")

All eyes will turn to Jackson Hole later this week and what Jay Powell has to say about the path of monetary policy. Meanwhile, the more important speaker of the week may come hours before Powell takes the stage and more than 5,000 miles away when Bank of Japan head Governor Kazuo Ueda appears before Japan’s parliament.

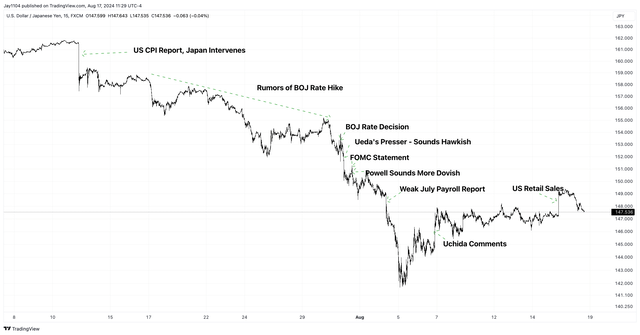

The Japanese yen and carry trade, the act of borrowing in a low-interest rate currency to invest in a higher-interest rate currency, have captured headlines in recent weeks, given the sharp decline of the USD/JPY, the exchange rate between the US dollar and Japanese yen, a sign that the US dollar is weakening versus the Japanese yen. The yen started to strengthen following the July 11 weaker-than-expected US CPI report, followed by a Japanese government intervention in the FX market. The USD/JPY continued to decline as fears grew that the BOJ might raise rates at its July policy decision.

That was followed by weak US employment data on August 2, which sent the USD/JPY plunging, causing risk assets globally to fall. The only thing that appears to have saved the USD/JPY from falling even further was BOJ deputy governor Uchida signaling the bank downplayed the chase for further rate hikes in the term, while indicating the bank would not raise rates during periods of market volatility.

TradingView

Governor Ueda has been called before the Parliament to discuss the Bank’s decision to raise rates on July 31 and the path forward. The question is how he will sound during this session, and whether he will signal that rate hikes are likely to still come in the future. Generally speaking, that had been the view, but some are wondering if the recent market volatility will get him to walk some of that back.

To add more confusion to the mix, Prime Minister Kishida has decided not to run for re-election, and the fear is that political players who may step in to fill the void may have views that are more supportive of the yen, which would imply that the USD/JPY would move lower.

While most of the focus has been placed on the BOJ decision to raise rates, one cannot forget that this all started following the weak US CPI in the middle of July and became scary after the US labor report in early August.

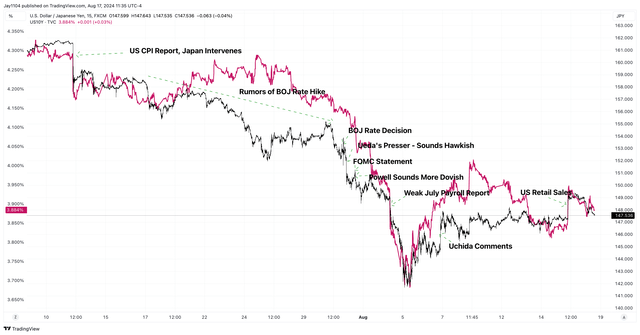

It almost appears that weaker US economic data is at play along with the Fed’s potential policy path, and less so on the BOJ’s actions. The USD/JPY has been tracking the US 10-year Treasury rate through the entire rapid decline. Was the BOJ rate decision part of the yen strengthening? Sure, but judging from the movement in the US 10-year rate, it would seem the US data may be playing an even bigger role.

TradingView

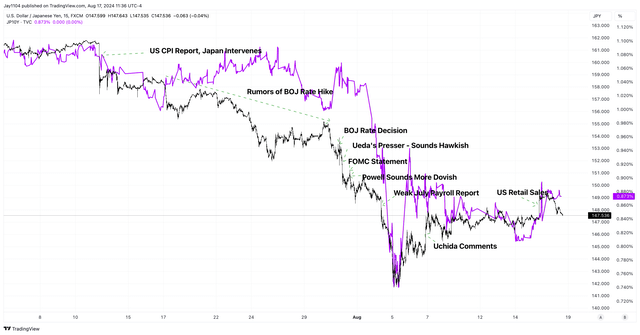

Because the spreads between US and Japanese rates have been contracting over this entire time, the strengthening of the Japanese yen is likely due to this contraction in interest rate differentials.

TradingView

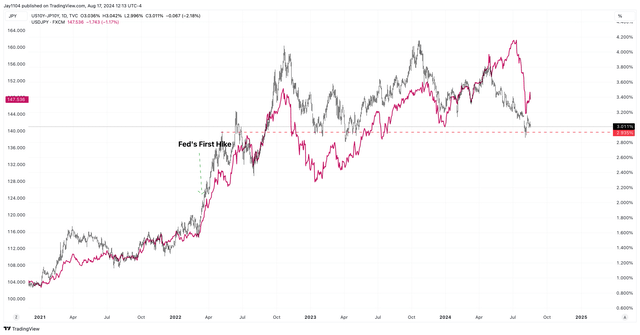

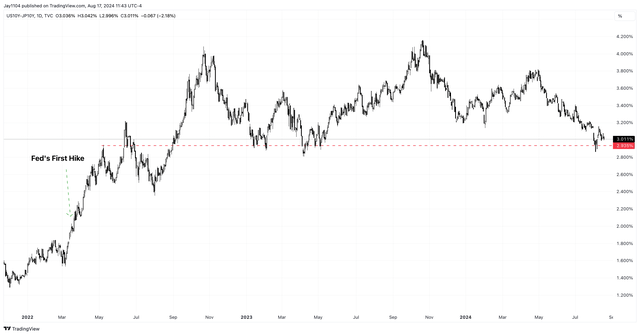

This game of USD/JPY and interest rate differentials has occurred since March 2022, when the Fed first raised interest. The USD/JPY and interest rate spreads between US rates and Japanese rates have been linked together ever since. Now that the Fed is embarking on a potential rate-cutting cycle and the BOJ is still in the middle of raising rates, these spreads are only likely to fall further.

TradingView

It would seem that technical support in the US 10-year rate minus the 10-year JGB is at an interest rate spread of 2.9%. If the spread drops below that level of support, it could lead to the interest rate differential narrowing even further, which could strengthen the yen further, pushing the USD/JPY even lower.

TradingView

This is a two-sided sword, though. What the market needs right now to keep this trade from unraveling even further is a more dovish-sounding (favoring fewer hikes) Ueda and a more hawkish-sounding (favoring not cutting too quickly) Powell this week. That would allow the USD/JPY to rise as interest rate spreads are likely to widen.

Because, as of right now, with inflation continuing to cool, the labor market softening, the Fed getting ready to cut rates, and the BOJ hiking, the yen is likely to strengthen more overtime, and that won’t be good for risk assets in general as the carry trade unwind continues.

Read the full article here

")

Q2 2025 Earnings Call Transcript")