")

")

Since I upgraded shares of Superior Group of Companies (NASDAQ:SGC) in the middle of March, the company has done well to generate upside for investors. Shares are actually up 12.3% compared to the 9.3% increase seen by the S&P 500. I would consider that a win in my book. Of course, this does come after a painful experience. You see, prior to earlier this year, I was neutral on the stock. From the time that I wrote my ‘hold’ assessment of the firm in January 2023 until I upgraded the stock, shares were up 63.4%. That was roughly double the 31.7% increase seen by the S&P 500 over the same timeframe.

Attractive growth, combined with certain valuation metrics, ultimately led me to change my tune on the producer of uniforms, corporate identity apparel, career apparel, and accessories. Of course, upside cannot last forever. But based on the most recent data provided by management, I would argue that it’s not time to downgrade the stock just yet. Management anticipates further growth, both on the top and bottom lines. And while shares might not be the cheapest compared to similar enterprises, they are cheap enough to warrant a good degree of optimism.

Still a good fit

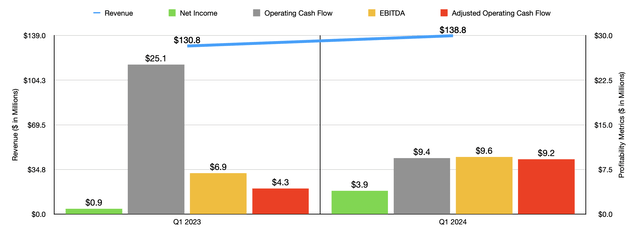

At its core, Superior Group of Companies is a company that focuses on uniforms, as well as similar products. But when you look under the hood, you see that the company is a bit more complex than that. But before we get there, we should touch on overall financial performance in the most recent quarter for which data is available. This is the first quarter of the 2024 fiscal year. During that time, revenue for the company came in at $138.8 million. That’s 6.1% above the $130.8 million reported one year earlier. Most of this sales increase came from the company’s Branded Products segment, which focuses on the sale of the company’s general branded uniform products. Revenue of $87.1 million beat out the $81.9 million reported one year earlier. Management attributed this mostly to an increase in sales volume. However, they did also acknowledge that higher pricing contributed to this upside as well.

Author – SEC EDGAR Data

Another major part of the company is its Healthcare Apparel segment. As you can guess, this is the part of the company that sells uniforms and similar products specifically to the healthcare industry. Examples include scrubs, lab coats, protective apparel, patient gowns, and more. Revenue growth here was much slower, at 3.8%, with sales inching up from $28.2 million to $29.2 million. Higher online sales volume was the primary contributor to this increase.

Even though the company focuses largely on uniforms and related products, it does also have another segment by the name of Contact Centers. With facilities in places like El Salvador, Belize, Jamaica, the Dominican Republic, and even the US, the company provides outsourced and near shore business process services for its clients. In essence, this would be most easily described as a call center support services firm. Thanks to attractive growth in demand for its services from existing customers, overall revenue managed to rise by 6.8% from $22.1 million to $23.6 million.

On the bottom line, Superior Group of Companies did not fail to impress either. Net income jumped from $0.9 million to $3.9 million. Operating cash flow did admittedly fall from $25.1 million to $9.4 million. But if we adjust for changes in working capital, we would get an increase from $4.3 million to $9.2 million. Lastly, EBITDA for the company rose from $6.9 million to $9.6 million. It is worth mentioning that all three of the company’s operating segments saw EBITDA expand year over year. The largest improvement came from the Branded Products segment, with a rise from $7.5 million to $9.9 million.

When it comes to the 2024 fiscal year in its entirety, management anticipates some impressive results. Overall revenue for the year is expected to be between $563 million and $570 million. At the midpoint, that would be 4.3% above the $543.3 million reported for 2023. This actually represents an increase in guidance from a prior range of between $558 million and $568 million. So it does appear as though things are getting better as opposed to worse. On the bottom line, management also increased guidance. Previously, it was expected that earnings per share would be between $0.61 and $0.68. That range has now been pushed up to between $0.73 and $0.79 on a per share basis. At the midpoint, that would imply net income of $12.5 million. That’s comfortably above the $8.8 million reported for 2023.

Author – SEC EDGAR Data

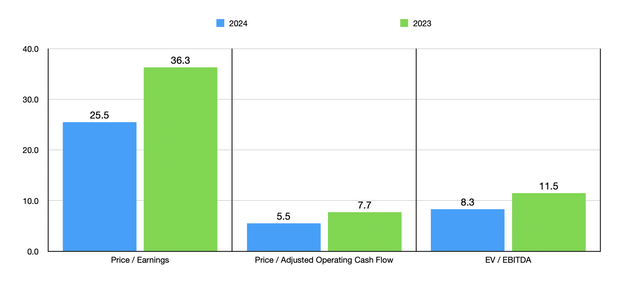

If we assume that other profitability metrics will grow at a rate that is similar to what was seen in the first quarter of this year compared to the same time last year, this would translate to adjusted operating cash flow of $88.6 million and EBITDA of $46.6 million. To be perfectly honest with you, the adjusted operating cash flow figure looks disproportionately large. So if we instead assume that it will grow at the same rate as EBITDA is expected to, we would get a more modest reading of $57.6 million. With these results, you can see how shares of the company are valued in the chart above. Relative to earnings, I would argue that shares are quite pricey. But when it comes to the other profitability metrics, they look fairly attractive. This is especially true on a forward basis. In the table below, I then compared the company to five similar firms. On a price to earnings basis, three of the five companies ended up being cheaper than Superior Group of Companies. This number drops to two of the five when using the EV to EBITDA approach. But on a price to operating cash flow basis, our candidate ended up being the cheapest of the group.

| Company | Price / Earnings | Price / Operating Cash Flow | EV / EBITDA |

| Superior Group of Companies | 36.3 | 7.7 | 11.5 |

| Lakeland Industries (LAKE) | 29.7 | 22.4 | 12.4 |

| FIGS (FIGS) | 47.4 | 8.2 | 18.4 |

| Aramark (ARMK) | 13.6 | 13.7 | 7.9 |

| Cintas Corp (CTAS) | 49.4 | 38.1 | 30.7 |

| UniFirst Corp (UNF) | 24.2 | 11.7 | 9.7 |

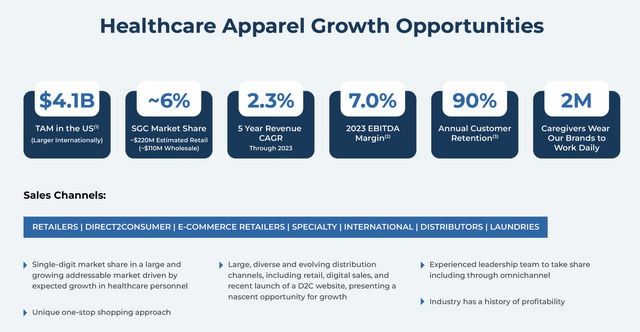

While these markets might seem small, management does have plenty of growth potential. When focused just on the US healthcare apparel space alone, management estimates the market to be worth about $4.1 billion. Naturally, the global space would be significantly larger. But with two million caregivers wearing the company’s brands daily, the firm boasts a market share of only 6%. This leaves plenty of upside potential as time goes on.

Superior Group of Companies

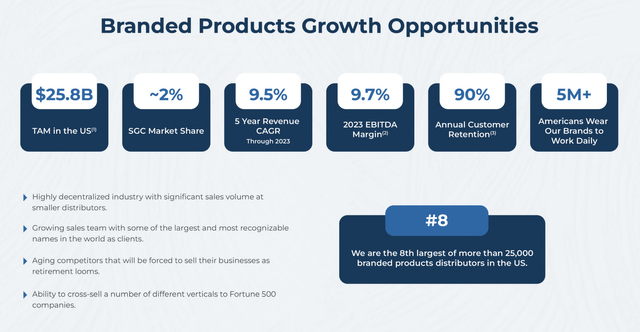

When looking at the Branded Products space that focuses on general work uniforms and the like, the market opportunity for the US alone is much larger at $25.8 billion. This gives the company a market share of only about 2%. In fact, it’s only the 8th largest player in this industry. But the good news about this is that, with over 25,000 distributors in this space in the US, it’s clear that the industry is heavily fragmented. This opens up the door for growth by means of acquisition. And as the company becomes larger, it should ideally achieve greater economies of scale that should allow it to compete better against those firms that it does not acquire.

Superior Group of Companies

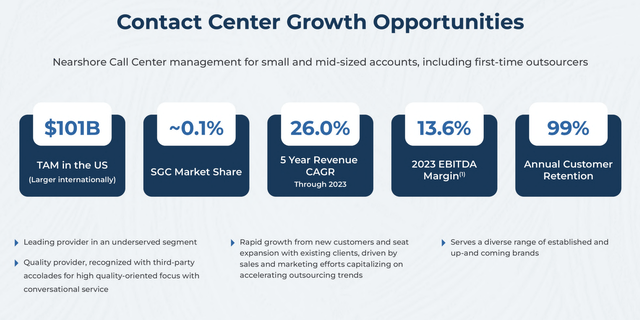

While the primary focus of Superior Group of Companies has historically been on work uniforms and the like, perhaps its greatest potential comes from the Contact Centers industry. Already, the company has established operations spread across parts of the Americas. But with this industry, focused on the US alone, worth around $101 billion, the company has only 0.1% of the space under its control. It’s clear that the firm has also been focused on growing this share of the pie. In the five years ending in 2023, the firm achieved annualized revenue growth of about 26%. And with annual customer retention rates of about 99%, the firm seems to be doing a fine job.

Superior Group of Companies

Takeaway

Operationally speaking, Superior Group of Companies is an interesting company that I believe has solid potential for future growth. Revenue continues to climb, while profits and cash flows follow suit. Relative to earnings, shares are pricey. And I wouldn’t exactly call them cheap compared to similar companies. But they are cheap on a cash flow basis. This, combined with the prospect of future growth, leads me to think that enough additional upside is warranted to keep the company rated a ‘buy’ for now.

Read the full article here

")

")

: Medical Properties Trust Stock (NYSE:MPW)")