")

")

")

(Note: all amounts in the article are in EUR. At the current exchange rate, 1 EUR is around USD 1.11.)

Investment thesis

thyssenkrupp (OTCPK:TKAMY) (OTCPK:TYEKF) is a German holding company with a variety of industrial holdings, the largest by far are the European Steel and the Materials divisions, which produce and trade steel and steel products.

I wrote an article on thyssenkrupp in April last year, saying that thyssenkrupp Does Not Know What Kind Of Company It Wants To Be. The gist of the article was that, while the company looks undervalued, there is no clear way for shareholders to profit from this because of the ongoing discussions about the strategy of the company and the future of the large steel division.

Since the article was published, thyssenkrupp shares are down 50%. I also predicted that the upcoming IPO of thyssenkrupp nucera (OTCPK:THYKF) would not benefit shareholders. thyssenkrupp nucera shares now trade at around EUR 9. The IPO price was EUR 20, and all the money raised in the IPO (almost EUR 600mn) went to thyssenkrupp nucera. thyssenkrupp itself got nothing from it.

The last years have been painful for thyssenkrupp shareholders. The market cap has eroded from a high of EUR 30bn to barely EUR 2bn now.

Source: Seeking Alpha

All this time the company has been a turnover candidate, but the turnover never materialized. The EUR 2bn market cap is astounding, as the company has a net cash position of EUR 3.2bn on its balance sheet. The market seems to attach a negative value of over EUR -1bnto the business. The number gets even worse when we consider that thyssenkrupp owns 50% of the publicly traded thyssenkrupp nucera which has a market cap of EUR 1.15bn.

A multitude of problems is dragging the company down:

1) There is an ongoing discussion about the future of the steel division. The company needs to put a lot of money into the green transformation of its steel business, money it does not have. So, it needs to rely on government subsidiaries, which limits the options thyssenkrupp has when it comes to restructuring or divesting its steel subsidiary. The discussion of whether and how to divest the steel business has been ongoing for years without a positive conclusion. The ugly truth is that thyssenkrupp does not have the money to keep the business running, and it does not seem to have the money to get rid of it. The company carries enormous pension obligations on its balance sheet and has chronically underinvested in its industrial footprint. Pension obligations amount to EUR 5.6bn and are growing (they are up 3% over the three quarters of the current fiscal year). Property, plants, and equipment amount to less than the pension obligations with only EUR 4.85bn, and this value is decreasing due to depreciation and amortization (-2% in the first nine months of the fiscal year).

2) The other business segments aside from Steel are not doing especially well either. Of the five business segments – Automotive, Decarbon Technologies, Material Services, Steel Europe, and Marine Systems, – only two had positive FCF in the last quarter.

3) Even if the discussion around Steel concludes somehow in a beneficial way for shareholders, there is still the strategic question: What company does thyssenkrupp want to be? The previous CEO Martina Merz, who was forced to resign, used to call thyssenkrupp a group of companies. The current CEO Miguel Ángel López Borrego still needs to explain how this is more than a different name for a holding company of loosely related businesses.

Until all those problems are solved, or at least until investors can see a path forward to a solution, I suggest staying on the sidelines. The valuation looks cheap, but it did look that way for a while now. Even if shares do not fall further, thyssenkrupp shares may provide trading opportunities in the short term, but it looks like dead money in the longer term.

Financial result in fiscal Q3

Note – thyssenkrupp has an irregular fiscal year from October to September. Q3 of the fiscal year 2023/2024 is the second quarter of 2024.

Results were bad and below expectations, and thyssenkrupp management agrees with that assessment, referring to the challenging market environment. thyssenkrupp incurred a net loss of EUR -33mn, compared to a net profit of EUR 107mn in the previous year. It was the fourth consecutive quarter with a net loss. FCF was also negative and EUR -203mn, compared to a positive EUR 608mn in the previous year. Q1 and Q2 of this fiscal year also had a negative FCF.

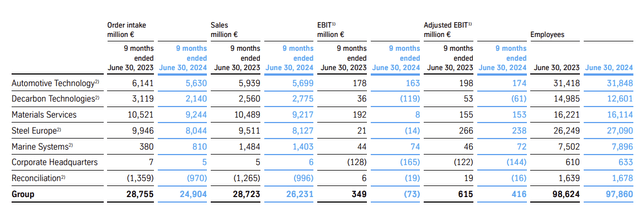

Sales were down and the intake of new orders was down too, which is especially disappointing.

Order intake was down in all segments except Marine Systems, both in Q3 and in the first 9 months of the fiscal year (Q1-Q3). In total order intake was down 11% in Q3 YoY and 13% in Q1-Q3. The book-to-bill ratio was below 1, although sales were also down in all segments except Decarbon Technologies. Sales in Q1 were EUR 9bn, -9% YoY, and EUR 26bn in Q1-Q3, -6% YoY.

Source: thyssenkrupp

So, most numbers in Q3 and the first nine months of the fiscal year were not good. The outlook for the full fiscal year (Note – due to the irregular fiscal year there is only one quarter left) does not foresee an improvement. thyssenkrupp expects revenue to decrease by 6-8% for the full year, versus the -6% in Q1-Q3. Adjusted EBIT is forecasted to be >EUR 500mn. It was EUR 416mn in Q1-Q3. It looks like Q4 will also see a net loss, which would make it the fifth consecutive quarter with a net loss.

Divestment of the steel subsidiary runs into problems

Thyssenkrupp Steel Europe is the largest steel manufacturer in Germany and employs around 27,000 people in its steel subsidiary. However, since the merger of Krupp and Thyssen in 1999, thyssenkrupp wanted to divest the cyclical steel business, with no success so far. When times are good, the steel business can bring in a lot of money, but when times are bad it drags the rest of the company down with it into a loss. Currently, it looks again like times are not so good. Overcapacity in China is hurting steel producers across the globe and leading to lower prices.

The new CEO López is pushing for a divestment rather sooner than later, which creates tensions with the works council and the powerful IG Metall union. Recently, internal disputes between the CEO of the steel division Bernhard Osburg and López have become public, too.

20% of the steel division has been sold to the Czech investor Daniel Kretinsky, and the target is a 50:50 ownership structure. The sale was done against the votes of the works council, which – as is the law in Germany – is represented on the supervisory board of the company.

Kretinsky owns significant fossil fuel assets across Europe, especially coal. Still, thyssenkrupp thinks that he will help in the green transformation of the Steel business. He may as well be the only one interested in the business as all other parties that thyssenkrupp has been talking to have declined. After years of efforts, the best his predecessor Merz managed to come up with was an unofficial offer of EUR 1 from the finance investor CVC.

There are two open issues, overcapacity (and how to resolve this, especially regarding job cuts), and the financial resources provided by the parent company for the division when it becomes independent. thyssenkrupp wants to get rid of the steel subsidiary as cheaply as possible, and it seems that Lopez and Osburg cannot agree on how much money the parent company needs to put into its subsidiary to make it financially independent. The quarrel resulted in an extraordinary step: According to the German newspaper Handelsblatt (article in German), López wants to have the steel subsidiary’s ability to be restructured checked by an external auditor. The outcome of this could trigger an exit clause Kretinsky apparently has in the contract with thyssenkrupp, getting López back to the starting point.

Whatever the outcome, it does not look like the issue will be solved quickly and it will most likely drag into next year. In my view, shares will not move up significantly before thyssenkrupp has found a way forward here.

I could be wrong and thyssenkrupp could find a positive solution quicker than I think. However, the worst-case scenario is that the steel business deteriorates further and thyssenkrupp will have to finance large losses in the next years. Then its future may be similar to that of another European company with a long and illustrious history which Kretinsky wanted to take over cheaply, the French IT company Atos SE (OTCPK:AEXAF, OTCPK:AEXAY). After a years-long decline, Atos shareholders are looking at an almost complete loss of their capital. To be clear, I am not predicting this outcome for thyssenkrupp, but the risk/reward ratio does not look favorable to me.

Conclusion

With a market cap of now just under EUR 2bn, thyssenkrupp looks cheap. However, there is a list of issues and open questions. The balance sheet shows net cash of EUR 3.2bn, but a deeper look reveals that pension obligations of EUR 5.6bn are not considered here.

The discussion about the future of the Steel division is unlikely to conclude this year. The other business segments do not perform well enough to compensate for the uncertainty, and there is the open strategic question of whether thyssenkrupp wants to be more than a holding company of loosely related businesses.

All this does not make for a compelling investment case, and it seems better to stay on the sidelines for now.

Editor’s Note: This article discusses one or more securities that do not trade on a major U.S. exchange. Please be aware of the risks associated with these stocks.

Read the full article here

")

")

")