")

")

On July 9th, uniQure N.V. (NASDAQ:QURE) announced 24-month trial data for its Phase 1/2 clinical trials for AMT-130, an investigational gene therapy for Huntington’s Disease. Despite only enrolling 29 patients in the trial and having data for only 9 at the high dosage, the reduction of disease progression of 80% was so great that it was still statistically significant. The market obviously liked this news, as the two trading days following its release saw QURE move from $3.78 to $10.12. I believe that the stock’s recent pullback into the mid-$7.00s represents an outstanding buying opportunity.

The company has made some aggressive restructuring decisions in order to further extend its rather long cash runway. Junior biotechs usually seek to extend their cash runway through financings or through partnerships with mature pharmaceutical companies. Then seek to expand their pipeline, as they know that any single pipeline product has a low chance of success. The fact that QURE is streamlining its pipeline and operations in the name of preserving cash and focusing on AMT-130 forecasts its confidence that it will be able to bring a product to market. Many small-cap biotechs talk a big game with not much to show for it. QURE has so far shown to be walking the talk.

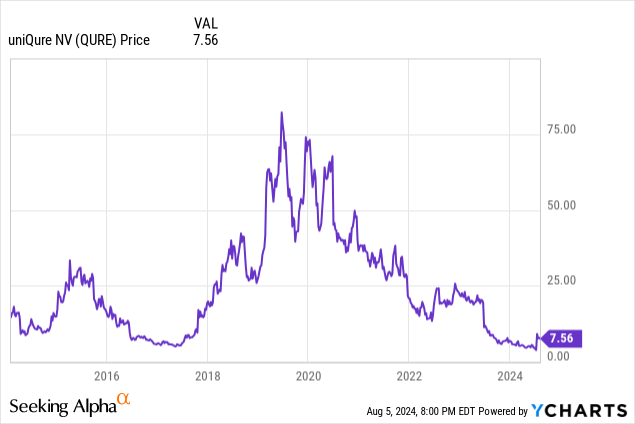

QURE has a five-year chart that is rather disappointing for those who bought between 2019-2021. However, there seems to be a disconnect in sentiment. AMT-130 appears to be back on track to being a potential treatment for Huntington’s Disease after some initially confusing data that was not well received by the market back in June 2023. Yet, it is still trading at a fraction of that price. Buyers today are buying in at a similar price as back in 2017 with hopes of seeing a similar kind of return over the next two years.

Q2 results show a company dedicated to maximizing shareholder value and pushing forward with AMT-130’s early-stage success

Fellow Seeking Alpha analyst Terry Chrisomalis wrote an excellent piece on QURE, getting into some details about the science, near term catalyst and risks. However, that article was written a month ago, prior to the Q2 earnings release. So there is already some information in it that is out of date.

As of March 31, 2024, QURE had $556 million in cash and equivalents. Fast forward three months and that cash balance is down to $524 million. Despite that, the company has managed to increase its projected cash runway from mid-2027 to the end of 2027. This is due to organizational restructuring and the sale of its Lexington manufacturing facility. Headcount has been reduced by 65% while recurring cash burn has been reduced by an estimated $75 million, or 40%, from ~$200 per year to ~$120 million per year.

The stock initially acted very positively to this news, rising 10% in early trading on August 1st before sinking to red. This may have been aided by the general market sell off. However, QURE looks to be at a near-term bottom, as the broad market sell off on August 5th initially saw the stock tank. It climbed to finish up 4% by the end of the day, and its highest close since the earnings announcement.

Such an aggressive reduction in headcount is an unusual move for a junior biotech, which may account for the confused market reaction beyond the broad market sell off. Usually, a junior biotech company undertakes an aggressive cost-cutting program because it’s low on cash or has a major setback during the clinical trial or regulatory process for one of its lead drug candidates. To me, QURE’s cost-cutting is an extraordinarily bullish sign. QURE will be meeting with the FDA by the end of 2024 to discuss an accelerated pathway to approval for AMT-130 for Huntington’s Disease. The fact that it’s getting laser focused on this venture along with its Phase 1/2 trials for refractory mesial temporal lobe epilepsy, Fabry disease and SOD1 amyotrophic lateral sclerosis (ALS) is a signal to me that it has high confidence that AMT-130 will have a successful outcome.

Valuation and risks

When it comes to an early stage, mostly pre-revenue biotech stock, it’s hard to come up with a proper valuation. That is shown with analyst targets that are often many multiples of the current stock price, and seldom right. QURE is no different, as it has an average of a $21.57 price target over 10 analysts, with a high target of $36 and a low target of $6. Seeking Alpha gives a valuation grade of C, but most valuation ratios do not provide meaningful results given QURE’s limited history of revenue and profits.

However, it is easier than average to come up with a justifiable floor target for QURE, due to its strong balance sheet relative to its valuation. Its $511 million in working capital compared to its $369 million market cap means that its enterprise value is deeply negative. Even when accounting for the $102 million in long-term debt, investors are getting a slight discount of $40 million on cash less debt. A trait usually reserved for a biotech fresh off a failed Phase 3 trial.

QURE carries $416 million worth of a liability from a royalty financing agreement relating to a deal signed back in 2021 for HEMGENIX. As this liability is related only to the royalty on sales of HEMGENIX, it doesn’t threaten the solvency of the company nor the of future sales of AMT-130 or other candidates in the pipeline. But it does make a big dent into the company’s net equity. This may be why QURE traded well below its cash balance, and still does despite the recent good news. Investors think the company is more overleveraged than it really is when looking at its balance sheet. Investors should always consult SEC filings to understand each line item on the financial statements, rather than relying solely on third-party data providers.

Risks are significantly mitigated due to the strong balance sheet and long cash runway. But they still exist. The most obvious risk being data on AMT-130 that results in a similar reaction as in June 2023. With such a small cohort of 9 patients receiving the high dosage, a significant regression in just one patient can wreak havoc on the data. The meeting with the FDA will happen before the 36-month trial update coming in mid-2025. But that is only a profit-taking opportunity if there is a positive development relating to accelerated approval.

QURE has reduced its workforce to extend its cash runway and focus on its pipeline. This is good news for the balance sheet and shows confidence from management that AMT-130 will be a success. However, it can be a double-edged sword if things don’t go as planned. The three other previously mentioned trials are there as contingency plans should AMT-130 ultimately not succeed. How much value the market assigns to them should AMT-130 fail is anyone’s guess, but is unlikely to be too high immediately after any setback.

Given the risks that are mitigated by the strong balance sheet, management’s confidence and upcoming catalysts, I believe that QURE will once again be trading north of $10 and ideally closer to $15 by the end of the year. A $10 stock price is still below the company’s working capital and should be considered a realistic floor. $15 leads to a $730 million market cap. That seems achievable for a company with an inside track to treating Huntington’s Disease, a projected $1.2 billion market within the next eight years. Capturing just 10% of the market, or conversely, assuming a 10% chance that it is a success at slowing the progression of Huntington’s Disease through an FDA-approved treatment and will take the bulk of the market, would lead to a risk-adjusted total of $120 million in revenue or a reasonable 6x revenue multiple. I believe that investors will see that risk-to-reward trade-off and bid up the stock price on speculative hype leading into the FDA meeting.

Read the full article here

")

")

")

")