion. This is based on Rivian investment, QuantumScape, and XPeng collaboration. This is very much aligned with our investment thesis, and as a result of lower EV adoption and new partnerships, the company might benefit from lower CAPEX. Related to Rivian (Fig 3), Volkswagen aims to solve the electric car software problem once and for all. This is happening after years of delays at its in-house unit, Cariad, which have caused significant delays in the launch of the new model. The deal will see the two companies forming a 50-50 joint venture that will allow them to share technology to create a next-generation electric architecture and best-in-class software technology, with vehicles expected to launch in the second half of the decade;

- Q2 CAPEX came in at €3.2 billion. For H2, FCF should improve this to a working capital build-up of €1.3 billion, boosted by inventory increases due to upcoming model launches. In addition, the Chinese entities’ dividends are to be received.

- We suggest our readers check Lamborghini’s H1 results for downside protection. Here at the Lab, we have good coverage of Ferrari. Lamborghini, which sells several cars near Ferrari, has reported positive financial results. Volkswagen fully controls the Italian company. In H1, the company recorded record deliveries (5,558), turnover (+14% to €1.6 billion), and operating profit at the highest level of €458 million (Fig 4). This success is supported by three models: Revuelto, Urus, and Huracán. In addition, as reported for Ferrari, the company expected expectations thanks to higher customizations. Lamborghini also distributes orders globally, without depending on China. Lamborghini also has an EBIT margin of 28.2% (similar to Ferrari at 28.9%). On a standalone basis, valuing the company with a 20% discount to Ferrari on EV/EBIT, we reached a valuation of almost €26 billion. This represents half of Volkswagen’s market cap. In addition, Volkswagen also owns supercars such as Porsche, Bugatti, and Bentley.

Rivian partnerships

Fig 3

Lamborghini H1 results

Fig 4

Adjusting Estimates and Valuation

Following the Q1 results, we confirmed our sales of €338 billion and lowered Volkswagen’s core operating profit margin from 7% to 6.5% to €21.97 billion. As we can see from the new company’s estimates (Fig 2), we are still at the low end of the guidance. On a yearly level, this represents an EBIT margin of 7.6%. Including the Q2 negative one-off, we decided to lower our EPS projection. In Q1, we reported a negative one-off cost of €900 million; in Q2, restructuring costs were almost €1 billion. For this reason, we lower our net income to €13.15 billion, with an EPS of €26.22.

Our equity story remains intact, and we believe it is vital to report our last assessment conclusion:

We are confident in better sales and margins in the upcoming quarters and positively view the Volkswagen redundancy provision for Q2 2024. This finally means the company is getting serious about reverting its operating margin decline.

These words were very much aligned with the company’s performance. Regarding the valuation, we value the company with a group P/E using an over-the-cycle multiple set at 6.5x. This reflects the company’s solid balance sheet and ability to ensure a smooth transition into autonomous driving and EVs. For this reason, we lower our valuation from €197 to €170.5 per share, maintaining a buy rating status. As a reference, the company now trades at a current P/E of 3x with an EV/EBITDA < 0.5x. Volkswagen is currently at a bargain with a €30 billion net liquidity.

Risks

Downside risks could arise from 1) COGS price changes, 2) lower-than-anticipated vehicle sales volumes in Volkswagen’s main markets, 3) lower price MIX with a deterioration of the pricing environment, 4) higher-for-longer interest rates (this is related to its Financial Services segment), 5) any rapid levering up of the company’s balance sheet, 5) currency development changes given the fact that the company reported in euro terms but 7.7 million cars are sold outside Europe, 6) higher litigation costs across different regions, 6) competitive pressure from new entrants (Chinese comps), and 7) execution risks on the company’s new partnerships.

Conclusion

We reduce the company’s EPS estimates for prudency reasons, adjusting our model for adverse one-off events. That said, we still believe it is The Most Discounted Auto Stock. There is downside protection in the luxury segment that cannot be unnoticed. Therefore, our buy rating is still confirmed.

Editor’s Note: This article discusses one or more securities that do not trade on a major U.S. exchange. Please be aware of the risks associated with these stocks.

Read the full article here

")

")

")

")