(NASDAQ:META)")

")

")

We have found in a long life that one competitor is frequently enough to ruin a business. – Charlie Munger

We are surprised to see Uber (NYSE:UBER) investors cheer autonomous driving advancements, with shares rising after the company announced an expansion of a robo-taxi partnership with Alphabet’s (GOOG) Waymo. While this makes Uber look relevant in the autonomous driving race, the reality is that it is much more of a threat than an opportunity for the company. It is likely to work as well for Uber as allowing customers to make Amazon (AMZN) returns at their stores did for Kohl’s (KSS). At first, it might appear that autonomous driving would reduce the biggest cost for Uber, and that this might allow the company to increase profits while lowering the cost of rides.

The same logic could have been applied to Office Depot (ODP) and declining prices of printers and copiers. At first it probably did help the company spend less money on its equipment, however it eventually led to people just buying their own home or office printer. Perhaps an even better example can be found with the Internet and newspapers, which reminds us that technological disruption can weaken or even destroy competitive moats. While the Internet lowered distribution costs for newspapers, it also lowered the cost to compete, opening the gates for anyone with a laptop to enter the publishing business. We know how well that has worked for the legacy publishing industry.

Uber’s management is happy selling a vision where the company remains at the center of the mobility revolution, and where different autonomous vehicle (AV) partners are simply integrated into the ecosystems. In addition to Waymo, they have discussed working with General Motors’ (GM) Cruise and UK startup Wayve, among others. The problem for Uber is that these companies will own the patents, know-how, and trade secrets that will be significantly more difficult to replicate than an app and a nice logo.

We cannot imagine these companies agreeing to share 30% to 50% of the generated revenue with Uber or Lyft (LYFT). They would have such strong bargaining power that ride-share companies would have to either lower their commissions by an order of magnitude, or the AV companies could simply buy cars, launch an app, and undercut the legacy ride-share companies by offering prices at a fraction of what they currently cost per mile. AV companies could even just sell the technology as a recurring subscription, in a similar way to what Tesla (TSLA) is doing with its FSD offering, and let local entrepreneurs buy a few autonomous cars and compete with Uber or Lyft in their city or town.

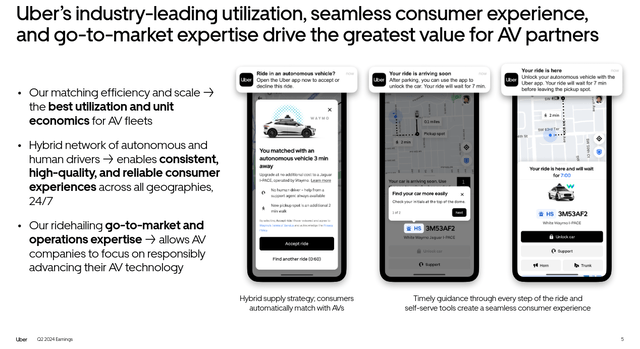

Uber Investor Presentation

2-Sided Marketplaces

Platforms like Uber derive most of their competitive advantage from network effects in 2-sided marketplaces. It is very difficult to sell rides if you don’t have drivers on your platform, and it is equally challenging to convince drivers to join if you don’t have enough rides for them to complete. Airbnb (ABNB) benefits from a similar dynamic, but we would argue that its competitive moat is stronger because it has a more global scale, whereas ride-sharing tends to require a certain critical mass at the city or state level. For example, Lyft has managed to reach enough critical mass in NY City to compete with Uber, and Bolt in London and other European cities.

The problem for Uber, and ride-sharing companies in general, is that once you remove the drivers from the equation, they no longer have 2-sided marketplaces. Suddenly, GM or Tesla can launch overnight an app in a given city, with just a few hundred robo-taxis. They could even offer rides for free the first month, and with a little bit of publicity and marketing they would take over the market faster than you can say, “Alexa, book me a ride… wait, what do you mean it’s free?”.

Autonomous Driving and Autonomous Delivery

Uber’s CEO Dara Khosrowshahi went into significant detail about Uber’s prospects in an autonomous driving world at a recent Goldman Sachs Group (GS) investor conference. It is long, but well worth reading as it presents the case for why Uber is well-placed to benefit from the new technology. Interestingly, he does not come across as very confident about the potential impact, describing it as dynamic and saying that they can only respond to developments as they gain visibility. There are some things with which we agree, like the historical precedent that lower prices will expand the market. Still, as memory chipmakers learned, lower prices significantly increased demand, but they still made less money. Similarly, Uber could see the number of rides increase, but with a lower price per ride and a lower take rate, their revenues could actually decline. One of his main arguments is that Uber, with its large number of users, could help autonomous players maintain close to 100% utilization rates. Still, they could prefer a lower utilization rate than pay the extremely high take rate Uber currently charges. With the 2-sided marketplace broken, the autonomous players could threaten a direct-to-consumer approach.

Yeah. Listen, it’s dynamic, and we can only do as best as what we see. Generally, we want to build a marketplace, and we want to stay as pure-play marketplace as we can. So if you look back three, four years ago, a bunch of our competitors in delivery, were getting into the dark kitchen business. They were building dark grocery. I was like this is the next big thing, and they went in and invested in those heavy assets, so to speak, to some extent, going in competition with some of their own suppliers, we didn’t, right? So philosophically, generally, we want to play where we’re strong, which is we bring demand and we’re able to target that demand against supply in a way that improves earnings for suppliers, improves utilization for suppliers. And it’s the reason why in mobility, we have the biggest supply in the world in delivery. Certainly, on a global basis, we have one of the largest supply bases out there. When you look at autonomous, the first thing I would say, is we think that autonomous, actually, is going to increase the pie for everybody, right? We are a supply-led business, the more supply we add into the marketplace, supply improves the quality of the marketplace in terms of ETAs, in terms of the choice that consumers have and we think autonomous can be very, very high-quality supply that comes on to the marketplace over a period of time because it’s going to take some time to scale up and is going to increase the total addressable market, certainly in mobility and delivery and freight as well. So we think increasing supply can actually improve our marketplace overall. We’re already working with over 10 autonomous players in the mobility delivery categories. We’ve had a few. We work with Waymo, but we’ve had a few cool announcements recently in terms of announcing that we’re going to be working with Cruise. And as they expand their offerings and relaunch and, for example, a company called Wayve in the UK which is building kind of underlying newer AI-based technology, self-driving technology. We think it’s absolute best-of-breed technology. And if anyone’s in the UK, I would encourage you to take a ride in one of their vehicles. It’s pretty amazing. And I personally like I’ve been to the UK, I’ve been to China, et cetera, but I would just comment that from a software basis, we think that technically the software is going to get to a very good place over the next three to five years. Hardware and scaling and thinking the economics work is going to be a lot more work. And based on what we see, there are going to be multiple providers and multiple winners in the space, so to speak. It’s not going to be a winner take all market. In terms of what we provide, the autonomous players, we’re already seeing with autonomous players that we work with, we’re able to drive much higher utilization of those assets. And those are very expensive assets. They need to — these have been multibillion dollar investment cycles over for many of these players over 10-plus years. So with the volumes and the higher utilization that we can drive through the marketplace versus standalone, we think they can earn their capital back both on investment and earn a return on capital on the vehicles that they have. And we’re seeing it live right now in the marketplace. And specifically, some examples of higher utilization are, we have a dynamic dispatch layer where if you request an Uber, we will dispatch an autonomous vehicle to you only if that autonomous vehicle has a pickup zone or a dropoff zone that’s within a block or two of where you’re being picked up and where you’re being dropped off. So the reliability of that car is very, very high, and the ride is the exact perfect ride that you want it to be. We will dispatch an autonomous vehicle when the autonomous vehicle is close to you, right? So if you have a 15-minute ride and you have a 15-minute pickup time versus a 15-minute ride and a two-minute pickup time, the latter autonomous vehicles, utilization is much, much higher than the former. That can make a huge difference, especially if you’re buying tens of thousands of these vehicles, especially if you have leverage on these vehicles, the return on investment of the car with a two-minute pickup, average two-minute pickup is much higher than the other cars. And then we can shape demand and supply in that we are — we position our drivers, et cetera. So during peak times, you can have a hybrid network that’s partially autonomous, partially manned, so to speak. And we pay our drivers only when essentially those drivers are utilized versus an autonomous system where you have to pay for the vehicle 100% of time. So an autonomous player who is playing with us can essentially build up their fleet to perfect utilization and we can move up demand — we can move up supply in a dynamic basis based on whether it’s a concert or whether it’s rush hour, et cetera, and make sure that during rush hour, you can get your Uber, but it doesn’t cost you too much to kind of overbuild in terms of hard assets. So the increase in utilization, the increase in ETAs and reliability and demand and supply shaping are something that we bring uniquely, we bring it at scale, we bring it all over the world. And we think it’s a reason why many, many autonomous players are choosing to work with us, including the leading players. And we will have more announcements over the next weeks and months in terms of the expansion of this autonomous marketplace. But we’re very optimistic about the technology like it is coming. We want to help it scale and we especially wanted to help it scale in an economic manner.

Unfortunately for Uber, it is not only its ride-share business that is at risk. There are several well-funded startups working on autonomous delivery as well. Some have even launched pilot programs, such as Nuro’s grocery delivery test pilot with Kroger (KR).

Kroger’s Website

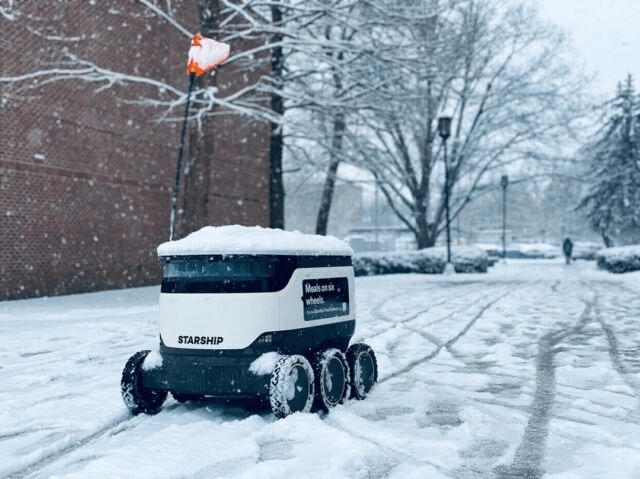

In other countries autonomous delivery is almost becoming ubiquitous, with Estonian startup Starship claiming to have completed more than 6 million deliveries already, and their robots now regularly seen on the roads of Tallinn. Needless to say, grocery stores will probably find it more attractive to invest in a fleet of robots like these ones, rather than pay Uber or Instacart (CART) a hefty commission.

Starship Website

Financials

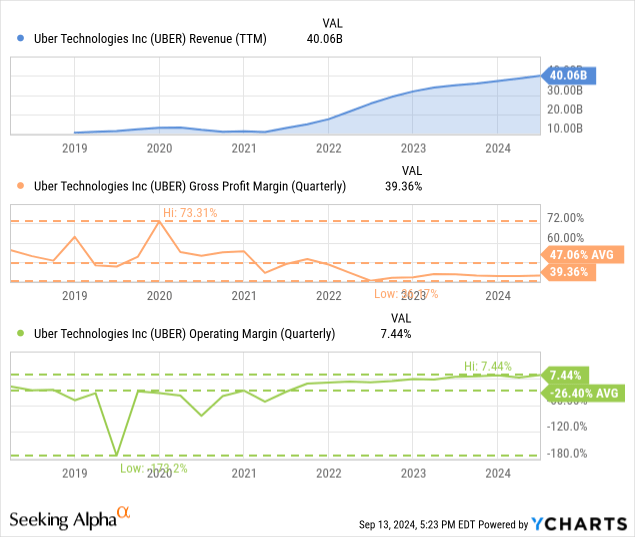

Uber’s revenue has significantly increased since its IPO, largely thanks to the rapid growth of the food and grocery delivery business. However, this is a business with worse unit economics, and has resulted in a declining gross profit margin.

Still, thanks to operating leverage, the company now has a positive operating margin, but it is nothing to write home about as it remains in the single digits. Uber has also benefited from income earned on the cash and short-term investments it holds, with an analyst recently calculating interest income representing about 14% of Uber’s free cash flow.

YCharts

Decelerating Revenue Growth

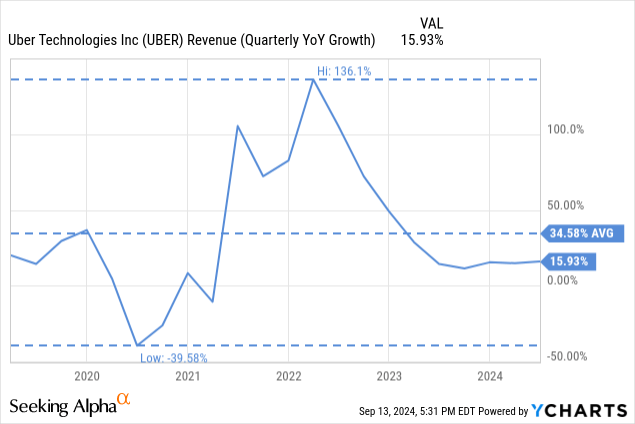

While its revenue growth has been impressive the last few years, it has been rapidly decelerating. It is currently at less than half what the company has averaged since its IPO, and we believe many of the levers it pulled to increase revenue are basically played out. In particular, we believe it will be extremely difficult for Uber to meaningfully increase further its take-rate without significant push-back from drivers, restaurants, and other partners. With signs that the consumer is weakening in the U.S., we would not be surprised to see further revenue deceleration, as people cut down on discretionary spending by going out less often to bars and restaurants.

YCharts

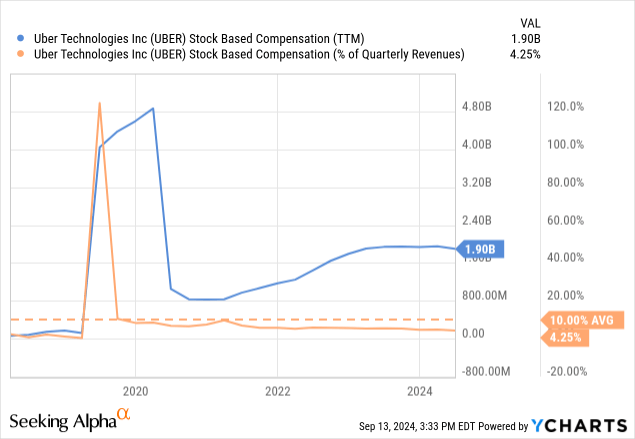

Stock-based Compensation (SBC)

Uber is also diluting its shareholders in a very significant way, with trailing twelve months stock-based compensation of about $1.9 billion. This is approximately 4% of its revenue, which might not sound like much, but it is very significant given that the company has an operating margin in the single digits. A very significant portion of this compensation goes to upper management, with just CEO Dara Khosrowshahi recently unlocking roughly $136 million after meeting a valuation target set at $120 billion.

YCharts

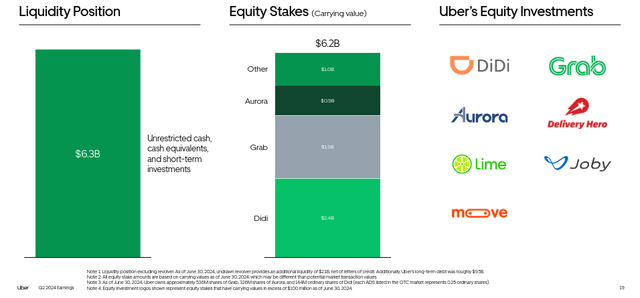

Other Investments

If autonomous driving and autonomous delivery come to disrupt the industry, they will also impact some of Uber’s equity investments. These include its stakes in Chinese ride hailing company DiDi Global (OTCPK:DIDIY), Grab Holdings (GRAB), and Delivery Hero SE (OTCPK:DELHY). It also has a meaningful investment in Aurora Innovation (AUR), which is working on self-driving technology but so far, has not really delivered.

Uber Investor Presentation

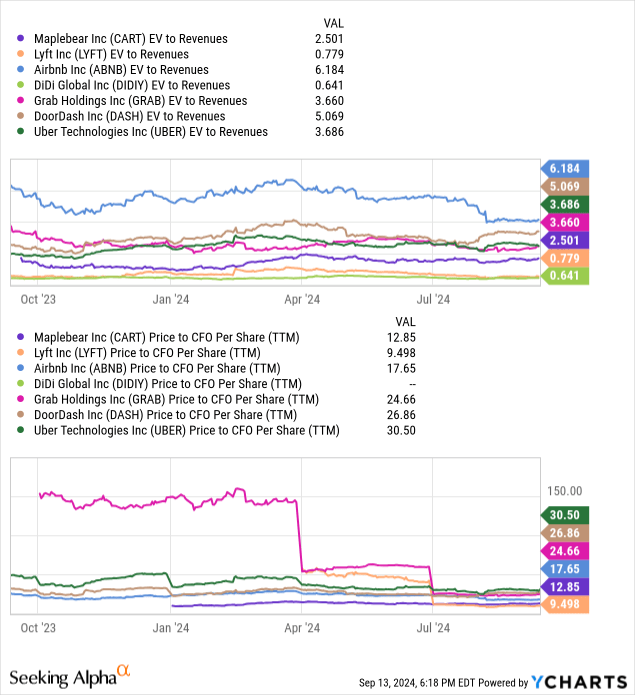

Valuation

Compared to peers, Uber has one of the highest EV/Revenues multiples, which we do not think is deserved given its low profit margin and recent revenue growth of only 16%. It is also trading with a very high price to cash flow from operations, almost twice that of Airbnb’s, which has significantly better profit margins. At current prices, we find shares unattractive, especially when considering the multitude of risks the company faces.

Risks

Uber is a company with a huge number of risks that go from changing regulations in the different countries where it operates, to difficult relations with its drivers and the cities where it operates, and intense competition. Competition is particularly intense in the food and groceries delivery business, with companies like DoorDash being particularly tough competitors. In addition to this already long list, we would add a high valuation and decelerating revenue growth.

Looking further into the future, we view autonomous vehicles as more of a threat than a potential benefit to Uber, as they could disrupt its 2-sided marketplace, enabling even car manufacturers like Tesla and GM to directly compete with Uber and Lyft.

Conclusion

Uber investors should probably be less excited and more concerned about advances in autonomous driving. This technology threatens to disrupt both its ride-share and food delivery businesses, as well as some of its main equity investments. The competitive moat the company enjoys from network effects would be significantly weakened, and barriers to entry into the business would become very low if the companies controlling the technology decided to license it or sell subscriptions to the software. Uber shares also appear overvalued when considering its low profit margins and decelerating revenue growth.

Editor’s Note: This article discusses one or more securities that do not trade on a major U.S. exchange. Please be aware of the risks associated with these stocks.

Read the full article here

(NASDAQ:META)")

")

")