")

Q2 2024 Earnings Call Transcript")

(NYSE:UTZ)")

My investment rating for Utz Brands, Inc. (NYSE:UTZ) stock is downgraded from a Buy to a Hold. Utz Brands’ near-term growth outlook has become less favorable with the company lowering its full-year organic sales growth guidance, and this justifies a rating downgrade. But there is upside potential associated with the stock, assuming that UTZ boosts its inorganic growth prospects with M&A deals or that the company becomes an acquisition target for bigger snack companies. As such, I have rated UTZ as a Hold, rather than a Sell.

This update is focused on Utz Brands’ updated fiscal 2024 organic sales growth guidance and the company’s disclosures at a recent investor conference. My prior July 3, 2023 write-up drew attention to UTZ’s capital allocation moves.

Utz Brands’ Downward Revision In Organic Sales Growth Guidance Was Disappointing

UTZ published a press release on Thursday, September 5 disclosing that it has lowered its FY 2024 organic sales growth guidance from +3% previously to +2.0%-2.5% now. In the company’s press release, Utz Brands cited “a more competitive promotional environment” for 2H 2024 as the key factor contributing to the change in its sales outlook.

I am disappointed with Utz Brands’ updated organic sales guidance for three reasons.

Firstly, the company’s diverse range of brands wasn’t able to offset the negative effects of price competition.

A Snapshot Of UTZ’s Various Brands

Utz Brands’ Investor Relations Website

At its earlier Q2 2024 analyst briefing on August 1, Utz Brands had stressed that it has a “broad portfolio of brands” which includes those targeting “a more value-conscious consumer who’s looking for an absolute price point.”

But UTZ acknowledged at the most recent Barclays (BCS) Global Consumer Staples Conference on September 5 that the gap between “the entry point in the marketplace” and the “premium point in the price ladder” is now “more compressed than we would normally expect it to be.” This means the lines between premium and value brands in the salty snacks market have blurred in this promotional market environment focused on pricing.

In other words, UTZ’s portfolio of brands positioned at different pricing levels offers limited support for its top line, when the players in the salty snacks market become more promotional and compete more aggressively on price.

Secondly, UTZ’s revised sales growth outlook for the current year implies that it has become more challenging for the company to meet its mid-term top line expansion targets.

UTZ had previously set a target of achieving a +4%-5% organic sales CAGR for the FY 2023-2026 time frame at the company’s Investor Day in mid-December last year. As indicated in its 2023 Investor Day presentation slides, the FY 2023-2026 organic sales CAGR goal of a +4%-5% assumes a +2%-3% volume CAGR and +2% price CAGR in the same time period.

At the latest Barclays investor event, the company highlighted that its “last major price advance was really in 2023” and emphasized that it has observed “a much more promotional environment than” expected with respect to “the depth of the pricing that they (competitors) went into.”

In a nutshell, Utz Brands’ updated FY 2024 organic sales CAGR outlook in the +2.0%-2.5% range is significantly below its medium-term organic sales CAGR target of between +4% and +5%. In particular, it might be difficult for UTZ to raise prices going forward to meet its intermediate term top line expansion goal if price competition in the salty snacks market remains intense for a sustained period of time.

Thirdly, there could be downside risks associated with Utz Brands’ full-year FY 2024 operating profitability.

In its September 5, 2024 press release, UTZ reiterated the company’s existing +5%-8% normalized EBITDA growth guidance for FY 2024. This is aligned with the company’s goal of improving its normalized EBITDA margin by +1 percentage points every year between FY 2023 and FY 2026 as outlined at its 2023 Investor Day.

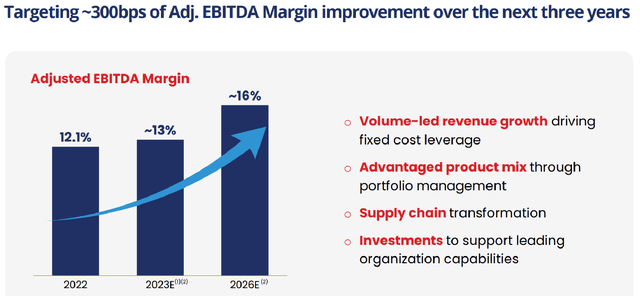

An Overview Of UTZ’s Efforts To Expand Normalized EBITDA Margin

Utz Brands’ 2023 Investor Day Presentation Slides

As per the chart presented above, “volume-led revenue growth driving fixed cost leverage” is one of the key driver of UTZ’s operating profitability improvement in the coming years. Notably, Utz Brands indicated at the early-September Barclays investor conference that “we do anticipate that the environment will be more promotional as we go forward.”

Assuming that Utz Brands’ volume expansion and organic sales continue to weaken, the company’s actual FY 2024 EBITDA margin and EBITDA growth might fall below expectations due to negative operating leverage effects.

In summary, I am no longer bullish on UTZ after assessing the unfavorable read-throughs from the company’s revised organic sales growth outlook for the current year.

The Potential To Acquire Or Be Acquired Is A Positive Factor For UTZ

I have stopped short of awarding a Sell rating to Utz Brands despite its weaker-than-expected organic sales growth outlook outlined in the preceding section. This is because there are potential value creation opportunities for UTZ relating to M&A.

On one hand, UTZ could boost its inorganic growth prospects with acquisitions to increase its geographical presence in specific high-growth markets.

In my July 3, 2023 update, I mentioned that “the company can achieve an even faster pace of growth by pursuing an inorganic growth path” and “build its presence in Expansion Geographies”, or markets with good growth potential identified by UTZ.

Utz Brands’ recent actions and comments suggest that it is on the lookout for potential M&A opportunities to grow in specific geographical markets.

Last month, UTZ announced that it bought over “certain distribution rights in South Florida from an existing third-party direct-store delivery distributor.” Separately, Utz Brands indicated at the September 5 Barclays conference that the company is in “a natural place to continue to be able to acquire and grow inorganically” and highlighted that “the opportunities are certainly going to be there in the next couple of periods.”

On the other hand, the company might be an acquisition target for larger players seeking to consolidate the snacks market.

At the Barclays Global Consumer Staples Conference on September 5, UTZ noted that there is “a longer tail of competitors” in “our category specifically.”

An earlier August 18, 2024 Seeking Alpha News article cited Piper Sandler’s research speculating that “Hershey (HSY) may be motivated to add more salty snacks to better compete with a combined Kellanova/Mars” with Utz Brands as a “logical candidate.”

In other words, the snacks market is fragmented and there are good reasons for the relatively bigger companies in the space to acquire their smaller peers.

To sum things up, M&A might throw up positive surprises for UTZ. Value-accretive acquisition deals could boost Utz Brands’ growth outlook, while the company’s shares have the potential to trade higher if UTZ becomes the subject of a takeover offer.

Conclusion

I still have a Neutral view of Utz Brands, taking into consideration negatives associated with the company’s organic sales growth guidance revision and positives relating to potential M&A transactions. In terms of valuations, the stock is reasonably valued at a PEG (Price-to-Earnings Growth) of 1.04 times. The PEG metric for UTZ is derived based on the stock’s consensus next twelve months’ normalized P/E multiple of 22.6 times and the company’s consensus FY 2023-2025 normalized EPS CAGR estimate of +21.7% according to S&P Capital IQ data.

Read the full article here

")

Q2 2024 Earnings Call Transcript")

")

")

")