")

Economic data may be more important this week than the Federal Reserve or Bank of Japan meetings and could prove to be a big pivot point for markets. That’s because the yield curve has been steepening, taking its cues from the job data. Typically, the curve steepens when the labor market shows signs of slowing. If the labor report and JOLTS continue to show slowing in the labor market, it will likely lead to further steepening of the yield curve.

For July, analysts forecast non-farm payrolls rose by 178,000, down from 206,000, with the unemployment rate expected to remain unchanged at 4.1%. Meanwhile, average hourly earnings are forecast to rise by 0.3% m/m, in line with June, and by 3.7% y/y, down from 3.9% last month. Additionally, the JOLTS data is expected to show that job openings in June fell to 8.05 million from 8.14 million in May.

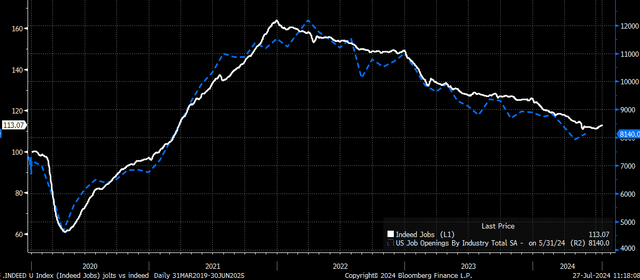

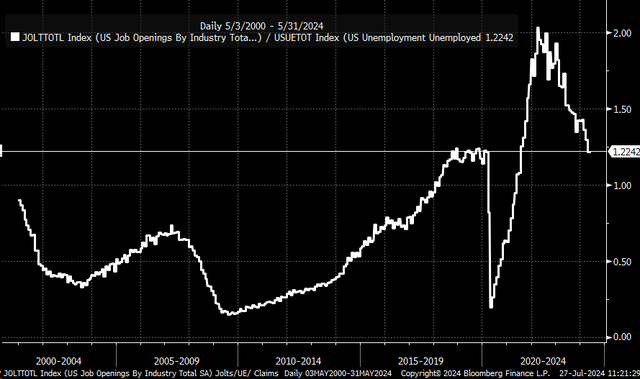

JOLTS

Data from Indeed shows that job openings in June fell relative to May. However, the data is also showing an uptick in July. This would be an important change in trend if it were to persist into August. Certainly, one month is not a trend. However, the Fed has made much progress in bringing the labor market back into balance, and the JOLTS data is not always consistent with the indeed on a month-to-month basis.

Bloomberg

The May JOLTS data showed that the ratio of job openings to the number of people unemployed fell to 1.22, which was back in line with pre-pandemic levels. Historically, this is still a very high level, so while the labor market is slowing, it remains healthy.

Bloomberg

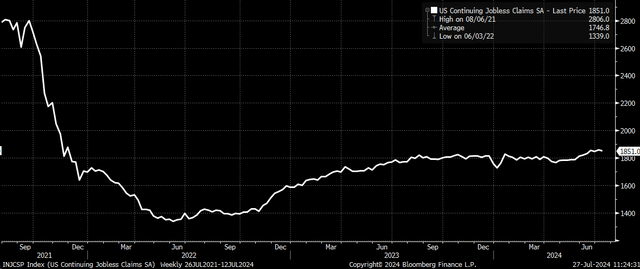

Unemployment

This has also come as we see the weekly initial jobless claims ticking higher and continuing claims rising to the highest levels since 2021. This is an indication that while the job market remains healthy; it is slowing down, and it is becoming harder to find jobs.

Bloomberg

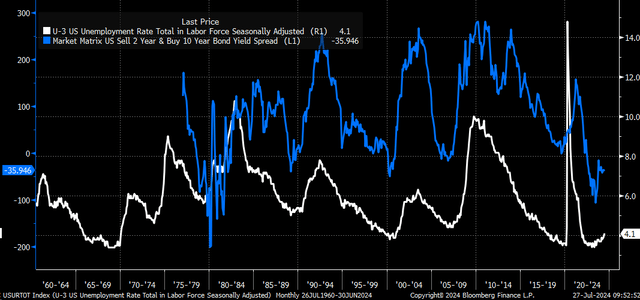

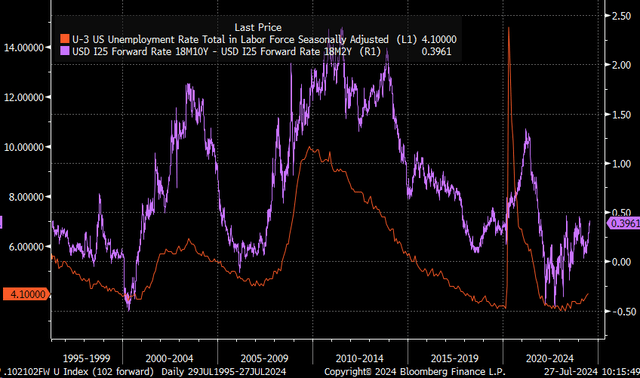

The yield curve also suggests the job market has slowed because, historically, it steepens and comes out of inversion in anticipation of the unemployment rate rising. This takes the form of the 2-year rate falling faster than the 10-year rate. An unemployment rate that remains at 4.1% or higher will confirm the bond markets’ recent steepening and could even result in the yield curve steepening even further.

Bloomberg

Yield Curve

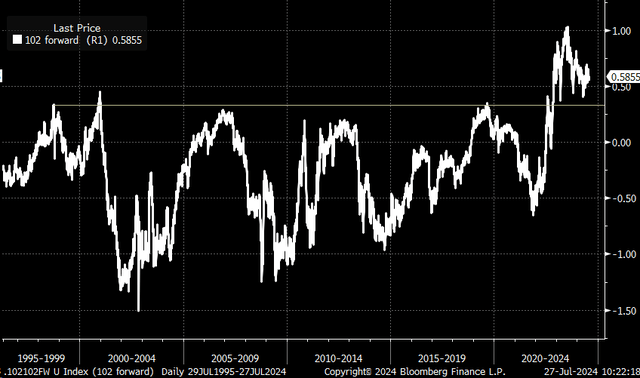

We have also seen the 10-year minus 2-yr 18 mo. forwards already steepen and move back into positive territory at 39 bps. This is the third time the forward curve has moved into positive territory, and more importantly, it has been steadily trending higher over the past year. Historically, the 18-month forward curve has also been a reliable predictor of not only the unemployment rate but also the steepening of the spot 10/2 curve.

Bloomberg

Currently, the spread between the 18-month forward 10/2 and the spot 10/2 spread is 58 bps, which is historically wide. This suggests that the spot curve could move higher and faster over the near term. Additionally, the spread between the two, should it normalize, would be around 35 bps, suggesting the spot curve steepening to around 0 bps, meaning an equal 2-year and 10-year rate.

Bloomberg

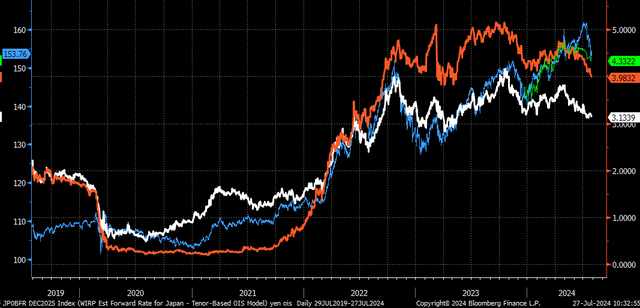

This could be especially important because if the steepening continues in the form of the 2-year fall, it could work to unwind the carry trade further, potentially strengthening the Japanese yen versus the dollar as the market prepares for a Fed rate-cutting cycle. Currently, the yen is traded based on interest rate differentials, whether it be overnight, 2-year, or 10-year rates.

The spread between the US 2-year Treasury and 2-year JGB rates is falling fastest. So, if the US yield curve were to steepen further and came in the form of the 2-year Treasury falling, it would pressure the yen carry trade further.

Central Bank Policy

Some of the carry trade fate may also be determined by the Bank of Japan meeting later in the week and how they signal the future path for monetary policy and bond buying. If the bank comes across as more dovish or opts not to raise the overnight, yields in Japan could fall, causing spreads to widen again and push the USDJPY higher. However, given how low rates are in Japan currently and how much of the yen depreciation has been based on higher US rates, falling US rates are far more important to the carry trade.

Bloomberg

The Fed will come into play this week, too, because if the Fed signals a bias towards potentially cutting rates in September, it could also steepen the yield curve as 2-year rates fall faster than 10-year rates. But if the Fed should remain resolute and indicate it still requires more data to gain the confidence to cut rates, it could make for a tricky situation, especially if the job data disappoints.

Right now, the focus is on the yield curve, and this week’s data will play a critical role in shaping it.

Read the full article here

")

")