")

")

Vanguard U.S. Value Factor ETF (BATS:VFVA), launched on 02/13/2018 and managed by The Vanguard Group, Inc., is an actively managed value ETF that measures its performance against the Russell 3000 index.

While I trust that the value factor based on relevant indicators can provide long-term outperformance, I am reluctant to believe that this active fund will be able to deliver meaningful excess returns going forward. Both its expense and turnover ratio are very low, and its valuation is very attractive, but its track record is short and there is not a lot of transparency due to its nature as an actively managed fund. But more important is the size agnosticism here; It’s usually both the value and company size factors that deliver significant outperformance in the long term. Here, we only have the former present.

Methodology

The ETF invests in stocks issued in the U.S. with the potential to outperform the broad U.S. market, as represented by the Russell 3000 index. Using a quantitative model, it focuses on stocks that are undervalued in a very large universe that includes large-, mid-, and small-cap U.S. companies.

The measures that managers employ to determine the exposure of the stocks to the value factor are the forward earnings yield, the book value to price ratio, and the operating cash flow yield (excluding financial companies). These are all classic indicators of value, with the last two being more predictive of outperformance in my experience, as the earnings ratio can often mislead due to the more volatile nature of earnings and earnings expectations.

As for the available universe, on the one hand, looking for value within such a large range of company size should theoretically allow investors to find the most undervalued stocks. However, the size factor is as important in yielding excess returns as the value one. Although such a portfolio may, for instance, be able to include a lot of value opportunities in the large-cap segment, the correction of such inefficiencies may not be as rapid as in the small-cap segment.

That may be the reason for the narrower performance differential usually observed when size is adjusted, as in this case (this fund’s available universe is the same as its benchmark’s). So, even if it ends up outperforming in the long run, it’s likely that VFVA will not deliver substantial excess returns. Speaking of which…

Performance & Cost

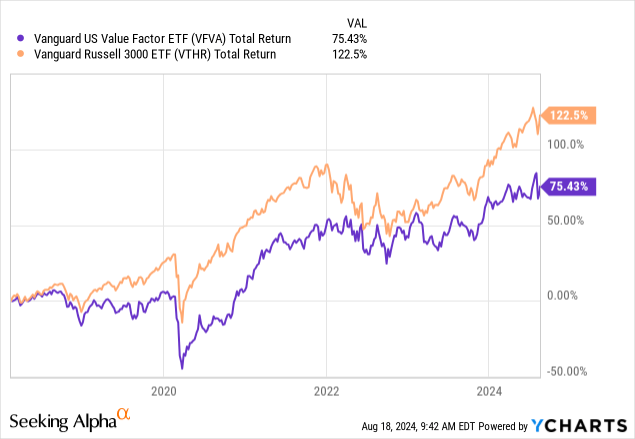

Since its inception, VFVA realized an annualized return of 10.34% based on its market price, while the index reflected one of 13.23%. Underperformance is also illustrated when you compare VFVA to its vanilla counterpart:

However, it’s good to remember that the track record we have available cannot provide us with a clear picture of whether management is effective here because it’s too short for a value fund.

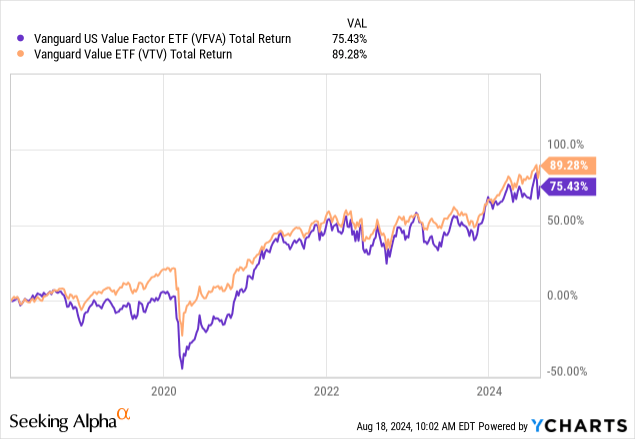

Now, look at how narrow the spread is when you compare VFVA to a large-cap value fund; in this case, the Vanguard Value ETF (VTV):

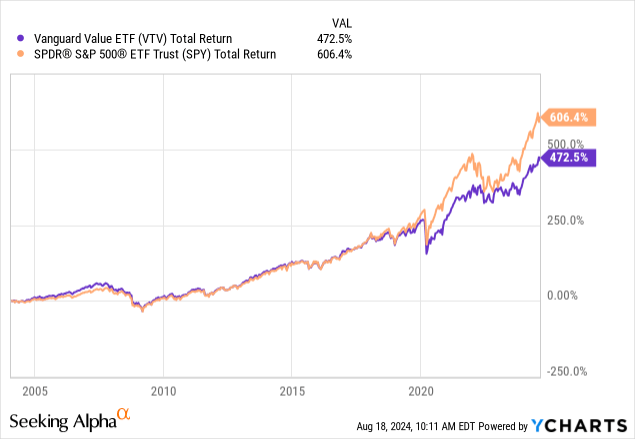

VTV has also been underperforming the broad market in the last 5 years or so:

There is always the possibility that an actively managed ETF may not be well-managed and result in underdelivering. However, I don’t think that this driver is very likely. It’s far more likely that by taking the size factor out of the equation, VFVA’s outperformance (if it ever realizes it) will not be significant, as I mentioned above.

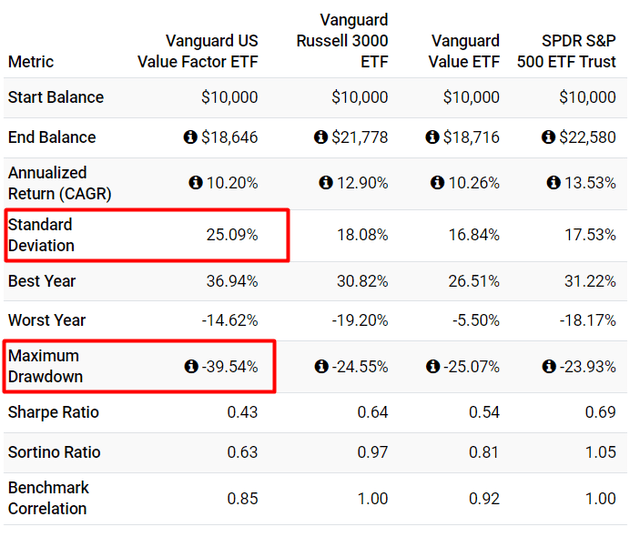

What is also concerning is its volatility relative to the other ETFs. Its maximum drawdown was particularly severe:

Portfolio Visualizer

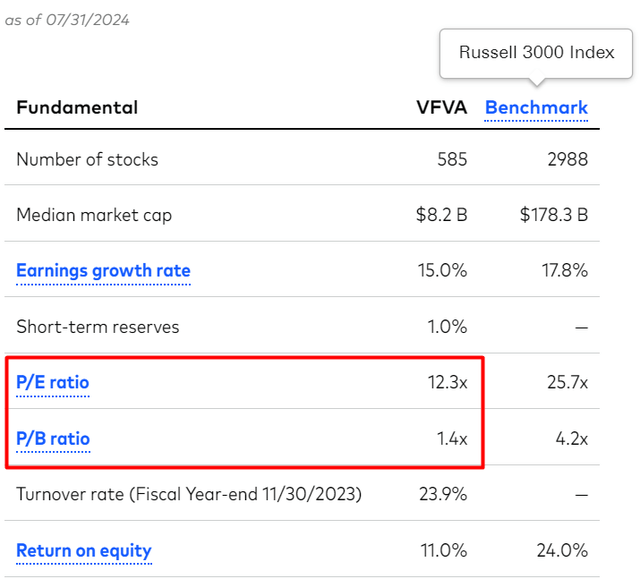

All that being said, the comparisons may not be the best here, as VFVA’s median market cap is $8.2 billion. It’s not exclusively a large-cap fund, so there’s a good chance it surprises us going forward. Valuation surely looks very attractive right now compared to its benchmark’s:

Vanguard

As you can see, turnover is also really low for an actively managed ETF and with an expense ratio of only 0.13%, it could manage to outperform the market in the long run. I just think that there are other, more promising options available for value investors.

Risks

The major risk here is the potential opportunity cost. I don’t think there is enough attractiveness here to select this fund with an adequate degree of confidence that its potential outperformance will end up worth your time in the market.

There’s also the risk that comes with active management. It’s one thing to rely on an index that selects and weights securities based on a ranking system for which you have adequate information to understand exactly what factors you’re exposed to, and a wholly another one to rely on a management team that follows a much less transparent strategy.

A concentration risk is also present as 28.08% of the portfolio is exposed to the Financials sector.

Verdict

In conclusion, I believe that its past performance is not that relevant, but the uncertainty of active management coupled with the short track record and the lack of a size bias make this ETF much less attractive than other options. Therefore, I am rating it a hold for now and I recommend you take a look at a recent article I wrote about Dimensional U.S. Targeted Value ETF (DFAT).

What’s your opinion? Do you own this ETF or prefer something else? Let me know below, and thank you for reading!

Read the full article here

")

")