(RSKD)")

")

Today, here at the Lab, we are revisiting our commentary on Teleperformance (OTCPK:TLPFF) (OTCPK:TLPFY), a company that stands as the undisputed market leader in outsourced customer experience. For our new readers, Teleperformance, established in 1978, operates through two main divisions: Core Services (comprising contact centers in EMEA, APAC, and Americas) and Specialized Services. The group has been steadily diversifying its operations across regions and sectors.

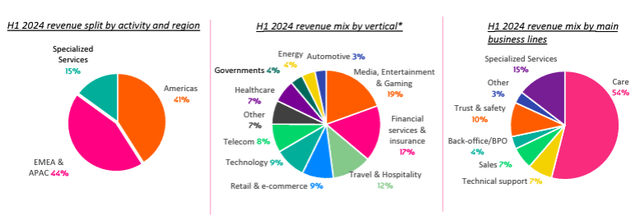

Teleperformance H1 sales split

Fig 1

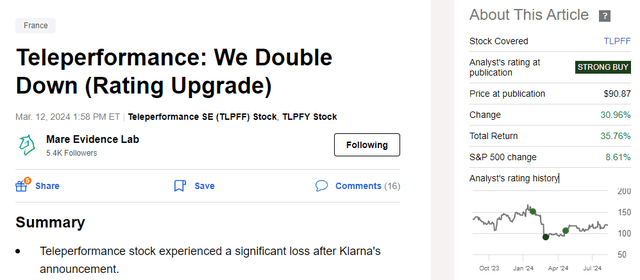

In February-end, the company’s stock price performance was heavily impacted by the Klarna AI assistant release. We increased our position with a double-down and a strong buy rating upgrade recommendation (Fig 2). This was supported by an upside integration on the latest acquisition (Majorel) and a positive view on GenAI continuing to leverage the company’s expertise, prevent churn, and boost profitability. In addition, Teleperformance has solid fundamentals, and as downside protection, we reported an attractive capital return investment story backed by a dividend and an ongoing buyback.

Mare Ev. Lab Rating Update

Fig 2

Teleperformance Earnings Release And Our Upside

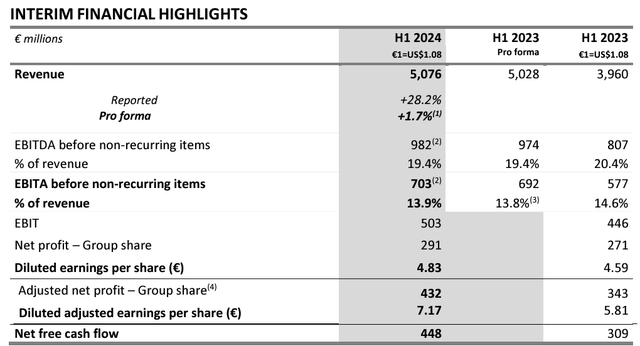

The company reported its Q2 performance in July-end. Very briefly, Teleperformance delivered an H1 top-line sales of €5.07 billion, with a plus 1.7% growth (Fig 3). That said, Q2 sales sequentially increased with a reported growth of +2.4%. This result was comfortably ahead of the Wall Street consensus estimate by +1.5%. With a margin increase of 10 basis points, the adjusted EBITA (before special items) broadly aligned with market expectations. On the FCF basis, the company reported solid operating cash flow. In detail, Teleperformance reached free cash flow at €473 million (including the Majorel cost synergies from integration), and the company reached clean results of €448 million. Considering the buyback and the dividend, the company was able to deleverage with net debt down from €4.6 to €4.5 billion.

Teleperformance H1 Financials in a Snap

Fig 3

Aside from a sound financial performance, looking back to our initiation of coverage upside, we report the following:

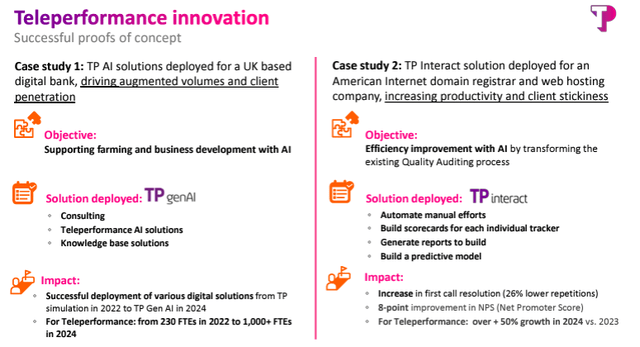

- On the AI, the company reported “more than 300 projects underway to improve the clients’ competitiveness.” We report a crucial partnership with Kore.ai to transform customer engagement solutions. This followed Microsoft’s collaboration to create a platform to make B2B companies more efficient. In early July, Teleperformance was awarded for the best AI-driven tech innovation. Here at the Lab, we have always supported the favorable tailwind of AI. In addition, as recently reported by Klarna, we see AI development as supportive of increasing sales generation and also lowering the cost basis. Klarna reported that its AI assistant reduced “the average resolution time from 11 minutes to just two”. For this reason, the company was able to reduce its workforce. This is still not the time for Teleperformance, but we believe it might be an earnings growth power ahead. In the Q2 slide, the company reported two real case studies to show its AI franchise development with the impacts of the results (Fig 4).

- The company continues to view Majorel integration as smooth. Teleperformance confirmed its run-rate cost synergies for €100 million and €150 million in 2024 and 2025, respectively. Here at the Lab, we should report that the company’s synergy generation costs are accounted for by the group holding EBITA, which was notably down on a yearly comparison. This includes the impact of Majorel IT integration systems. For this reason, we anticipate a cost improvement in H2. Looking at the combined numbers, the company reported a growth of 28.2% in H1, with a positive take in the margins. This cannot go unnoticed.

Teleperformance AI upside

Fig 4

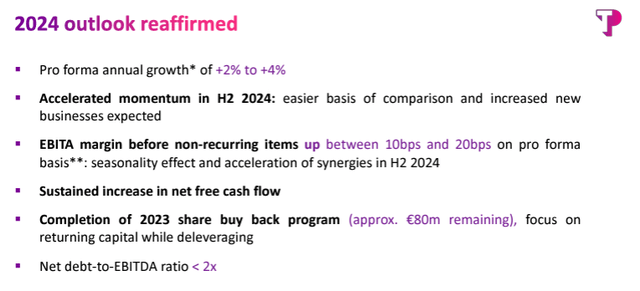

On a new upside, in Q2, there was a notable sales sequential acceleration. This was due to the performance of Specialized Services, which grew organically above 10% year-on-year. This was supported by new tech/retail clients and a ramp-up in the financials & autos segment. Q2 marks the second quarter in which the company has beat expectations. In addition, Teleperformance reiterated its 2024 outlook (Fig 5). We believe it is gaining traction in reassuring its investor base after the downgrades through the 2023 Fiscal Year. On the margin side, the company expects an acceleration over the H2, with a confirmation of +10-20 basis points EBITA growth.

Teleperformance 2024 Outlook

Fig 5

Valuation

Considering a supportive H1, we left our sales forecast of €10.3 billion unchanged. Indeed, going down to the P&L assumption and assuming higher costs at the Group holding due to Majorel integration costs, we lower our EBITA projection to 14.9%. Since synergies are expected to bear fruit in H2, we decided to await visibility on moving parts. That said, given the company’s FCF to EBITDA, we see support for an additional €350/400 million in deleverage. This includes the fact that the company has already paid its annual dividend and has a minimum buyback left. Teleperformance shows no changes in the technical guidance. For this reason, we arrived at an adj. net income projection of €950 million with an EPS of €12.8.

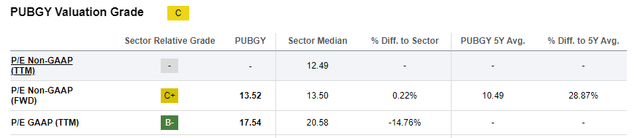

Even considering higher synergy generation costs linked to the Majorel acquisition, we still believe Teleperformance’s valuation is attractive. In our estimates, for consistency reasons, we confirm our 13x P/E target. With our numbers, our valuation is set at €166 per share. This is well-supported by peers analysis such as Publicis Groupe SA, which trades at a forward P/E of 13.52x (Fig 6), and by looking at the Business Support Services sector, with a P/E of 14.53x. Teleperformance is the global leader in CX, and we are not applying any synergies to Majorel’s acquisition.

SA Valuation data

Fig 6

Risks

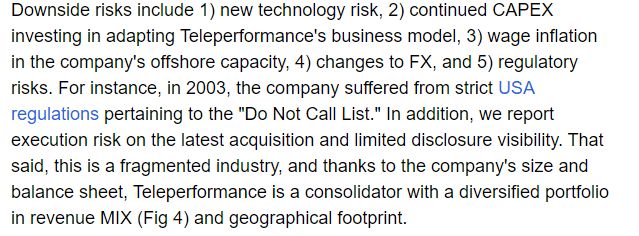

Teleperformance risks are included in our previous coverage (Fig 7). In addition, we report the following: 1) the company needs to continue adapting and investing in its business model, and generative AI could potentially disrupt pricing and competitive dynamics, and 2) a challenging pricing environment. In the Q4 risk section, we also reported Investor Relations risks related to AI communication development. Looking at the corporate website, we believe Teleperformance has significantly improved its disclosure.

Mare Ev. Lab previous risk section

Fig 7

Conclusion

Following the H1 results, we are reassured of the AI upside as well as in Teleperformance natural consolidator within the CX industry. There is a valuation discount to grab while awaiting a critical acquisition development to play.

Editor’s Note: This article discusses one or more securities that do not trade on a major U.S. exchange. Please be aware of the risks associated with these stocks.

Read the full article here

(RSKD)")