")

")

: Back To Its Margin Expansion And Hyper Growth Path")

")

Introduction

My last look on Twist Bioscience (NASDAQ:TWST) followed their Q3 2023 earnings report. The article painted a mixed picture, highlighting the company’s innovative growth prospects despite challenging finances. I concluded with a “hold” recommendation, noting:

Current investors may see reason to maintain their positions and monitor the company’s progress toward profitability and reduced expenses, while potential new investors might approach with caution, keeping a close eye on the evolving financial landscape.

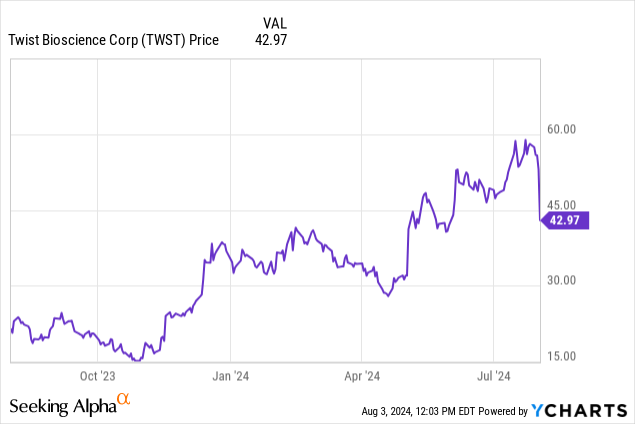

TWST is up 87% since last August. One would believe this reflects significant growth and developments, so let’s take a closer look at Q2 2024 earnings.

Twist Bioscience: Improved Margins but Ongoing Financial Strains

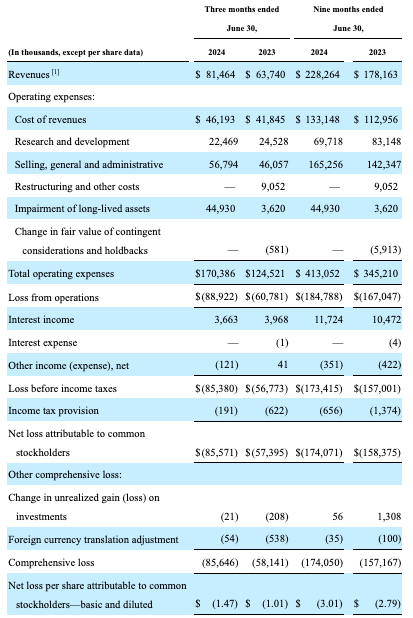

The company reported revenue of $81.5 million in Q2 (fiscal Q3), marking a 28% increase from Q2, 2023. This beat analyst estimates by ~$4 million. However, EPS missed, coming in at -$1.47, well below $-0.74. For fiscal Q4, Twist raised their revenue estimates to “$82 million to $83 million, compared to the previous estimate of $77 million to $80 million.”

Let’s take a look at the income statement.

Seeking Alpha

As Twist pointed out themselves, gross margin did see major improvements in Q2 (43.3% compared to 34.4%). This implies the company is operating more efficiently than it was last year. Improved gross margins are the result of the company’s efforts towards optimization, aiming for >50% by the end of fiscal 2025. They are also a result of growing demand in their next-generation sequencing [NGS] segment, which saw revenues grow 31% year-over-year to $43.4 million, driven by demand from clinical customers in liquid biopsy and rare disease diagnostics. However, the NGS market is highly competitive and driven by rapid technological advancements, necessitating consistent and robust R&D expenditures. Competitors like Thermo Fisher Scientific (TMO) and Illumina (ILMN) dominate these markets, thanks to continuous innovation and robust technological platforms, making it difficult for smaller companies like Twist to make too much of a dent (see Pacific Biosciences and Genomic Health as prime examples).

Twist’s future remains very much reliant on its synthetic biology segment, which differentiates the company from others, but faces uncertain prospects. Indeed, Twist’s proprietary silicon-based DNA synthesis platform offers theoretical advantages in speed, cost, and scalability. However, there are a number of other companies, such as CustomArray (GenScript), Evonetix, and Synthomics, leveraging silicon or semiconductor-based methods. Moreover, traditional DNA synthesis methods benefit from existing infrastructure, broad acceptance (established standards for quality and safety), ongoing technological improvements, and regulatory familiarity. So, within the competitive landscape of silicon- or semiconductor-based methods, its ascent over traditional methods is not guaranteed.

Within this context, Twist’s R&D expenses falling from $83 million (2023) to $69 million (2024) in the nine months ended June 30 are unlikely to be a positive indicator of growth and market leadership, but rather a sign of a company with limited resources.

The $44.9 million impairment charge was the kicker in Twist’s earnings report and the cause of the EPS miss. The company pointed out during their earnings call that the impairment charge was related to a more realistic take on the “long-term growth forecast” for their biopharma segment, which has performed poorer than anticipated. The biopharma segment was anticipated to be a significant driver of future growth for Twist. This likely accounted for the 19% drop in Twist’s stock.

Financial Health

As of June 30, Twist had $239.142 million in cash and cash equivalents, $50.276 million in short-term investments, $361.831 million in total current assets, and $73.757 million in total current liabilities, indicating that the company can easily meet its short-term obligations.

Twist is not profitable, so I will provide a cash runway estimate based on historical data. Their comprehensive loss for the nine months ended June 30, 2024, was $174 million, implying a cash burn of around $58 million per quarter. If we divide their cash equivalents and short-term investments by this figure, we get approximately 5 quarters of a runway.

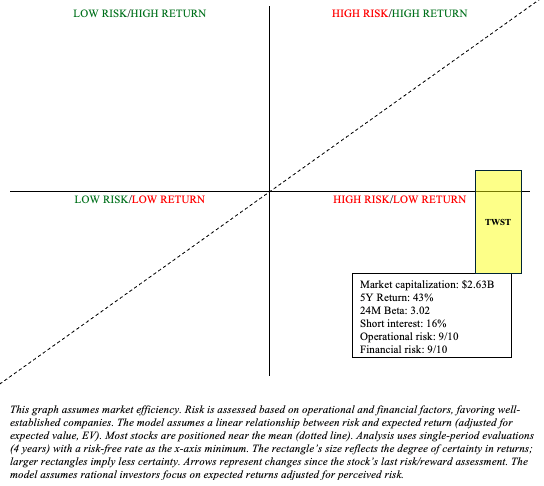

Risk/Reward Analysis and Investment Recommendation

In conclusion, while Twist’s stock has been up significantly since my last look, their outlook has diminished (e.g., biopharma segment), and their financial performance, although marginally improved, is still quite poor (e.g., consistent and ongoing net losses). Furthermore, their cash reserves are running uncomfortably low in light of their ongoing expenditures, causing the company to reduce their R&D investments, which are critical to staying relevant in a competitive and rapidly evolving market like DNA synthesis.

There is significant operational and financial risk involved with TWST. It cannot be overstated. This likely explains the high short interest and the volatile price movements.

Author

It’s difficult to envision Twist coming out of this without significant operational changes in the near future. As such, I feel it is necessary to downgrade TWST to a “sell.”

There are risks associated with my “sell” recommendation. The main one is the opportunity costs associated with the stock outperforming the market, which it has been doing since my last look in August. After all, Twist’s technology is innovative and forward-thinking. Finally, they may overcome their financial constraints through a variety of strategies (e.g., achieving profitability in operations, partnerships, and debt financing).

Read the full article here

")

")

: Back To Its Margin Expansion And Hyper Growth Path")

")