")

")

SoundHound AI, Inc. (NASDAQ:SOUN) has risen again, but not as high as the recent AI hype highs. The AI voice company has a promising future, but the business just doesn’t ever scale fast enough in the dynamic AI market. My investment thesis is Neutral on the stock around $5 with another deal likely to boost revenues, but not help with the key organic growth.

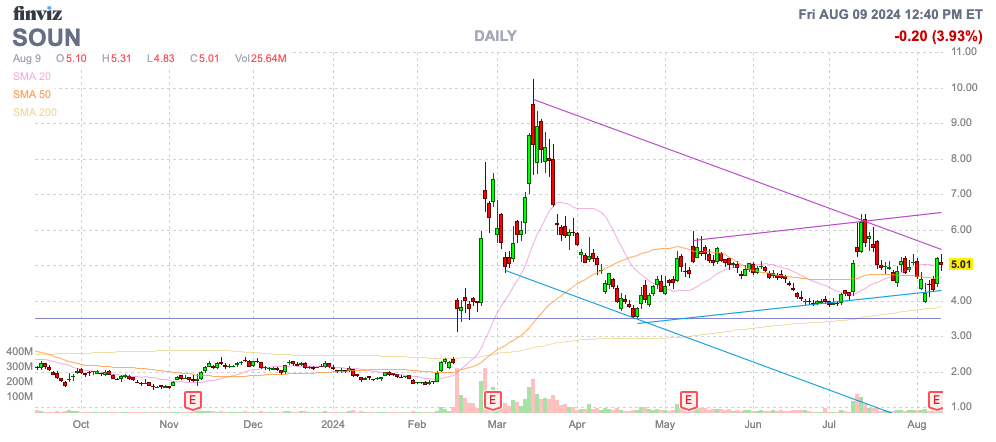

Source: Finviz

Unimpressive Results

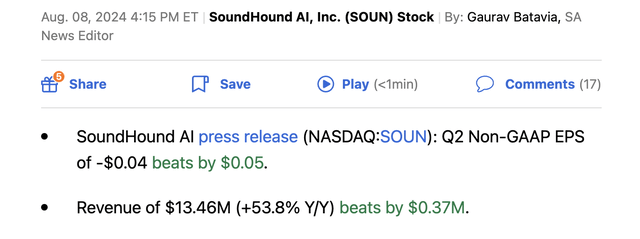

SoundHound AI reported solid growth for Q2’24, but the company trades based on the hype surrounding automotive and restaurant AI voice deals that never really flow into quarterly results. The company reported the following numbers:

Source: Seeking Alpha

AI hype has been around for nearly two years now, and SoundHound AI reported another quarter with minimal revenues. Besides, a decent part of the growth is attributed to acquisitions in a period when companies like OpenAI and such have grown to $1 billion in annual revenue overnight.

SYNQ3 and Allset have both been acquired since December to boost AI voice ordering capabilities. Neither company was included in the majority of 2023 financials.

SoundHound AI reported an adjusted EBITDA loss of $13.8 million. The company is reasonably operating in a manner to approach breakeven in the 2H when revenues were already set to accelerate towards the $20-$25 million range.

SoundHound AI now lists a $723 million cumulative subscriptions and bookings backlog, up from $682 million in the prior quarter.

Another Deal

While analyzing the Q2 results are important, the real story is the deal to acquire Amelia. The deal brings a legacy business in enterprise AI across key verticals of finance, insurance, retail and healthcare, though the press release hints at customer service contracts.

Amelia is expected to be accretive in the second half of 2025 and management suggests the business has lower margins and slower growth rates. SoundHound AI would already seem to be heavily focused on a 100,000 restaurant pipeline or AI voice ordering, so the integration of another business would be distracting from an already big opportunity.

The deal value immediately sets off some alarm bells as well. SoundHound AI is only paying $80 million in cash and equity for a company listed as generating over $45 million in recurring AI software revenue next year, plus other non-software revenues.

In essence, SoundHound AI isn’t even paying 2x 2025 sales in cash and equity for the business. SoundHound AI currently trades at nearly 17x the prior estimates for 2025 revenues of $103 million.

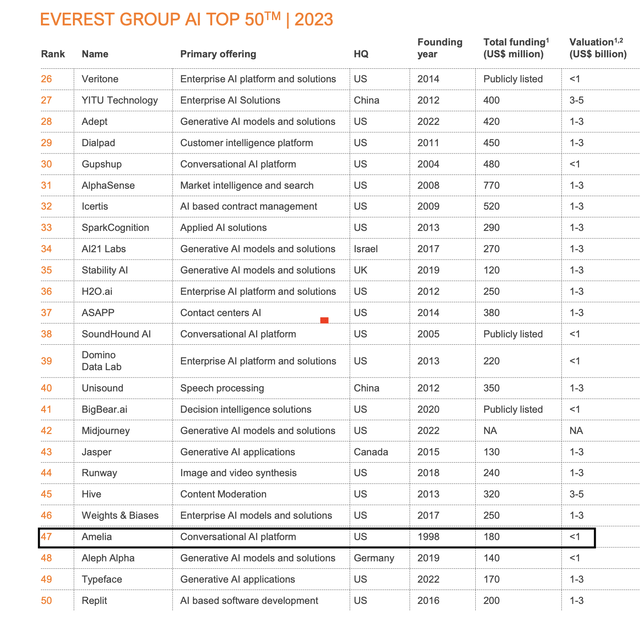

The deal valuation is even more perplexing, with Amelia listed in the Top 50 AI software companies. The list includes the well known generative AI firms like OpenAI and Anthropic topping the list, with Amelia at #47 and SoundHound AI at #38.

Source: Everest Group

The other firms have valuations in the billions, similar to SoundHound AI. Even BigBear.ai (BBAI) listed at #41 has a publicly listed valuation of $300 million.

The financial details of the transaction change the valuation a lot. SoundHound AI is paying $10 million in cash and ~$70 million in stock via issuing 13.1 million shares at a price of $5.35.

The catch is that the company assumed $110 million in debt, having already paid off $70 million. Also, the owners of Amelia can earn 16.8 million in earnest shares starting with software revenue topping $55 million in 2025. These additional shares could increase the purchase value by up to $90 million.

SoundHound AI updated financial targets based on this deal, with full year 2024 revenue now to exceed $80 million and its 2025 revenue outlook to exceed $150 million. The details suggest maybe Amelia isn’t growing very fast.

The consensus estimates had SoundHound AI producing $70 million in 2024 revenues, becoming $103 million next year. The Amelia revenue of $45+ million next year fits with the new $150 million target for 2025, though the numbers suggest SoundHound AI hasn’t hiked their estimates despite supposedly booming demand for automotive and restaurant voice AI, including dynamic ordering at restaurants.

The revenue forecast for 2024 jumps to $80 million, suggesting somewhere around $10 million from the Amelia business. SoundHound isn’t clear when this deal will close. If immediately, Amelia is a $30 million business in 2024, growing at a roughly 50% clip.

Again, the question is why the owners of Amelia would want to cash out at this valuation. If the deal closes later in the year, the new AI business has very limited growth more supportive of the low valuation, even when assuming the debt portion.

SoundHound AI lists an expectation to have $160 million in cash and $39 million in debt at closing. The company ended Q2 with $201 million in cash, suggesting a potential offsetting cash amount to cover some of the debt payments along with the assumption of $39 million in debt.

The stock has a current market cap of $1.66 billion based on the 332 million shares outstanding. The merger only boosts outstanding shares to a minimal 13 million, again questioning why Amelia holders would want in on this valuation.

SoundHound AI still trades at 12x updated sales targets for 2025. The forward P/S multiple is lower, but the company will have substantially reduced organic growth rates. The market might push the stock higher based on some misunderstanding of organic sales growth dynamic when SoundHound AI reports 2025 quarters, but the gains won’t hold.

Takeaway

The key investor takeaway is that SoundHound AI still isn’t producing the growth at scale to make the stock attractive. The Amelia deal isn’t as appealing as the headlines, and likely a distraction from already appealing market opportunities in automotive and restaurant voice AI.

The stock might rally on some sales growth confusion after the deal closes, but SoundHound AI isn’t appealing unless the stock dips back to prior lows.

Read the full article here

")

")