")

")

TSLA stock: Q2 earnings scheduled on July 23

I last wrote on Tesla, Inc. (NASDAQ:TSLA) with a HOLD thesis more than a month ago (on June 12, 2024, to be exact). That article, entitled “Tesla: Inventory Does Not Lie“, cautioned investors about the inventory buildup. Quote:

I see a mixed picture facing TSLA stock and thus rate it as a HOLD under current conditions. To reiterate, TSLA is still the leader in the EV space, a sector I anticipate enjoying secular growth for years or even decades to come. However, over the next 1~2 years, I see strong growth headwinds and I see its current inventory buildup as a clear reflection of these headwinds.

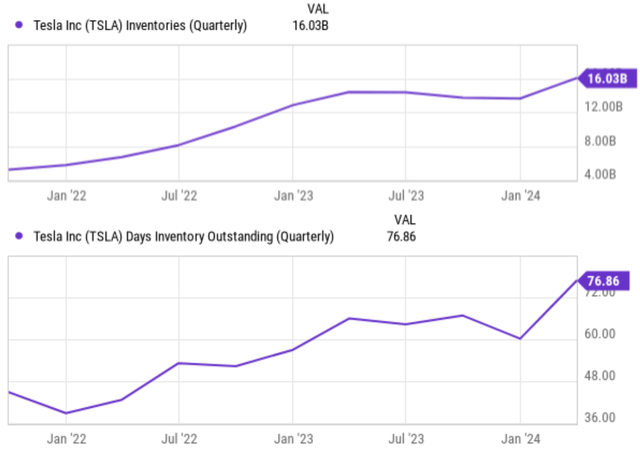

The buildup I was referring to is shown in the chart below. As seen, both in dollar amount and days of inventory outstanding, the buildup hovers near multi-year peak levels. In that article, I also expressed my skepticism regarding TSLA’s confidence in reversing inventory buildup as soon as Q2 2024 (e.g., via its CFO Vaibhav Taneja’s recent comments).

Seeking Alpha

A key new development since my last writing was Tesla’s report of its Q2 vehicle deliveries. The tally exceeded market expectations and triggered a large stock price rally (together with the robotaxi excitement). With this new development, I think an updated assessment is in order. The goal of this article is to evaluate if the new delivery data could dispel my above skepticism. My results, unfortunately, are inconclusive and thus I remain skeptical. You will see a key issue involves the uncertainties caused by TSLA’s use of lease accounting.

Given that Tesla is expected to release its Q2 2024 earnings report next week on July 23, 2024, this article also serves as a preview of its Q2 earnings. And I especially urge investors to watch out for clarifications on this topic, as elaborated on immediately below.

TSLA stock: role of lease accounting

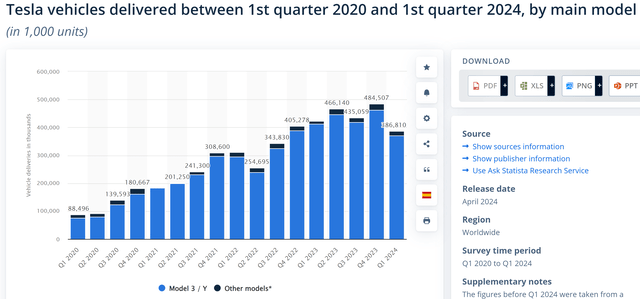

As a brief recap of its 2024 Q2 deliveries, TSLA reported a total delivery of 443,956 vehicles in the quarter. The tally is thus ahead of market estimates of 439,302 vehicles. Moreover, the company also said that it produced 410,831 vehicles during Q2, thus the delivery also exceeds the production and represents a step toward clearing its inventory buildup.

However, I remain unconvinced for a speedy growth recovery for several reasons. First, despite the consensus-beating numbers, the deliveries in Q2 still represent a decline of about ~5% YOY and are about 10% below its recent peak level reported in Q3 2023 (see the next chart below). More importantly, the delivery beat the consensus by such a narrow amount (of only 1%) and thus it is difficult for me to judge if this is a meaningful signal or just random fluctuations within the margin of error. The evaluation is further clouded by TSLA’s use of lease accounting. For Q2, TSLA reported that 2% of the deliveries total was subject to operating lease accounting, in contrast to the 1% margin it beats consensus.

Statistica

Most readers probably never paid too much attention to operating lease accounting – for good reasons. It is not essentially important for most companies anyway. And for companies that lease accounting does play a substantial role, the numbers are often reported in a way that is lumped together with other items and thus cloud assessment. With all these backgrounds, my point is that TSLA is such a case. It is difficult (at least for me) to accurately assess the impact of lease accounting on its financials.

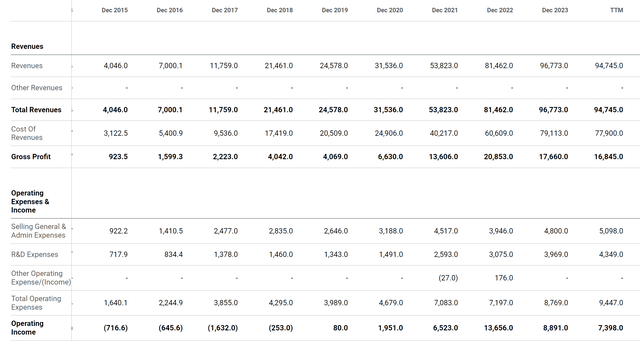

Operating lease accounting requires companies to recognize lease payments as expenses over the lease term. Lease payments are treated as an operating expense, impacting the operating income but are not itemized as you can see from TSLA’s income statement below. Thus, it is difficult to delineate the impact of lease accounting here. However, the issue is significant in my mind for at least two reasons. First, as just mentioned, TSLA’s reported impact of operating lease accounting is massive (relative to the margin over consensus). Secondly, TSLA offers a resale value guarantee program for some of its vehicles. This way, TSLA essentially acts as a lessee, even though the vehicle is already sold to the customer.

The lease expenses related to these vehicles were lumped together with other expenses in its income statement, thus complicating the analysis of its true financial performance. But overall, the results do not paint an encouraging picture for me. For example, its gross profit has been in sharp decline in the recent 2 years, dropping from $20.8B in 2022 to the current level of $16.8B on a TTM basis. Meanwhile, total operating expenses increased substantially from $7.2B to $9.5B over the same period. If you have additional information that can help to delineate the role of its lease expenses in this increase, please let me know, and thanks in advance!

Seeking Alpha

Other risks and final thoughts

Tesla also uses some capital leases (as illustrated by its balance sheet below), but I suppose the operating leases are the main issue here due to the relatively short-term nature and high residual value of vehicles. Although note that:

- The capital leases are sizable. Many analyses quote TSLA’s low debt level as a strength (with which I, of course, agree). However, the argument is partial, as the capital leases exceed the debt.

- Its capital leases have also been growing substantially recently, as seen.

Seeking Alpha

Another downside risk involves the high valuation multiples. Due to the recent stock price rebound, TSLA is now trading at over 100x of its FWD EPS, as seen in the chart below. Even accepting the growth projection assumed by consensus, the stock would be still trading at about 45x of its EPS 4 years later.

Seeking Alpha

In terms of upside risks, first I need to reiterate the limitations of the analysis of its lease expenses and obligations. Even after piecing together information from various sources, my assessment presented above is based on educated guesses at best. As mentioned in my earlier article, I am optimistic about the company’s long-term prospects. Tesla continues to aggressively invest in production capacity, its charger network, and new products. The excitement surrounding its next-generation platform is well deserved. The secular shift towards EVs, the ramp-up of its CyberTruck production, and its leading autonomous driving technology (its driver-assistance system was tentatively approved in China) all provide highly nonlinear growth opportunities in the years to come.

All told, this article is more focused on the near term. To recap, I am seeing mixed signals (or lack of definitive signal) in the near term and thus maintain my HOLD rating for Tesla, Inc. stock. A key development since my last writing was its Q2 vehicle delivery report. However, as argued in this article, the new delivery data did not dispel concern over its inventory buildup, elevating operating expenses, and margin headwinds. These are the issues that I will pay special attention to in its upcoming Q2 earning report.

Read the full article here

")