")

Business Update Conference Call Transcript")

")

Invesco S&P 500 High Beta ETF (NYSEARCA:SPHB), launched on May 5, 2011 and managed by Invesco Capital Management LLC., is an ETF that tracks the performance of the S&P 500 High Beta Index.

This fund’s long-term performance hasn’t been great, despite the fact that high-beta stocks should deliver excess returns in a bull market. The idea behind high-beta tilting is solid, but only under certain circumstances, which are currently not present. Regardless, that may change in the future and this ETF can have a place in your portfolio if you understand the risks and potential drivers.

Methodology

The approach of the ETF’s index is fairly simple. It selects and then weights the top 100 stocks in the S&P 500 based on beta (the higher a constituent’s beta, the greater the weight it has in the index). As beta represents the sensitivity to market returns, the result should be the amplification of both gains and losses relative to the S&P 500.

The idea behind investing in high-beta stocks is sound for those who are trying to outperform the market, but only under some circumstances. A high beta can substitute the use of leverage as far as results are concerned, so just like using leverage can be beneficial in some instances but damaging in others, high-beta stocks can be appropriate in certain situations.

For this reason, I believe that the approach of SPHB mostly caters to traders, as long-term investors are probably better off investing through a vanilla S&P 500 ETF.

Performance & Cost

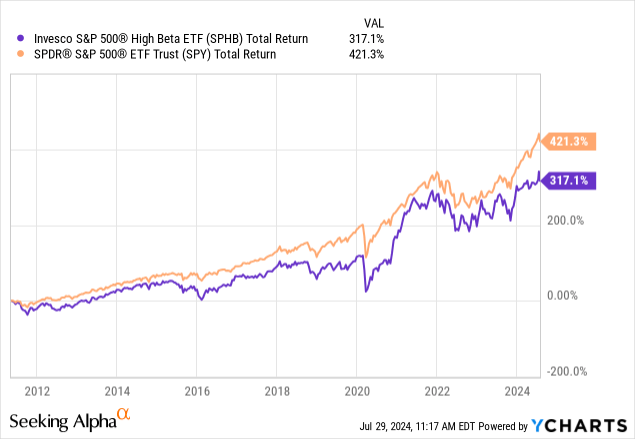

During the last 10 years, the fund’s NAV return has been 11.28% per annum, so it underperformed the SPDR S&P 500 ETF (SPY) which returned 12.72%.

The underperformance is better illustrated when you compare the total returns of each fund since SPHB’s inception date:

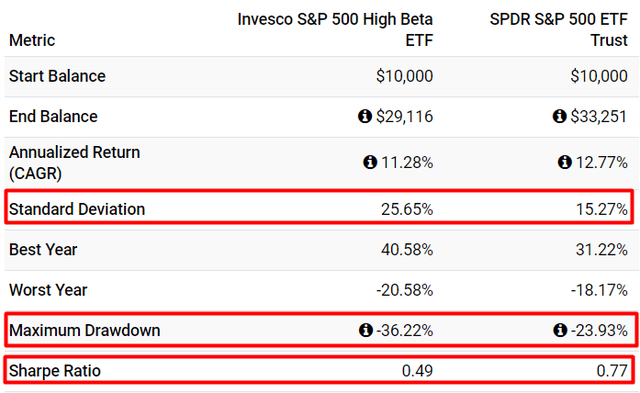

Predictably, the high-beta tilt has resulted in much higher volatility, so SPHB has underperformed on a risk-adjusted basis too:

portfoliovisualizer.com

So the reasoning that this ETF is not ideal for long-term investing is supported by evidence. Since 2011, SPY has delivered exceptional returns for passive investors and, yet, a high-beta bias would underperform. This is interesting considering the idea of the “risk-return tradeoff.”

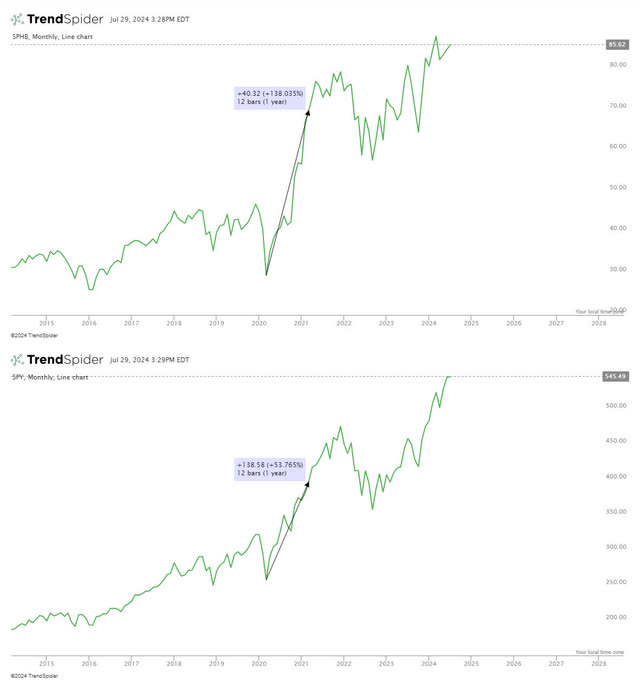

It’s also interesting to note, however, that the fund did outperform by a huge margin for a short period after the 2020 drawdown:

TrendSpider

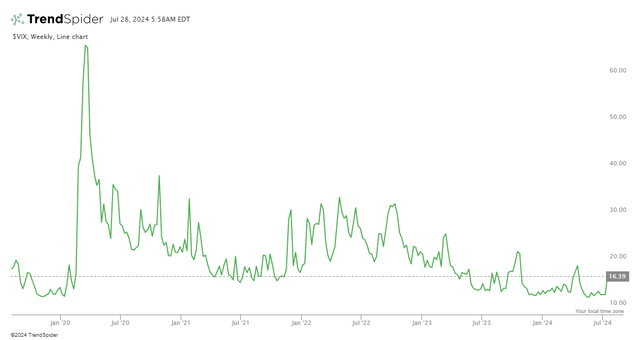

Assuming that interest rates are low, the market is in recovery mode, and there is low expected volatility, SPHB could be used to capture returns coming from increased investor confidence. The keyword here is “could” because it’d be challenging to time such a trade successfully, even if you can reasonably expect rising interest rates when inflation is high. In any case, only one of those conditions that were present back then is also present today, and that is low expected volatility:

TrendSpider

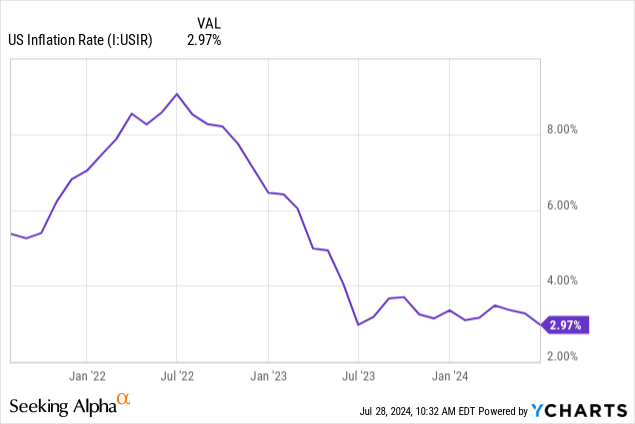

Moreover, something that wasn’t present back then but now is low inflation:

So, what’s missing are low interest rates and the beginning of a market recovery. The market hitting all-time highs also brings us to valuation. Right now, SPHB’s holdings are not much cheaper and its relatively high expense and turnover ratios don’t make a purchase attractive:

| P/E | P/B | Expense Ratio | Turnover | Daily Volume | |

| SPHB | 22.07 | 3.23 | 0.25% | 66% | 292,191 |

| SPY | 22.74 | 4.64 | 0.09% | 2% | 11,868,017 |

The threat of a recession is another shadow that is looming over this ETF. So, while some of the conditions that may have been the drivers behind that short-term outperformance before interest rates started rising are currently present, there should be a greater valuation differential as well as more promising signs that interest rates are going to fall to a more attractive level before SPHB is worthy of consideration.

Risks

I think the most important risk here is related to valuation. While there are some opportunities present today that investors shouldn’t ignore, the market is too confident today and unexpected events like the Fed keeping the policy interest rate as it is this year present a huge danger for high-beta portfolios.

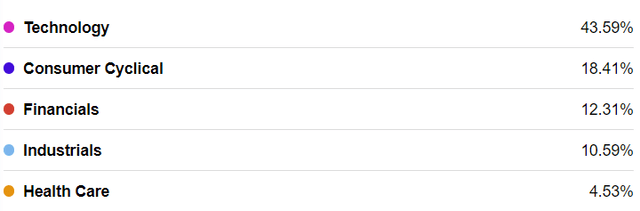

Also, because of the high-beta bias, a huge part of the portfolio is tech stocks, introducing sector concentration risk:

Seeking Alpha

Verdict

Riding the wave back to market recovery seems to be this fund’s true value to holders. Because of the absence of such a situation and the significant risks present here, I am rating SPHB a hold. However, investors should re-examine it if the market crashes as a way to capture excess returns.

What do you think? Do you own this fund or not? Let me know in the comments! Thank you for reading.

Read the full article here

")

Business Update Conference Call Transcript")