")

")

")

")

")

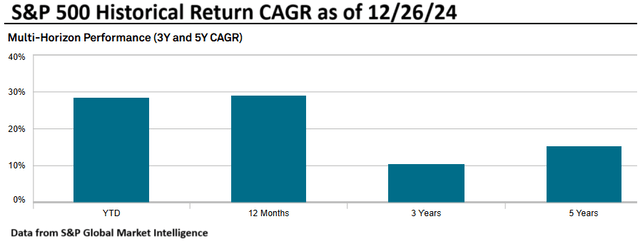

There is no doubt that S&P 500 (SPX) returns have been fantastic with investors enjoying nearly 30% gains in the last year.

S&P Global Market Intelligence

It has been a multi-year success story with a roughly 15% CAGR over the past 5 years.

Will it continue? Is it still a great place to park investment dollars?

We believe the answer is no. A substantial portion of the S&P’s recent gains have come from multiple expansion and valuation is flashing some serious warning signs.

This article will examine valuation from a variety of angles in an attempt to hone in on forward expected returns. Let us begin with the broad view and then get into the numbers.

Broad view of S&P 500

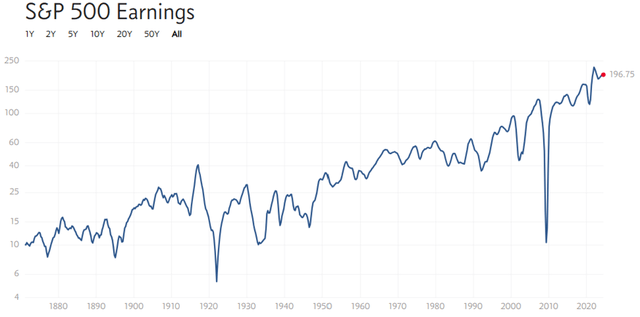

The S&P 500 is roughly a reflection of the U.S. economy. Over very long periods of time, the U.S. has had the best economy in the world and that is reflected in robust earnings growth for the S&P 500.

Multpl.com – earnings go through June of 2024

Consensus estimates call for fundamental growth to continue in 2025 and beyond. I largely agree as the U.S. economy appears to be generally growing nicely.

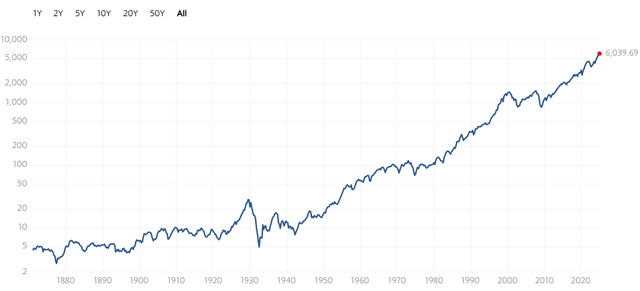

The problem from an investment standpoint, however, is that price gains have dramatically outpaced earnings growth. Below is the price of the S&P 500 over the same time period as the earnings above.

Multpl.com – earnings go through June of 2024

It might be hard to tell because the Y axis of both graphs is logarithmic, but the slope of the price graph is much steeper than the slope of the earnings graph.

Since 1872, S&P 500 earnings increased by 20.2X, but over that same time period, market price increased 1241.7X.

An interesting factoid, but perhaps wonky because of the nascent market back in 1872.

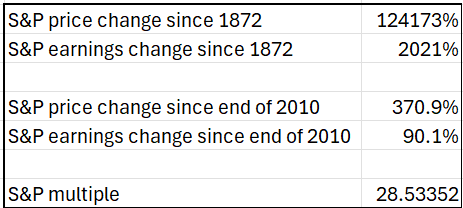

Let us instead look at a more modern and normal time in the market starting in January of 2011.

S&P trailing earnings were 111.34 and the S&P 500 was priced at 1,282. Current estimates for 2024 earnings are 211.67 and the S&P is priced at 6,039 as of the close of December 26th, 2024.

So while earnings are up about 90%, the price has soared 371%.

Data from Multpl.com and FactSet as of 12/24/24. Calculations by 2MC

That takes the trailing multiple to a whopping 28.5X

Historically, the S&P 500 has traded at a median multiple of 15.04X (source Multpl – Market, financial, and economic data).

That is quite a high valuation and most analysts would agree that the S&P valuation is high at the moment.

Opinions diverge as to whether that is too high. We believe it is too high and that forward returns will suffer as a result.

Cyclically adjusted analysis

Earnings are strong and earnings growth projections for 2025 are strong which some suggest justifies the high multiple. FactSet consensus is calling for 14.8% growth in 2025 and 28.5X earnings would be a reasonable valuation if we were to extrapolate that growth rate well into the future.

Given pricing, it seems that is what the market is doing.

However, the S&P, like the economy, is quite cyclical. It has times of excellent growth and times of negative growth, so I find it a bit aggressive to straight line the good times.

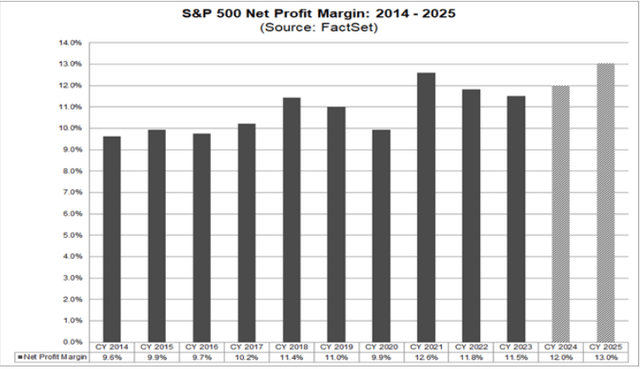

In fact, one could argue the S&P is currently over-earning its potential. Net profit margin is expected to be 12% in 2024 and 13% in 2025.

FactSet

These numbers are well above historical norms and could be subject to mean reversion.

Net profit margin tends to track toward mid-to-high single digits due to free market forces.

- When margins are too low, companies will disband allowing the remaining companies to gain market share and increase margins

- When margins are too high, new companies will be incentivized to enter which increases competition and lowers margins.

A forecast that margins will remain unusually high in perpetuity suggests something has profoundly changed about equilibrating market forces. There have been substantial productivity gains which may be the source of higher margins, but without equilibrium breaking mechanisms, I see no reason it would not just filter through to lower prices. I have not seen a compelling argument for permanently high margins and believe they will still be subject to mean reversion as they have been in the past.

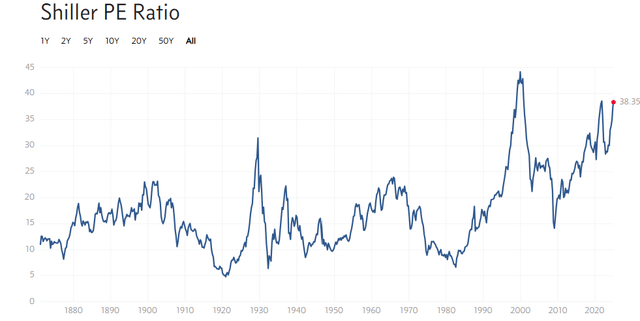

Due to cyclicality and the mean reversion of margins, I believe Robert Shiller was on the right path with viewing valuation from a cyclically adjusted standpoint. Shiller created the CAPE ratio or Cyclically Adjusted Price to Earnings ratio which averages earnings over the preceding 10 years. The Shiller P/E also adjusts for inflation, which is particularly relevant today given the recent bout.

On this metric, the S&P’s valuation is extraordinarily high.

Multpl.com

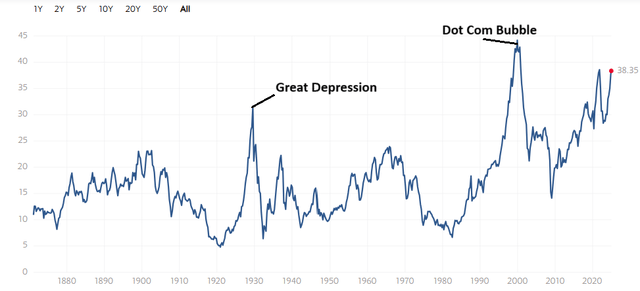

With a Shiller P/E of 38.35X, the S&P has only been higher once, and approached this level at a peak back in 1929. Thus, today’s valuation is most similar to the dot com bubble or right before the Great Depression.

Multpl.com as of 12/24/24 annotations added

Either of these would have been terrible times to invest in the S&P 500.

In the following section we will explore how valuation impacts forward expected returns.

Shiller P/E as an indicator of forward return

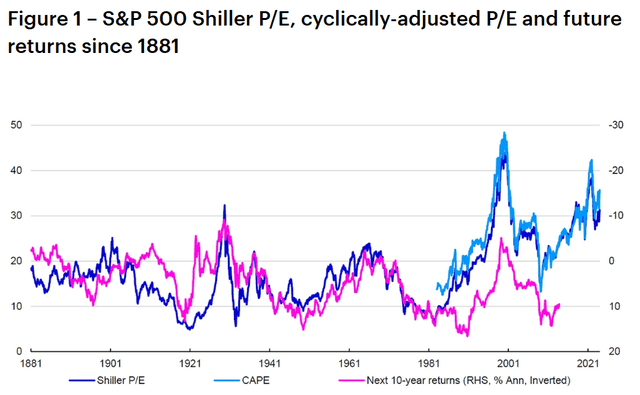

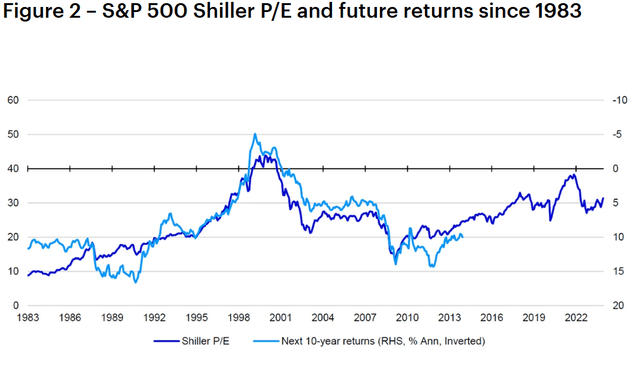

Invesco put out a great research piece on the predictive power of the Shiller P/E. In it they chart forward returns against the Shiller P/E of the S&P 500.

Invesco

Just as we discussed before, the market has changed since its nascency, so Invesco redid the graph for more modern times (since 1983).

Invesco

Source: Invesco

In each graph, the right axis is inverted so as to show how strong the correlation between Shiller P/E and forward returns is.

Noting that it is inverted, we should conclude that it is a negative correlation.

In other words, the higher the Shiller P/E is at any given time, the lower the forward returns of the S&P 500. Since this is historical data on forward 10 year return, the light blue line, of course, ends 10 years ago.

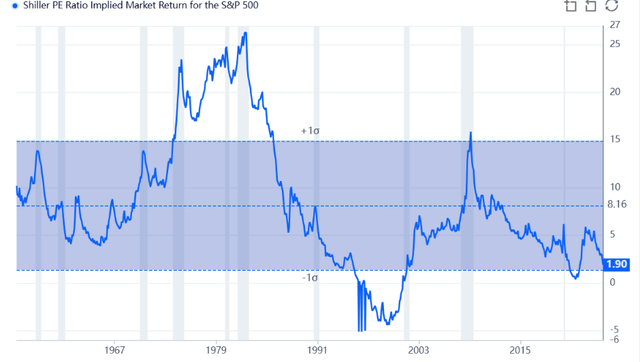

GuruFocus used this and other data to estimate forward returns based on Shiller P/E going up to the present (or rather November 2024 when their graph was made).

GuruFocus

The latest datapoint on the chart above is November 1st, 2024, which corresponds to an implied forward return of 1.9%.

This is of course hypothetical and is merely the implication if the historical trends of Shiller P/E hold true. As such, I would take this not as a hard datapoint of 1.9% but rather as a ballpark figure.

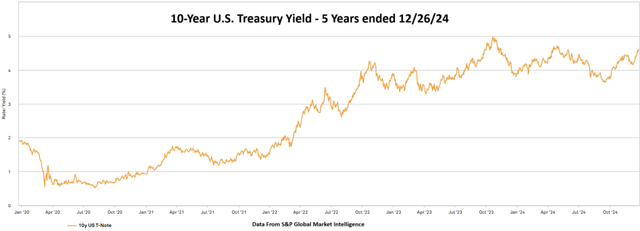

The logic checks out. With the earnings multiple being so high, cashflows are really low relative to each dollar invested. I find the extremely high valuation of the S&P to be particularly puzzling given the surge in 10-year treasury yields.

S&P Global Market Intelligence as of 12/24/24

Overall take

While S&P earnings have been strong, price gains have far eclipsed earnings growth such that valuation has become extremely high. From these lofty levels we expect forward performance of the S&P to be substantially lower, likely in the low single digits on average for the next 10 years.

Note that when valuations were extreme around 2000, the forward 10-year return of the S&P was approximately 0%. It is now known as the Lost Decade. Valuations are not quite that extreme today, so we think low single digits (maybe 3%-5% CAGR) is the more likely outcome.

Editor’s Note: This article covers one or more microcap stocks. Please be aware of the risks associated with these stocks.

Read the full article here

")

")

")

")

")