")

")

")

Qorvo (NASDAQ:QRVO) reported strong earnings for the June quarter, but left analysts scratching their head with slightly lower year over year guidance. This guidance came after management had touted the marketplace with visions of continued ASP growth beginning in September from their largest customer, Apple (AAPL). The strong June quarter didn’t overcome the perceived weak guidance rather left us cold until we made a deeper scratch. This writing continues our generally bullish stance on the company, being, Qorvo: Report Yields A Clearer Picture For The Company And Mobile Devices. We are upgrading to a buy. Maybe we should stop scratching and hit the keyboard. Would you join with us? Now, put that hand down.

The Company

Qorvo, for the 1st time or maybe just in a long-time, included a really nice summary. We are adding relevant portions. The summary includes: the primary end markets are “automotive, consumer, defense and aerospace, industrial and enterprise, infrastructure and mobile.” Each market is “underpinned by global megatrends, including electrification, connectivity, mobility, sustainability, datafication, and AI.”

Continuing, and for the techies, management added, “Our markets are characterized by multiyear upgrade cycles, including 5G Advanced, Non-Terrestrial Networks, Wi-Fi 6 and Wi-Fi 7, DOCSIS 4.0, Matter, Ultra-Wideband and others.”

Several technical issues drive changes: low latency, speed, bandwidth, and power efficiency. One massive coming change, AI, consumes massive amounts of power, a problem especially with battery powered products. Low power usage will become more and more and more and more important going forward.

The businesses are divided into three sectors, ACG, HPA and CSG.

The Strong Year over Year Quarter

The company reported EPS of $0.87, above the high end, with revenue of $887 million, a revenue increase of 36% year over year and non-GAAP margins at 41%. Cash on hand equaled $1.1 billion with debt at $1.5 billion. $27 million of the 2024 notes due at year’s end were paid. Inventory remained relatively flat at $727 million. Materials needed for the seasonal ramp with Apple are included in the flat value. The company purchased $125 million worth of stock. Finally, the yearly tax rate will range between 10% – 12%.

Market Penetration

Qorvo ramped several new products into several customer ramps including:

- New BAW and LRT SAW processes.

- A most dense functional mid-high band pad.

- Multiple design wins in mass-market smartphones with LMH band paths.

- Significant board space saver.

- Sole MediaTek supplier for Wi-Fi 7 FEMs (DX4 products.).

- Expanded Ultra-Wideband wins in Android including a first win in a mid-tier phone.

- Fully integrating in the Anokiwave team for developing more highly integrated products.

Looking into the future for each business segment, management noted:

- ACG is focused on Apple.

- HPA is focused on defense and aerospace plus power management.

- CSG is focused on automotive connectivity, advanced Wi-Fi RF solutions and Matter/Ultra-Wideband SoCs.

In our view, Qorvo’s conferences always loaded with techie like comments indicates the importance of top end technologies and products.

AI

On the current market buzz subject, questions relating to AI, most easy to predict, surfaced. In answer, Robert Bruggeworth, CEO, stated,

“And as far as AI goes, I think, we’re taking more of a conservative approach. I mean, clearly, we saw that in what Samsung released in the S24. And just to remind the group, we’ve got excellent dollar content in that and they had a pretty nice ramp. It wasn’t tremendous above what expectations were, but they did a good job this year with the S24. Whether it was due to AI or not clearly sure. And as far as our largest customer goes, since they haven’t released their next-generation phones, we’re not going to comment. But I think as an industry, it would be wonderful if that AI came out, it was very useful for users and reduce the replacement cycle time so that we would see an uplift. . .. But that’s not what we’re modeling at this time.

Qorvo seems to be very conservative compared with Skyworks Solutions’ recent comments. They will believe it when they see it. But new technologies with higher ASPs are coming, regardless.

The Marketplace

During the call, a few comments appeared on the marketplace including this bit of in-site.

“In calendar ’24, we expect Android 5G unit volumes to grow greater than 10%. We are also positioned to grow with 5G Advanced, which occurs with new releases of the 5G standard.”

On the mobile markets, management noted:

“Turning to mobile, which is primarily smartphones and tablets, our largest opportunity remains at our largest customer. We are investing in multiple multiyear programs to increase our content and continue to grow revenue with this customer.”

With respect to Android, management also made this comment:

“Within the Android ecosystem, Qorvo remains the primary RF supplier. We collaborate with Android OEMs on their product road maps over multiple years and we are positioned to drive growth as 4G devices move to 5G . . .”

Similar to Cirrus Logic (CRUS), Qorvo seeks long-term relationships with real roadmaps for growth. These strides are measured and steady.

In the past, this 10% comment of growth in 5G conversion has appeared several times. The comment confirms this expectation at least for this year.

The Guidance Back & Forth

Now, let’s comment on the guidance which triggered an interesting back and forth between the analysts and management. The report guided September at $1.05 billion with non-GAAP margins between 46% and 47%. Margin improvement is expected to continue going forward as communicated at the last Investor Conference. Before continuing, a past look at September 2023 guidance must be included given at $1 billion. The September release posted an actual at $1.1 billion, higher by 10%.

On a revenue basis, the company guided at $1.025 billion a very slight increase year over year. It is with this issue that analysis pounced. From a very carefully worded question, Christopher Rolland of Susquehanna, asked,

“I guess, maybe getting back to the September quarter. Just a question I keep getting asked from investors is around revenue still being down year-over-year. And I think the assumption is you have content growth at your largest customer. So and perhaps we have an AI refresh cycle. I know you’re conservative there. I appreciate that conservatism. But still why not growth or at least flat year-over-year particularly in mobile?”

Grant Brown, CFO, answered with the same level of tact that “the slight decline is principally related to smartphone revenues. This change is based on the total smart phone marketplace, and we are being a little conservative.” Then, with an additional one from Dave Fullwood, Senior Vice President, Sales & Marketing, came this,

“We actually have purchase orders on the books now and that will just start to ramp at the very end of this quarter. So that will ramp up as we go through the balance of this year and into next year. So we’re — it’s kind of a timing situation happening there in the Android ecosystem.”

The answer included a commentary discussing a ramp peak with other Android vendors earlier in the year. Our take: management guided September with extreme conservatism. Either September picks up a larger piece from the new phones or the revenue slides into December beefing that quarter. Over time, it makes little difference. We believe that the market mistook the real issue once again, when it sold off the stock price steeply the following day.

The call entertained additional questions on this issue being answered with assurance of additional content with Apple, but not enough to overcome other weaknesses.

Next Year

The company offered a few comments opening more color into next year. When asked about Apple’s potential with providing its own modem chip in a test phone, the answer came back with a it won’t likely impact a path to higher ASPs. This answer came with a significantly higher level of confidence than when Skyworks was asked at its conference. Qorvo has developed a tight long-term plan with Apple. It seems integrated parts are at the heart of this development for saving board space, lowering power usage and most generally lowering costs. In the past, with Apple talking about using its own modem, market reactions have been negative. Some analysts believed that the long ago new hires from the RF world signaled Apple’s intent to develop and use its own RF products. RF is a very difficult product; one Apple would take on huge risk in developing its own. It makes no sense. What makes sense is that Apple will develop a product strategy and companies like Qorvo or Skyworks in parallel will develop the products.

Regarding next year, Qorvo expects revenue increases with China-based automotive including V2X FEMs and Ultra-Wideband portfolios. We aren’t certain of the level of revenue increases from this addition.

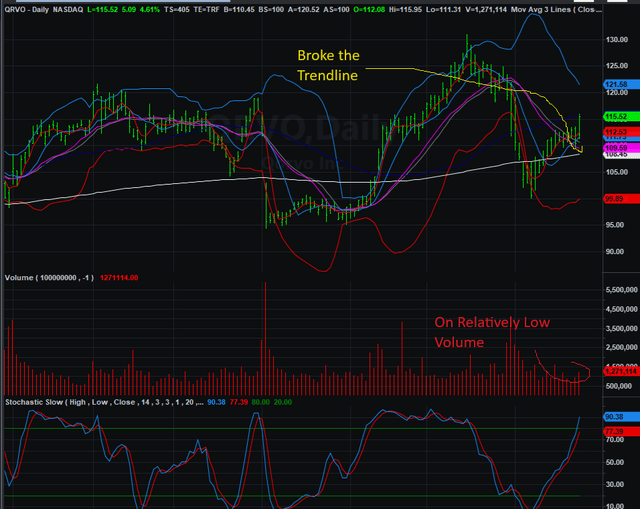

Chart

Next. a chart generated from TradeStation helps investors understand possible prices.

TradeStation Securities

From the chart, Qorvo seems stuck trading between $100 – $125 for now. We don’t know of anything that would change this at least through the next earnings. We are carefully watching the price action. The break of the 18 SMA, the magenta line, puts an upward pattern back in place.

Risks

One major risk is a recession with the latest jobs report pointing square at one with a level of sting. If the market senses this, it will tank taking in general all stocks with it. Another risk might occur if China decides to capture Taiwan. We can’t imagine this positive. But clearly, in our view, management gave very conservative guidance. Either September will be stronger or December much stronger, or both. We expect a price bump with the early November reported September quarter. At this point, we have short $115 January calls plus several $120 and $125 short November calls. We plan on moving up the November expiring strike price toward $130 sometimes in October. We expect to lose the stock associated with the $115 calls.

One last interesting tid-bite of positive news was found in this recent release. From Seeking Alpha,

‘”Morgan Stanley noted that Apple’s (NASDAQ:AAPL) iPhone 15 builds were stronger than expected in July, and that momentum seems to be building into the iPhone 16 launch.

And this,

“The 54M iPhone builds represents an all-time September quarter build record (4M units higher than the previous record) and would imply September quarter iPhone shipments of 55M units (+10%year-over-year), 5% above Morgan Stanley’s current Sept quarter shipment forecast (of 52.5M units) . . . “

Keeping this in context, Counterpoint estimates a normal September unit sale at slightly less than 50 million. We believe that Qorvo’s management had not included this late quarter surge into its guidance. For Qorvo, this is worth nearly $50 – $75 million in additional revenue.

In-spite of risks, Qorvo, in our view, remains a buy in particular at its relative cheap price in context with the chart. It is also highly likely to beat by a large margin the September guidance. This is a long-term, decades long, incremental growth story. Picking reasonable prices in which to buy and add will come along. We upgrade to a buy rating, but patience is still in order. The recent Fed announcement burst will die off likely offering lower entry points. Also of note, at times our rating toggles between buy and hold with stock price being the driver. There is no need to continue head scratching, problem solved.

Read the full article here

")

")

")