Thesis

We have covered the SPDR Blackstone Senior Loan ETF (NYSEARCA:SRLN) more than four months ago, when we outlined for readers why we believed the exchange-traded fund to be the weakest among its peers when it came to floating rate loan construction. The name is down slightly on a price basis and up slightly on a total return basis since our piece:

Prior Rating (Seeking Alpha)

With PPI data coming in better than expected on August 13, 2024, and the market now solidly pricing three plus cuts for 2024, we are going to revisit the name. In today’s article, we are going to articulate why we believe retail investors are well served to start divesting the weakest names in the leveraged loan space, with capital being pulled out from the asset class.

Better inflation data spells Fed cuts

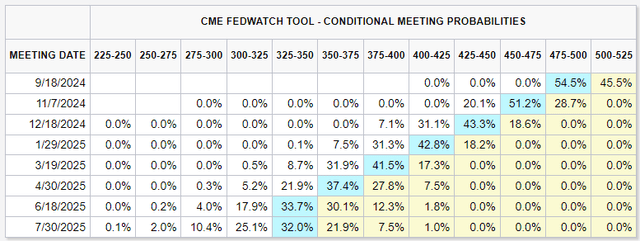

The trend in the past few months has been of better than expected inflation data, a trend which continued with the PPI figures on August 13, 2024. The hard data has prompted the market to price more than three cuts in 2024:

Meeting Probabilities (CME)

Based on the CME Fed-watch tool presented above, we can see the market pricing in at least three cuts by the end of December 2024 currently. This is a snapshot of the market as of today, and future data releases will impact the figures and probabilities.

Suffice to say that we are no longer in an environment where ‘higher for longer’ is the mantra, and while our personal opinion is that we will get two or three 25 bps Fed cuts this year, some market participants are even calling for a 50 bp cut in September.

Irrespective of what the actual figures will end up being, what is clear for investors is the down trajectory for rates going forward. We are set for an upcoming period of 18 months where risks free rates will be moving lower, an action which will result in floating rate assets yielding less.

Once SOFR resets on the new lower levels, the rate cuts will be passed one for one to investors via leveraged loans. The same way the low duration of the asset class helped insulate investors in a monetary tightening, the feature will account for immediate lower yields as Fed Funds and SOFR move lower.

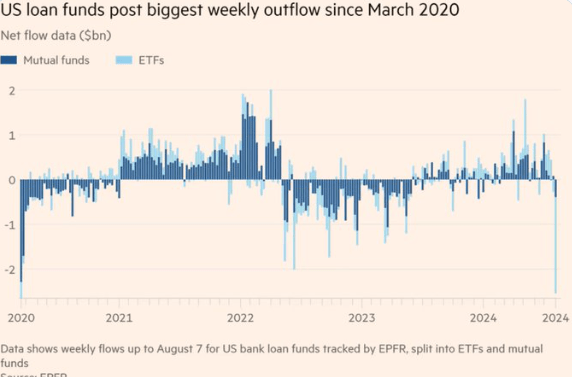

Rate cuts equal capital outflows

While there will always be investors in the leveraged loan space, lower rates have spurred a capital re-allocation from floating rate into fixed rate:

Leverage Loans Flows (FT)

Leveraged loans have proved to be very popular in the past three years due to their low duration and ability to pass on to investors a high rate of return. As Fed Funds soared to 5.25%, the leveraged loan asset class was able to pass on to investors all in yields in excess of 8%, total return which was obtained with low volatility figures.

Now that the market is pricing in a high amount of cuts with a terminal Fed Funds rates of 3.5% in late 2024, investors are moving towards buying duration, thus navigating away from funds such as SRLN.

Sell the underperformers, hold the winners

While we are not advocating selling all leveraged loan holdings, we are nonetheless of the opinion that the weakest links should be sold, since they will end up underperforming the market, a market which in itself is starting to have a down shift.

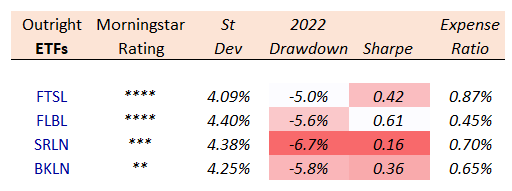

Let us reference the cohort of exchange-traded funds which are composed of floating rate loans, and look at the relevant analytics:

Leveraged Loan Cohort (Author)

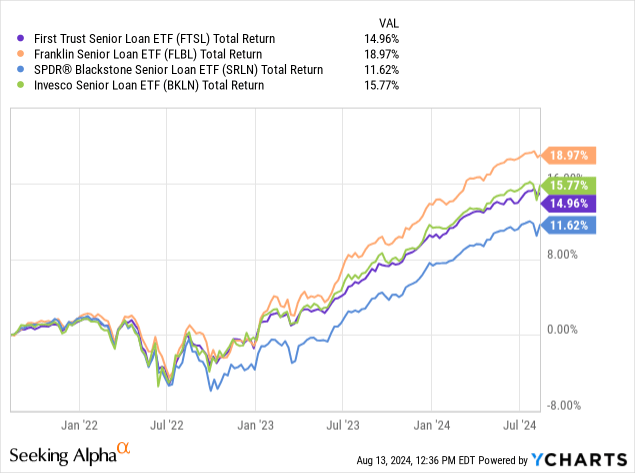

SRLN has a high standard deviation, a high 2022 drawdown and an expense ratio on the high side. In the past three years, it has been the clear underperformer by a very high margin:

When comparing the First Trust Senior Loan Fund (FTSL), the Franklin Senior Loan ETF (FLBL) and the Invesco Senior Loan ETF (BKLN) versus SRLN, we will notice that SRLN is at the bottom of the performance chart, with a constant weak return figure.

When faced with an asset class which is falling out of favor, you want to hold the best names to still have some exposure to floating loans, but at the same time sell underperformers because they will keep doing what they do best, namely be at the bottom of the performance charts.

We have written a number of articles as of late where we switched to ‘Hold’ for a number of floating rate ETFs and CEFs, but in our mind, SRLN is a clear case of outright sell in today’s market, since the downside is not compensated by the upside.

Middle of the road fund build

SRLN is a fund that predominantly holds leveraged loans:

Composition (Fund Website)

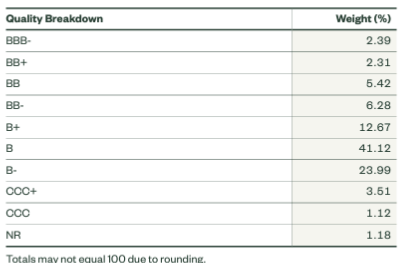

Over 96% of its portfolio is invested in loans, while only 4.3% represents bonds. The fund is focused on the lower quality floating rate loans:

Rating (Fund Website)

More than 64% of its portfolio is concentrated in the lowest tier ‘B’ and ‘B-‘ names, thus representing the riskiest portion of a regular portfolio build. We call this ‘riskiest’ of a regular build because we consider the ‘CCC’ bucket to fall squarely in the speculative space. The fund does do a good job at having a very limited amount of speculative-grade leverage loans.

Conclusion

SRLN is a leveraged loan exchange-traded fund. The vehicle represents an unleveraged take on the asset class, and has demonstrably underperformed a cohort of its peers in the past three years, with overall underwhelming analytics. As inflation data comes in better than expected, the market is pricing in excess of three rate cuts in 2024, with the first one expected in September. Given this macro outlook, capital is being pulled away from floating rate assets and allocated into fixed bonds, capital rotation, which will have a negative impact on SRLN. While we rated the fund a ‘Hold’ in our last article, we are now downgrading the name to a ‘Sell’ based on the asset class outlook and the fund analytics.

Read the full article here