")

")

")

")

Pet Insurance has been a rising industry over the last decade. Back in 2016, Forbes reported on the rising trend of millennials to prefer getting pets to having children. A more recent report indicates that this has continued and that Gen Z is joining in on it. When secular changes like these occur, investors naturally wonder who is poised to make money on that and how they can get into it.

Trupanion (NASDAQ:TRUP) gives folks a chance to invest in pet insurance. Yet, I will argue that a rising trend doesn’t necessarily have profitable economics. Ultimately, I regard the stock to be a SELL until I see a substantive change.

Financial History

Let’s look at how the company spent the last decade riding that trend. I’ll include YTD reported data for 2023 as well.

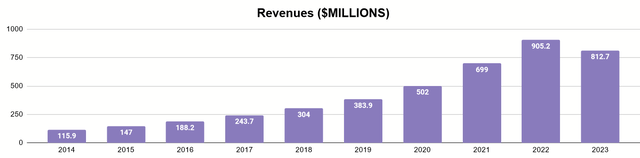

Author’s display of 10K/10Q data

Revenues experienced wild growth, up almost 8x. Yet, a look at their earnings shows that it’s not been that simple.

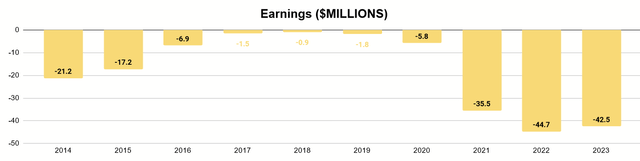

Author’s display of 10K/10Q data

Initially it seemed that the company was successfully scaling its model and about to break into profitability. That trend began to reverse itself in 2020 and took heavier tolls in the years after.

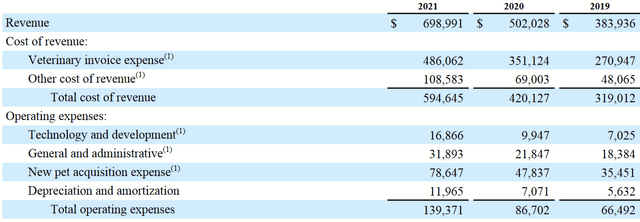

2021 Annual Report

Revenue increased 82.1% from 2019 to 2021. Yet, cost of revenue rose by 86.4%. Operating expenses rose by 110%!. With costs rising across the board well in excess of revenues, the company’s negative margins only increased. This got worse as inflation persisted in 2022, along with other macro-challenges that year. Darryl Rawlings (Chairman & CEO), noted this in the Q3 2023 earnings call:

Coming out of COVID in 2022, the cost of veterinary care began to quickly accelerate. Within a period of less than 10 months, veterinary inflation increased an additional 900 basis points over historical norms. While this rapid rise in the cost of veterinary care was unprecedented in 50 plus years at Trupanion, we were slower to react than I would have liked.

The extra 900 basis points of inflation had a material impact. Adding to this challenge our current policy terms means it takes us 12 months to 18 months to reprice our existing members. In 2020 and 2021, our annual adjusted operating margin for our core subscription business was 13.9% and 14.3%, respectively. After this rapid change in veterinary inflation, this same margin compressed sequentially four consecutive quarters until we hit a low of 7.6% in Q1 of this year.

I will highlight, though, that Pet Acquisition Expense (the cost to acquire new pets in their customer accounts) is a major part of this operating expense.

Author’s display of 10K/10Q data

In spite of those consistent losses, the company has been growing the assets on its balance sheet, largely done by selling new shares. The biggest instance of this was in October 2020 with Aflac, which acquired about 9% of the company in a $200m transaction. This represented the start of a Strategic Alliance between the two, wherein Aflac bundles Trupanion’s health insurance with other products in its existing networks. The reserve cash provided to them made navigating the recent years possible. Aflac has defended this alliance, restating its commitment in December 2023.

Insurance Business

Given these troubling numbers, now might be a good time to look at what exactly is entailed by pet insurance.

Company Website

The insurance offered is for the healthcare expenses of dogs and cats, which makes up their Subscription Business. These subscriptions are paid primarily on a monthly basis. When a customer incurs an expense at a vet, this typically involves an invoice being sent directly to Trupanion.

Q3 2023 Earnings Release

Most of the cost of revenue comes from this process specifically. This is why the pricing power of vets squeezed the company’s margins recently, as they await approval from state governments.

Company Website

Expenses can cover just about everything a pet owner might need to insure their pet. As such, it has a reasonably attractive product for customers. What kind of costs are customers experiencing with this?

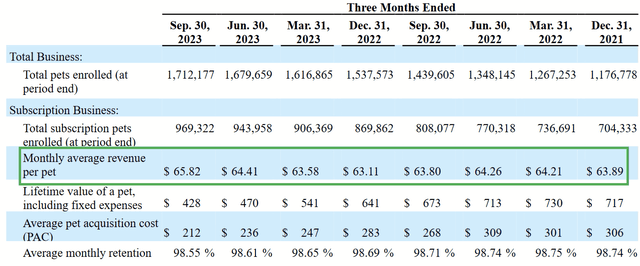

Q3 2023 Earnings Release

This table shows us that they are usually getting around $64 per month per pet ($768 per year).

Q3 3023 Earnings Release

Seen above, this Subscription Business accounts for a majority of all revenues. The Other Business is not insignificant, though. While Subscription is direct-to-consumer, this segment operates on a B2B model and involves their agents underwriting policies for different brands.

A Look to the Future

Overall, I see a lot of risks with buying into this company, but I’ll be sure to go through what I think are the good and bad things.

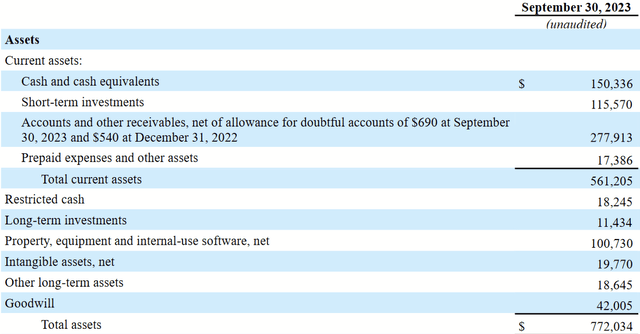

Balance Sheet

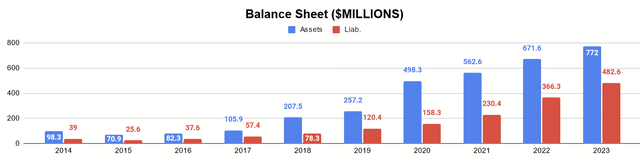

This balance isn’t exactly loaded with a lot of liabilities that could result in a liquidity crisis. The tangible book value is $227m. Yearly losses haven’t been more than $50m, so there’s some breathing room there.

Balance Sheet (Q3 2023 Earnings Release)

If we look at the assets from their latest balance sheet, almost none of that is in long-term investments. This shouldn’t be a surprise, given the financial history I discussed. Typically, an insurer takes their earnings and reinvests those in bonds and equities to compound the business’s value over time without recklessly originating riskier policies. As such a portfolio grows, its assets can be liquidated to rescue the company in a pinch and serve as an extra source of income in the meantime. An insurer’s TBV is often defined to a significant extent by investment portfolio.

Accounts receivable is the biggest asset on Trupanion’s book, a number that may not always prove to be what is reported. Realistically, this company will need a bailout if it runs into trouble.

Turn To Profitability

From what I can see, the main thing that will allow a switch to profitability is stabilizing their operating expenses, especially the cost of acquiring new pets. The rise of that cost alone over recent years accounts for most of their reported losses. At some point, the company needs to ease back on expensive growth and try to convert it into positive cash flow.

At the same time, doing this effectively doesn’t protect them from getting squeezed by veterinary price hikes, as was discussed in Q3 earnings. The company needs to have more generally aggressive pricing than it’s had in the past to account for this risk. Naturally, this might turn off customers. That brings me to the last point.

Unnecessary Product

I grew up with several dogs. My family took special care of them, with regular trips to the vet. I recognize, however, that my family was exceptional and that most people do significantly less, which again is part of the appeal. Pets are low-responsibility, emotional investments for young adults who don’t have financial independence to raise children. People can dote upon them as if they were children, but it’s generally accepted that they will get sick and die well before we do.

Unlike car insurance and homeowner’s insurance, there are no laws, ordinances, or others rules that tend to require us to purchase these things. The moral and legal weight when homes burn down or cars crash is much more than when a pet gets sick. Mothers Against Drunk Drivers exists for a reason. I don’t think we’ll ever see Dog Moms Against Drunk Drivers. Given these things, I believe it will always be easier for customers to drop pet insurance if they find themselves needs to save more.

Put more briefly, even if the business turns profitable, I don’t it’s needed badly enough that it would be a durable stream of earnings. In fact, these realities are probably the reason that it hasn’t been.

Valuation

With no earnings in its history, this is a tough business to value. Normally, you can at least value an insurance business by TBV per share. As of Q3 2023, that’s $5.47, substantially less than the current price. Since this number will decline as negative earnings continue, an investor would only benefit if they were getting a significant discount to that as well. TRUP’s current valuation north of $27 just doesn’t offer any margin of safety to owners.

Conclusion

Trupanion seized on an emerging opportunity to profit from the rising rate of pet ownership among Generations Y and Z, as they increasingly use it as an alternative to parenthood. They have a very sophisticated, tech-savvy business operation.

However well-oiled the machine is (and it really seems like it is to me), the company hasn’t priced itself effectively to account for the costs of running this type of business. Given how nobody truly needs pet insurance and how it can be easily dropped when times are tough, I suspect this is the reason why. As such, while some may see a profitable investment here, even Aflac, I am not convinced. Until costs (particularly those of acquiring new pets) can be lowered or stabilized, the company is a SELL for long-term investors.

Read the full article here

")

")

")

")

")

")