")

")

")

(NYSE:BABA)")

")

The Vita Coco Company, Inc. (NASDAQ:COCO) is going to report the company’s Q2 results on the 31st of July, foreseeing pressured gross margins due to higher freight costs. The overall growth story continued strong despite hiccups in the gross margin and in revenue growth in 2024.

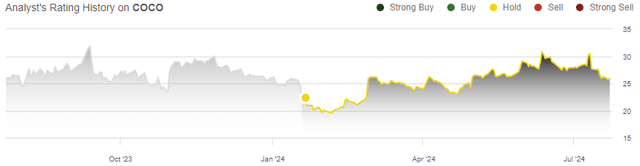

I previously wrote an article on the stock, titled “Vita Coco: Future Growth Potential Is Fairly Valued.” In the article, I went over Vita Coco’s growth ambitions and the valuation that reflected the company’s earnings prospects well, initiating the stock at a Hold rating. Since, the stock has returned 20%, slightly outpacing the S&P 500’s return of 14% in the same period.

My Rating History on COCO (Seeking Alpha)

Upcoming Q2 Report: Expect Freight Turbulence

Vita Coco is going to report the company’s Q2 results on the 31st of July in pre-market hours. Wall Street analysts estimate a revenue growth of 3.2% into $144.1 million along with a normalized EPS of $0.32, a decrease of one cent year-over-year.

Ocean freight rates will be taking a toll on Vita Coco’s profitability in upcoming quarters, especially in Q2, as noted in the Q1 report. The Red Sea Crisis that affects shipping through the Suez Canal is going to have a very negative impact on the gross margin, which Vita Coco communicated to have an especially large effect in Q2.

Considering Vita Coco’s Q1 growth of 1.8%, the company’s 2024 financial guidance including a $500-510 million sales guidance corresponding to a growth of 1.3% to 3.3%, and the foreseen freight issues, I believe that the Wall Street estimates represent a fair baseline expectation. While discretionary product firms have battled with slower demand, beverage companies have still mostly reported stable figures in recent quarters. Vita Coco is even seen by Wells Fargo to have experienced accelerating demand trends during Q2. The launch of Vita Coco Treats drinks in Targets in April should also aid the growth in Q2 to be above the 1.8% growth in Q1.

Higher freight expenses could still cause turbulence in the quarter, but as they are likely only temporary, and are already communicated clearly, I don’t believe that investors should read too much into the weakness. The company didn’t provide a clear gross margin expectation for Q2 in the Q1 earnings call yet, with Vita Coco also having unclear visibility into the freight costs’ trajectory.

The Overall Growth Story Continues

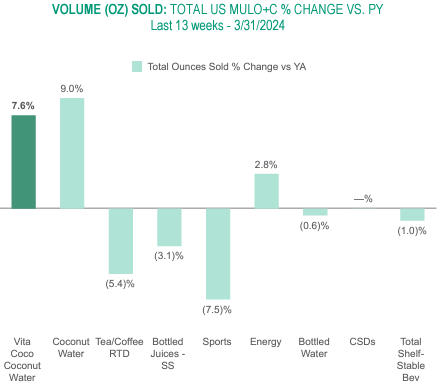

While the Q2 growth and 2024 financial outlook both expect slower-than-usual growth at the mid-point of only 2.3%, the overall growth story remains strong. The ending of a private label contract is causing the hiccup in growth temporarily in 2024, whereas Vita Coco’s sales are still performing strongly. The gross margin has seen impressive expansion into 42.2% in Q1, up a dramatic 11.5 percentage points year-over-year, showing even stronger margin expansion than I could have previously anticipated.

Vita Coco’s Q1 Investor Presentation

According to Nielsen’s quantitative research, Vita Coco has continued performing incredibly well in the beverage industry from mid-June into mid-July as well, adding onto Wells Fargo’s positive remarks of Vita Coco’s demand. The branded sales look to grow with continued momentum, with Vita Coco also communicating faith in good sales momentum in private label sales in the Q1 earnings call.

The company has also identified potential additional product categories in functional hydration, including orange juice, cranberry juice, Greek yogurt, and hummus, adding to Vita Coco’s longer-term growth story beyond the strong branded coconut water growth. The expected Q2 hiccup in profitability, and 2024 hiccup in growth are likely only temporary.

COCO’s Valuation Remains Balanced

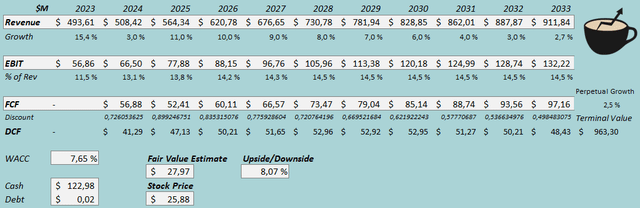

I slightly updated my discounted cash flow [DCF] model from previous estimates, now estimating a 3% growth in 2024 instead of 4% previously within Vita Coco’s guidance range for the year. Afterward, I still estimate similar growth at a total organic revenue CAGR of 6.3% from 2023 to 2033, and 2.5% perpetual growth afterward.

With Vita Coco’s great reported margins, disturbed in the short term by higher freight costs, I now estimate the EBIT margin to expand into 14.5% eventually compared to a 14.0% estimated level previously. I have kept the cash flow conversion at a good level.

DCF Model (Author’s Calculation)

The estimates put Vita Coco’s fair value estimate at $27.97, 8% above the stock price at the time of writing – the growth story remains relatively fairly valued at the current forward EV/EBITDA of 16.7. My DCF model’s fair value estimate is up from $24.11 previously due to slightly higher cash flow estimates.

CAPM

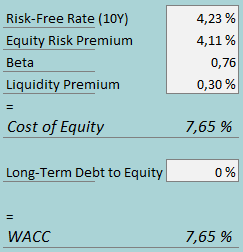

A weighted average cost of capital of 7.65% is used in the DCF model, down slightly from 7.94% previously. The used WACC is derived from a capital asset pricing model:

CAPM (Author’s Calculation)

Vita Coco doesn’t have notable interest-bearing debt, and as such, I again estimate a long-term debt-to-equity ratio of 0%. To estimate the cost of equity, I use the 10-year bond yield of 4.23% as the risk-free rate. The equity risk premium of 4.11% is Professor Aswath Damodaran’s estimate for the US, updated in July. I have kept the beta estimate at 0.76. With a liquidity premium of 0.3%, the cost of equity and WACC both stand at 7.65%.

Takeaway

Vita Coco’s Q2 report is looking to show continued moderate growth, but pressured margins due to higher temporarily turbulent, high freight expenses. The company’s underlying strength is still impressive, with branded sales showing great demand and faith for private label sales being high. The freight issues and a priorly communicated private label deal’s ending creating the hiccups in gross margins and growth temporarily. Ahead of the Q2 report, Vita Coco’s stock is again valued fairly, and as such, I remain with a Hold rating.

Read the full article here

")

")

")

(NYSE:BABA)")