(NASDAQ:NFLX)")

")

")

")

Introduction

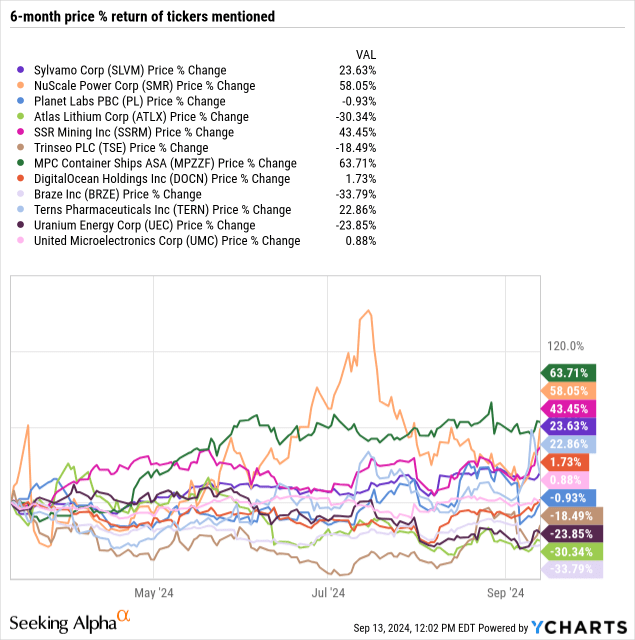

The ‘Undercovered’ Dozen is a Seeking Alpha editor-curated series highlighting 12 articles on undercovered stocks from the last week. We hope this provides ideas and provokes discussion among the community.

Today, we’re looking at articles published between September 6th – 12th.

Take a look at what these less-covered stocks might hold for you. And please join the conversation below to share what you think: are any of these worth following up on?

Zach Bristow | Buy

The overarching thesis on Sylvamo Corporation (SLVM) includes the following:

- Reasonable valuations where the risk/reward opportunity is asymmetrically skewed to the upside. At ~10x earnings / 1.9x EV/IC, market multiples 1) have a high propensity for expansion but 2) have less scope for contraction beyond current levels.

- Management’s attitude towards allocating capital, with ~$200mm set for allocation towards “high return projects” at the end of Q1 FY’24. It is rolling off capital as well and has shed gross debt by >40% since the spin-off.

- The business repurchases high amounts of stock, therefore increasing our stake in a high-quality enterprise without any additional outlay of capital to do so.

- Valuations supportive up to $95 per share in base case assumptions, stretching above $200/share in the upside scenario with (i) less embedded risk [i.e. discount rate] and (ii) more aggressive growth targets.

George Theodosi | Sell

NuScale Power Corporation (SMR) is an overhyped but well-timed 2022 SPAC which raised $380m from a $1.9bn valuation at the time. On a fully dilutive basis, the company trades around $1.85bn (Market cap) currently with shares priced around $7.59. The company designs “NuScale Power Modules” which are uranium fed light water reactors for nuclear power plants.

These are SMRs (Small Modular Reactors) which have been newly implemented by some global superpowers as part of their clean energy mix. The US has over 50 nuclear power plants with over 90 nuclear reactors but no SMRs. NuScale is one of the few US OEMs at the forefront of winning a US SMR project. Energy consumption from electrical grids is expected to climb gradually into the 2030s, partly due to increased electricity data centre demand, which Goldman Sachs forecasts will grow 160% into 2030.

The US doesn’t have any SMRs in construction, or in fact any new nuclear reactors being built (most recent was unit 4 at Vogtle). China, Russia, India, Turkey, South Korea plus many more all have multiple new nuclear power plants being built. However, there are only 4 SMRs in advanced stages of construction globally and 3 operational SMRs globally.

Jason Ditz | Buy

I’ve been looking a lot at companies who make their revenues (or at least plan to) through operations in space. I’m not sure why so many of those have been coming up on my radar lately, but the Q2 earnings release of Planet Labs PBC (PL) has me looking at them closely, especially after they dropped in price significantly on revised Q3 guidance.

Planet Labs is a company that makes its money by collecting a large data set of high and medium-quality satellite images, covering every point of the surface of the Earth. They supply this data on a non-exclusive basis to commercial and government customers for a fee.

The company supplies customers in the agriculture business, along with energy, forestry, finance, and insurance, along with government at the federal, state, and local level, along with international groups.

Planet Labs also uses artificial intelligence and cloud computing to conduct increasing analysis on daily Earth changes in its satellite imagery, which they are hoping will expand the company’s reach into new customers and new applications for their services.

Andrew Hecht | Buy

Lithium is the alkali metal with the lowest density, the most significant electrochemical potential, and the highest energy-to-weight ratio. Lithium’s low atomic weight and the small size of its ions speed its diffusion, making it an ideal battery material. Lithium-ion batteries are critical for electric vehicles and green energy technologies.

Lithium prices have plunged nearly 90% from their 2022 highs, presenting a potential value-based investment opportunity as commodity cycles suggest a price bottom.

Atlas Lithium Corporation (ATLX) is a Brazilian mineral exploration and development company. Atlas Lithium Corporation is transitioning from exploration to production, with significant projects in Brazil and a strategic investment from Mitsui. Mitsui’s $30 million investment in Atlas Lithium, despite current low lithium prices, underscores confidence in the company’s long-term potential and the cyclical nature of commodities.

Bujon Capital | Hold

In February 2024, SSR Mining Inc. (SSRM) suspended all operations at Çöpler following a significant slip on the oxide leach pad, which accounted for roughly 11.0% of Çöpler’s total production in 2023. The share price fell by 53.5% on the announcement date and has been languishing since. The company’s enterprise value is now around $900 million or roughly equal to $122.6 per proven and probable gold ounce and that excludes the silver reserves located at Puna and other resources like those at Hod Maden for example. At the current valuation, I see Çöpler as a cheap call option and any positive news about processing the 706,000 ounces of gold contained in the sulphide stockpiles could act as an important catalyst.

As discussed in my latest article ”Eldorado Gold: All Eyes On Skouries”, Eldorado Gold (EGO) has proven and probable reserves of 11.7 million ounces of gold at an average grade of 1.04 g/t. Based on its current enterprise value of $3.4 billion, we are talking about a valuation of $300 per proven and probable ounce in the ground, which is almost 150% higher than SSR’s valuation. Just prior to the Çöpler incident, both companies were trading roughly in line and if we go back to 2023, SSR was actually trading at a pretty large premium versus Eldorado.

Stefan Lingmerth | Strong Buy

Trinseo PLC (TSE) is a global plastic products’ manufacturer spun out of Dow Chemical Company 15 years ago. The company’s focus has gone from commodity feedstock to value added engineered materials and latex binders to various end users, like housing, automotive, medical, and consumer electronics companies. The current business environment has caused the company to lose sales and experience compressed margins. However, the company has recently seen an improvement and the business cycle looks to be on the up.

The company is dealing with high debt, a legacy from the Bain Capital, LBO, and the Arkema and Aristech acquisitions. The focus now is on selling its JV, using proceeds to reduce the term loan, as well as retiring the bond, maturing in Sep 2025. This is achievable by improving profitability and cash flow, and with very low market capitalization one could see impressive share price improvement going forward. The fed cutting rates will help both the company’s business and lower the interest rate on the debt, which would result in improved cash flow. The market capitalization is only $115 million, yet I believe it could increase to $500 – $1000 million or $14-$28/share with improving cash flow and these catalysts.

Soroya Investments | Buy

MPC Container Ships ASA (OTCPK:MPZZF) recently reported another strong quarter. Its Q2 earnings were $84 million on revenues of $131 million. It declared a $0.10 dividend, the 11th in a row, bringing its yield to about 28%. 76 percent of 2025 and 42 percent of 2026 are already fixed at reasonably good rates.

Since I took up coverage of MPZZF in Q4 2023, the company has continued executing its fleet optimization strategy. This has resulted in a relatively new fleet on water and low operating leverage for the segment. MPZZF is currently in a net cash position, having $160 million in cash and $132 million in long-term debt as of Q2.

Compared to Q2 last year, revenues and earnings were down 32 and 40 percent, respectively. This drop is expected, given the company’s emphasis on earnings visibility through longer-duration time charters.

Combined with the underinvestment in the feeder segment in which MPZZF operates, this company is a vehicle for exposure to a sometimes forgotten part of the global logistics supply chain: the feeders. Its shareholder-friendly communication and capital returns policy makes it well-suited for dividend investors. This segment will reach the end of the cycle later, and I am rating it a buy.

The Other Five Fit For Mention

DigitalOcean Stock: Let Us Wait For A Powerful Catalyst To Break Resistance

KM Capital | Strong Buy

DigitalOcean Holdings Inc.’s (DOCN) financial performance is consistently improving, making it a strong long-term play for growth investors despite current stock price resistance at $40. The company’s scalable business model and increasing ARPU and NDR indicate robust growth potential and effective customer retention strategies. DOCN’s valuation is attractive, with a target price of $61 per share, reflecting a 68% upside based on DCF modeling and industry growth projections.

Braze Stock: Good Q2 Results, But Weaker Long-Term Thesis

Oliver Rodzianko | Hold

Braze, Inc. (BRZE) has shown strong growth thus far, but it is now showing significant trends in contractions in customer adoption and revenue growth rates. This indicates a weaker long-term thesis. While the company achieved good Q2 results, full of estimate beats, its Q2 presentation has particularly revealing charts showing underlying expansion concerns. As a result of macro and AI-company startup competition pressures, its high price-to-sales ratio of 8.66 looks set to contract over the coming years. Near-term alpha likely, long-term alpha unlikely.

Terns Pharmaceuticals: Weight Loss Drug TERN-601 Is Competitive

Biotech Beast | Buy

Terns Pharmaceuticals, Inc.’s (TERN) TERN-601 shows impressive weight loss results in a phase 1 study, positioning TERN competitively in the obesity drug market. The commercial viability of TERN-601’s manufacturing scalability could be an advantage over certain competitors like Novo Nordisk’s Rybelsus. TERN has sufficient funds to support operations into 2026, and a recent $125M public offering could allow it to go further.

Uranium Energy Corp. Has The Assets, Now Has To Produce

Michael Del Monte | Sell

Uranium Energy Corp. (UEC) brought back their Wyoming mining operations in August 2024 and has a remaining purchasing agreement for 1mm pounds of uranium priced at $39/lb. The company remains in the exploration stage with no proven reserves, generating minimal revenue and relying heavily on uranium stockpiling and toll processing services. Despite long-term potential due to rising nuclear power demand, Uranium Energy Corp. continues to finance operations through large equity raises, creating a challenging environment for investors.

United Microelectronics: Performance Gets Better With Every Quarter

Gytis Zizys | Strong Buy

United Microelectronics Corporation’s (UMC) Q2 results show improved financials with a $1.75B revenue, a $0.17 GAAP EPS, and increased gross and operating margins, signaling a positive shift. The company’s strong financial position, with $4B in cash and low debt, ensures stability and growth potential, even during market downturns. Despite market volatility, United Microelectronics remains a strong buy at its current discounted price, with long-term growth expected as demand recovers in key sectors.

Editor’s Note: This article discusses one or more securities that do not trade on a major U.S. exchange. Please be aware of the risks associated with these stocks.

Read the full article here

(NASDAQ:NFLX)")

")

")

")