")

")

")

")

Verizon Communications Inc. (NYSE:VZ) is a stock we traded in 2023, running the stock from buys at 34 and 31 back to $40. While traders took profit at our service, a number of them rolled the profit into a so-called house position to collect long-term future gains, all dividends, spinoffs etc. It is a key approach for wealth creation long term that we like to employ. With the rally, the Q4 earnings were heavily anticipated. And well, Verizon just dropped the hammer with its just reported earnings.

Overall, the Q4 results were mixed, with some high points and some lows. We still believe this is a great stock for long-term income and/or compounding in a tax-favored account as well. We also love a buy-write options strategy here for added income. In this column, we compare results to our expectations.

Verizon Q4 results in context

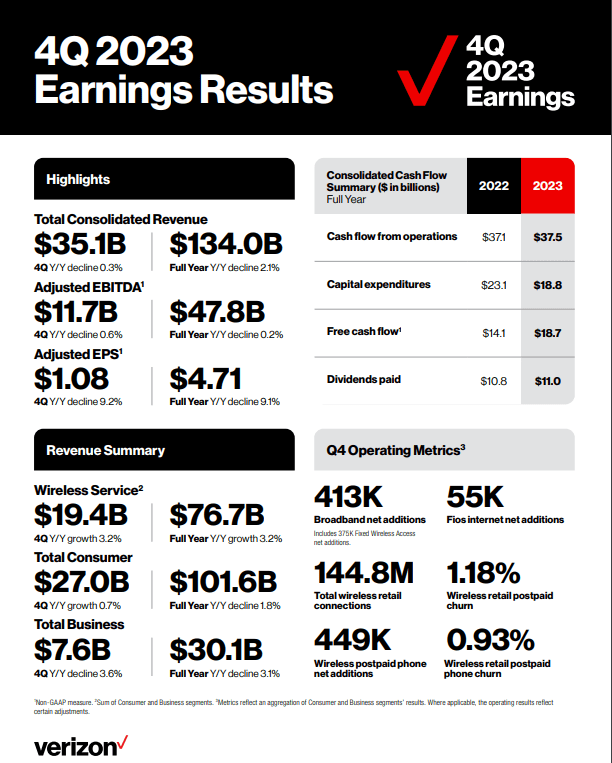

While the critical Q4 earnings season is just getting started, there are growing concerns over what guidance for 2024 will look like and concerns over the health of the consumer stemming from all of the Feds actions. That said, Verizon revenues were well ahead of expectations, and hit the very top end of our expectations. For the most part in the report, our forecasts were pretty close, and while we thought Verizon may have difficulty with margins and earnings from being very promotional to attract customers, they once again reported decent results relative to our expectations. Revenue came in at $35.1 billion and was down just 0.6% from last year. See the infographic below:

Verizon

The comparisons of interest you should be aware of are largely summarized above for Q3. What about the revenue drivers?

Verizon’s Q4 2023 revenue drivers

As we saw, revenues were down 0.6% but well ahead of expectations, setting a strong tone. For Q4, we were looking for $34.5-$35.1 billion for the top line, so these results were at the highest end of our projections. Recall we were much more bullish than consensus. Those expectations were surpassed by $550 million. What about customer additions? We were looking for retail postpaid net additions of 500,000+ and wireless postpaid phone gross additions to increase high single-digits year-over-year. We were also looking for churn below 1.2% for retail postpaid customers. For broadband, we were looking for net additions of 420,000 and were projecting 36,000+ Fios Internet net additions.

Our projections were relatively reliable. In wireless, there were postpaid phone net additions of 449,000 and retail postpaid net adds of 1.4 million, the latter trouncing our expectations and leading to the high end of revenue expectations. Churn came in right around what we were looking for at 1.18% overall, but consumer wireless retail postpaid churn was almost in line with our expectations at 1.08%, and wireless retail postpaid phone churn was 0.88%. Business wireless retail postpaid churn was 1.48%, and wireless retail postpaid phone churn was 1.14 percent.

Over in broadband, there were net additions of 413,000, reflecting a strong demand for fixed wireless and Fios products. There were 375,000 fixed wireless net additions. That marked the fifth consecutive quarter that Verizon reported more than 400,000 broadband net additions. There are now over 3 million subscribers. There were 55,000 Fios Internet net additions, also surpassing expectations. All in all, the company performed well relative to what we laid out that you could expect.

Verizon Q4 earnings outperformance

For Q4, we were expecting ongoing cost controls. Q4 2023 operating expenses were $28.0 billion, and for Q3 2023 we were targeting operating expenses of $28.1-$28.4 billion, and operating income of $7.7-$7.9 billion. These expectations were about spot on, but there was a massive write down of goodwill in the amount of nearly $6 billion. As such, operating expenses were $34.5 billion in total, or $28.5 billion without the impairment/

For adjusted EBITDA, we are targeting $11.7-$12.1 billion. On a per share basis, assuming our projections capture the results with relative precision, we see EPS of $1.07-$1.14 for Q4. Analysts were looking for $1.08, the low end of our target, and the company hit $1.08 in EPS. Adjusted EBITDA was $11.7 billion, also at the low end of our expectations.

Free cash flow

Assuming cash from operating activities of $10.1-$10.6 billion, capex and other expenditures of $4.8-5.2 billion, we were targeting free cash flow of $5.3-$5.8 billion. Well, cash flow from operations was $8.7 billion. Capex was $4.6 billion. Keep in mind that Verizon pays more each year to the dividend. Dividends paid were about $2.75 billion in Q4. Free cash flow was $4.1 billion. As such, the free cash flow payout ratio was 67% here. For the year, we were anticipating a payout ratio of less than 75%.

Folks, free cash flow this year was $18.7 billion, so the payout ratio was just under 60%. Solid

The debt

So, if there is one thing we hear over and over about, it is the debt. We have said before and will reiterate, the debt will never, ever be paid off. But leverage will be reduced, so that it is not eating up so much of the cash coming in to pay interest and principal. Yes, the debt burden is large. Interest expense will continue to climb on new debt at higher rates in this climate. So, the company is trying to chip away at the debt. Coming into Q4, the net debt was still massive at $122.2 billion, with a debt to adjusted EBITDA ratio of 2.6X. However, it ticked up in the quarter to $126.4 billion.

Final thoughts

Our projections were relatively close here, and we like the Verizon Communications Inc. Q4 results. The impairment charge is a one-off in our opinion. For income seekers, the dividend is well covered. Debt needs to be watched. What about the all-important guidance? Guidance was mixed in our opinion. It is looking for revenue growth of 2-3.5% in total wireless service revenue, adjusted EBITDA growth of 1-3%, and adjusted EPS of $4.50-$4.70, which was below consensus at the midpoint. Cash flow should be around $19 billion since capital expenditures were guided to be about $1.0 to $1.5 billion lower from 2023, though the expectations on revenue are murky, and likely to be flat to within 3% declines or growth depending on performance.

Verizon stock is not as attractive as it was when we were big buyers, but the yield is still attractive. The company is on the come up.

Have some thoughts to share?

Do you have thoughts here? Are you a perennial bears that see the company going broke? Do you think the company can reduce leverage? Are you long and collecting the dividend? Are you trading options on the stock, or embracing an approach to trade around the core position to magnify gains? Got a better dividend name in the space? Have something else to add? Let the community know below.

Read the full article here

")

")

")

")

")

")