Introduction

SoFi (NASDAQ:SOFI) ended 2023 with a huge bang, producing Q4 financial results that surpassed all expectations.

Even the bears were surprised.

Growth accelerated, profitability skyrocketed, and management provided their outlook for the next three years — solidifying SoFi’s path of becoming a top 10 bank.

Our 2023 results have reinforced my conviction in our long-term potential and our ability to achieve our aspiration to become a top 10 financial institution.

(CEO Anthony Noto — SoFi FY2023 Q4 Earnings Call)

And now that the company is on a stronger fundamental footing, more people are turning increasingly bullish on SoFi.

Time and time again, SoFi continues to execute — with profits set to explode in the next few years and with a short interest of more than 13%, it looks like bears are next on the execution list.

Growth

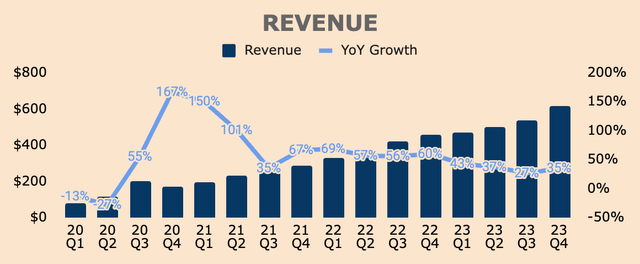

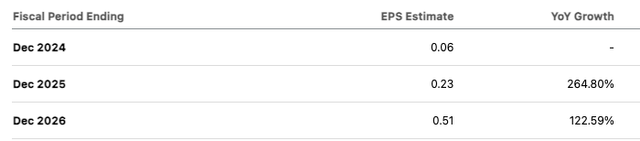

SoFi capped the year with a $615M Revenue in Q4, up by 35% YoY, which is an acceleration from Q3’s growth of 27%. This beat analyst estimates by 4%.

Q4 Adjusted Revenue was $594M, up by 34% YoY, extending SoFi’s streak of record Adjusted Revenue to 11 consecutive quarters.

Author’s Analysis

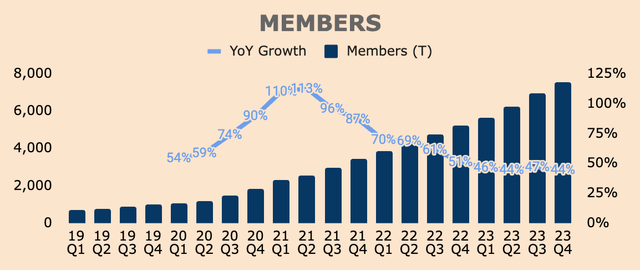

SoFi’s record-breaking performance was driven by its expanding Member base, which grew 44% YoY to 7.5M. On a sequential basis, SoFi added 585K new Members in Q4, well above its quarterly guidance of 500K, which goes to show how much customers love SoFi’s digital banking solutions.

Author’s Analysis

Member growth is important because the number of Members is a leading indicator of future growth, and as more Members join the platform, the more Members there are that SoFi can monetize through its different products, which ultimately contributes to Revenue growth.

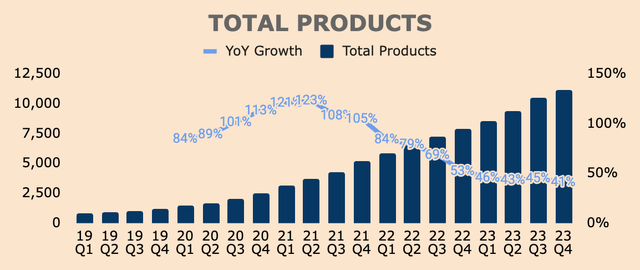

As you can see, product adoption continues to be robust. The company added 695K new Products, bringing Total Products to 11.1M in Q4, up by 41% YoY. If not for the closure of its digital assets business, Total Product growth would have been 45% YoY.

Author’s Analysis

That said, strong Member and Product growth led to record Revenue across all three business segments.

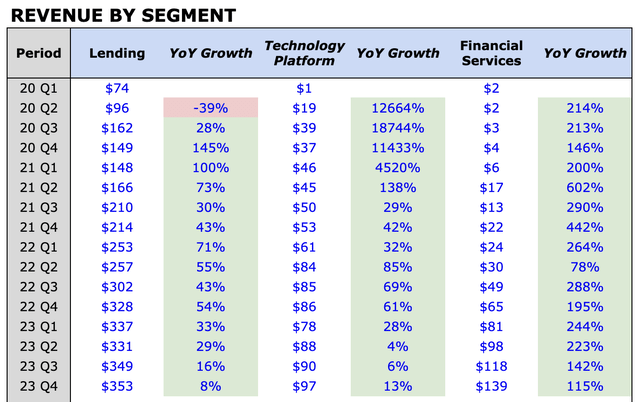

- Q4 Lending Revenue was $353M, up by 8% YoY, driven by higher loan balances and net interest margin. But notice the major slowdown in the segment. This was intentional as management planned for lower originations in 2024 — Q4 Loan Originations grew 45% YoY to $4.3B, but this was $0.8B lower QoQ.

- Q4 Tech Platform Revenue was $97M, up 13% YoY. As you can see, growth for the segment continued to accelerate, driven by strong organic growth of existing partners and new clients, which consequently led to an 11% YoY growth in Tech Platform Accounts to 145M. Moving forward, management expects the segment to continue to accelerate as the deal pipeline remains robust.

- Q4 Financial Services Revenue was $139M, up by 115% YoY, which marks the sixth consecutive quarter of triple-digit growth. Truly astounding. Growth was mainly due to strong product adoption, which grew 45% YoY to 9.5B, as well as improved monetization, with Revenue per Product up nearly 50% YoY to $59. What’s worth mentioning is that the segment exceeded $1.5B in point-of-sale debit transaction volume in Q4, which is up nearly 3x YoY.

Author’s Analysis

All in all, a very strong quarter in terms of growth.

Record Revenue, record Members, record Products.

Just flawless execution. Nothing else.

But here’s the best part.

Profitability

SoFi’s profitability stole the spotlight in Q4.

Let’s work our way down the income statement.

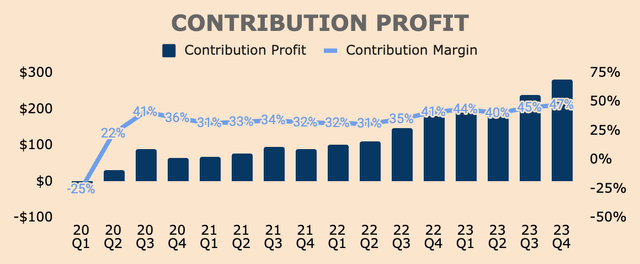

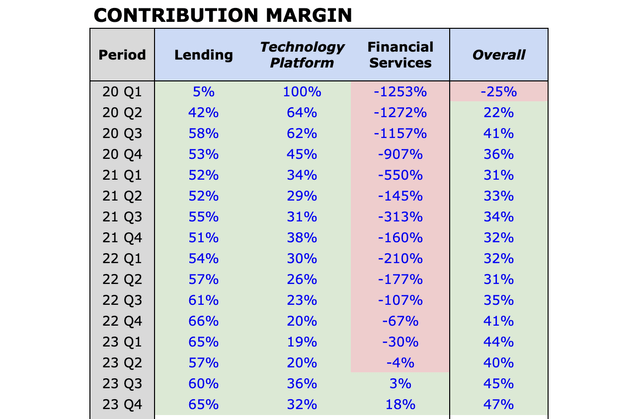

First, Q4 Contribution Profit, which is Net Revenue minus Direct Expenses, was $282M, representing a Contribution Margin of 47%. As you can see, margins continue to expand, demonstrating economies of scale within the business.

Author’s Analysis

Here’s what Contribution Profit looks like for each segment:

- Q4 Lending Contribution Profit was $226M. Contribution Margin was 65%, which was down 100 basis points YoY. However, this was a 500 basis point improvement QoQ, reflecting the recovery in the home loans and student loans segments. Regardless, the long-term margin trend is up with the possibility of reaching 70% by the end of 2024 or 2025.

- Q4 Tech Platform Contribution Profit was $31M at a 32% Contribution Margin, which is up 1,200 basis points YoY, as the segment regains momentum.

- Q4 Financial Services Contribution Profit was $25M. Contribution Margin improved massively to 18%, from (67)% last year and 3% last quarter. This was mainly driven by strong operating leverage due to blistering growth and improved monetization. As a matter of fact, operating leverage was so strong that the segment generated $74M in incremental Revenue with only $6M in incremental Direct Expenses, resulting in an incremental Contribution Margin of 92%! This is despite heavily investing in its Credit Card and Invest businesses, which have losses of over $100M on an annual run rate basis. Safe to say, the 18% Contribution Margin is still far from its optimal point.

Author’s Analysis

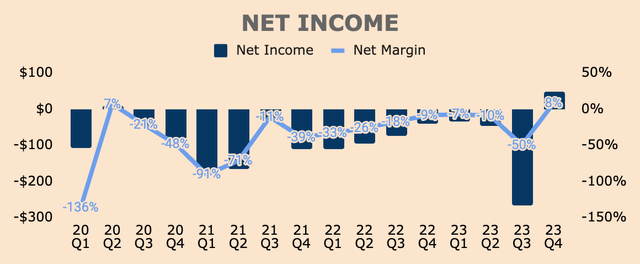

As a result of improved profitability across all three businesses, SoFi generated positive GAAP Net Income of $48M in Q4, a significant jump from last year’s $(40)M loss. GAAP EPS was $0.02, beating analyst estimates of $0.00.

Again, the company gained operating leverage as:

- Total Operating Expenses as a % of Revenue dropped 1,700 basis points YoY

- Sales and Marketing Expenses as a % of Revenue dropped 1,000 basis points YoY

Author’s Analysis

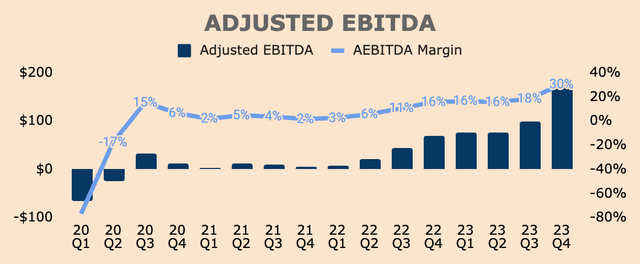

Adjusted EBITDA — which is a proxy for Cash Flow — was $181M, representing an Adjusted EBITDA Margin of 30%, up 1,200 basis points YoY, reaching management’s long-term target of 30%!

Q4 Incremental Adjusted EBITDA Margin was 74%, meaning, there’s still much more room for margin expansion moving forward.

Author’s Analysis

In short, management promised and they delivered.

Simple as that.

Just take a look at all the charts above — each and every profitability metric improved significantly with no signs of slowing down.

I know extrapolation is a dangerous practice but given the strong growth and profitability momentum of the business, I don’t see why profitability won’t improve from here.

This is the Financial Services Productivity Loop strategy in action — and we can see it becoming more prevalent with each passing quarter.

As seen in Q4, the resulting network effects are beginning to deliver exponential improvement to the business, which should drive monumental earnings growth for years to come.

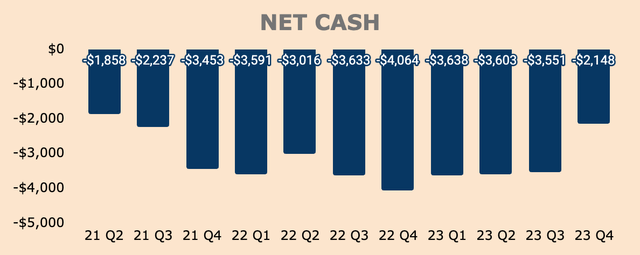

Health

SoFi’s balance sheet continues to strengthen as well, with Net Cash improving $1.4B QoQ, to $(2.1)B as of Q4.

SoFi also grew Tangible Book Value for the sixth consecutive quarter by $0.2B, to $3.5B as of Q4.

Author’s Analysis

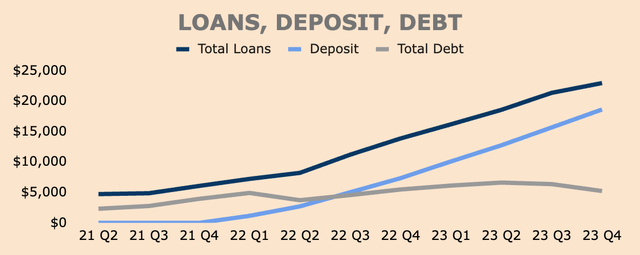

Its balance sheet continues to expand as well:

- Loans grew $1.6B QoQ to $23.0B

- Deposits grew $2.9B QoQ to $18.6B

- Debt shrank by $1.1B QoQ to $5.2B

If you haven’t noticed, deposit growth outpaced loan growth, which enabled SoFi to reduce its debt exposure, resulting in a lower cost of funding for its loans.

As such, SoFi’s Net Interest Margin expanded to 6.02%, up from 5.99% QoQ and 5.94% YoY.

Author’s Analysis

In addition, SoFi maintains a stringent credit policy, approving loans only to high-quality customers. In Q4, new direct deposit accounts have a median FICO score of 744.

Outlook

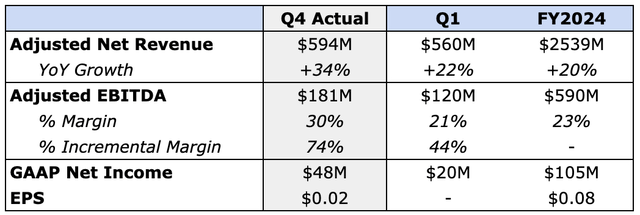

Note: Unless otherwise noted, I will only be referring to the high-end of management’s guidance.

In my opinion, Q1 guidance was a little soft. I have also included Q4 results for comparison.

As you can see, Q1 Adjusted Revenue is expected to be $560M, up 22% YoY, which is a material slowdown from Q4’s growth of 34%. In addition, management expects Q1 Adjusted Revenue to be lower than Q4’s figure, which also means that SoFi is expected to break its 11-quarter streak of record Adjusted Revenue.

Due to the sequential drop in Adjusted Revenue, management expects lower profits as well. In Q1, management expects Adjusted EBITDA of $120M at a 21% Adjusted EBITDA Margin, which is down 900 basis points QoQ.

Fortunately, management expects to maintain GAAP Net Income profitability in Q1 with a Net Income of $20M for the quarter.

Author’s Analysis

In terms of the full year, management has the following assumptions for 2024 Adjusted Revenue:

- Lending Revenue to be 95% of 2023 levels

- Financial Services and Tech Platform Revenue to grow 75% YoY and 20% YoY, respectively. Combined, they should “grow 50% or more”

- 50-50 Revenue split between the Lending segment and the other two segments.

- 2.3M new Members added in 2024, bringing the total number of Members to 9.8M, up 30% YoY.

Based on these assumptions, I’ve calculated an estimated $2.5B of Adjusted Revenue for 2024, which is about a 20% increase YoY. Again, this is quite a slowdown from last year’s growth of 35%.

In terms of profitability, management expects an Adjusted EBITDA of $590M for the year, with “Adjusted EBITDA Margin ramping to 30% by year end”.

And finally, 2024 Net Income is expected to be $105M or an EPS of $0.08.

At first glance, guidance seems disappointing. But keep in mind that management is taking a very conservative approach to their financial guidance:

- First, management is expecting some sort of a recession in 2024, with GDP down for the year, a 5%+ unemployment rate, and four rate cuts.

- Second, given macro uncertainties, management is intentionally limiting Lending growth below its level of demand and capacity.

- Third, they are assuming “no significant new business launches or acquisitions” in their outlook, with growth entirely coming from existing businesses.

In other words, if the opposite were true for each of the reasons above, we could see SoFi easily beat their guidance. In addition, management has a history of sandbagging guidance, so don’t be surprised if we see SoFi outperform expectations in 2024.

In short, 2024 guidance seems too conservative — a perfect setup for another year of outperformance.

That said, management also expects $0.80 per share in GAAP EPS in 2026. Beyond 2026, they also see 20% to 25% EPS growth. I would take these longer-term goals with a grain of salt but considering management’s strong execution thus far, I have very little doubt that management has what it takes to achieve their long-term goals.

However, based on today’s stock price of $8 and GAAP EPS of $0.80 in 2026. SoFi is now trading at just 10x its 2026 earnings — which is pretty darn cheap.

Speaking of which, let’s talk about valuation.

Valuation

A PE Ratio of 10x is incredibly cheap for a high-quality hypergrowth company like SoFi. However, 2026 EPS estimates are too far off, and thus, are not very helpful.

Instead, let’s take a look at some other metrics.

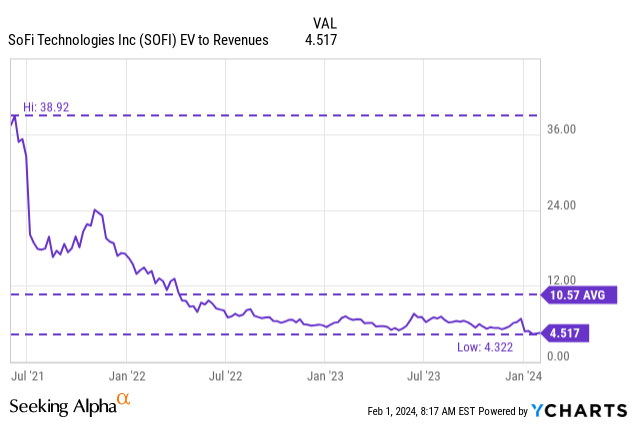

In terms of EV to Revenue, SoFi now trades at its lowest valuation multiple ever, at just 4.5x, well below its peak of 38.9x and average of 10.6x. Very attractive indeed.

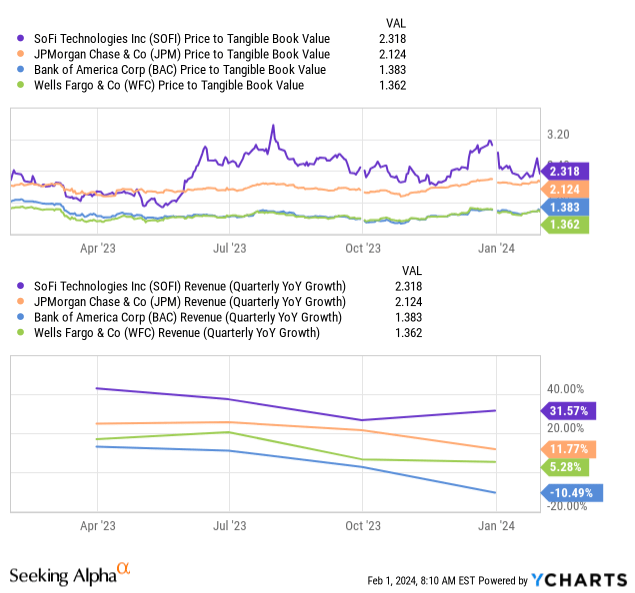

Some might argue that it’s inappropriate to value banks using Revenue multiples but here’s a more traditional metric. In terms of Price to Tangible Book Value, SoFi trades at a premium compared to the three largest banks in the US, at 2.3x.

However, SoFi is growing much faster than legacy banks, reflecting market share gains over incumbents. As such, the premium is well justified. In my view, SoFi may even look cheap since it’s growing multiple times faster than these legacy banks.

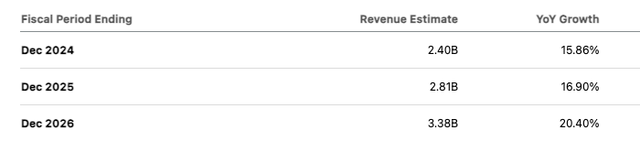

Also, analyst EPS estimates are way too low.

- Analysts expect $0.06 EPS in 2024 when management guided for $0.07 to $0.08.

- In addition, they expect $0.51 EPS in 2026 when management guided for $0.55 to $0.80.

Have they not learned that management has a history of obliterating estimates and guidance?

Seeking Alpha

The same goes for Revenue estimates:

- Analysts expect 2024 Revenue of $2.4B, up just 16% YoY. As I have discussed earlier, I expect 2024 Revenue of $2.5B, up 20% YoY.

Seeking Alpha

Simply put, analysts are too bearish on the stock. Combined with management’s overly conservative guidance, I think the bar is set too low for SoFi stock.

This is a perfect setup for outperformance — a classic case of underpromising and overdelivering — which should lead to earnings beats and upward revisions, and ultimately positive market reactions.

Let me remind you: management has a track record of strong execution.

And with 13% short interest as of this writing, it won’t be long before the bears get executed.

Risks

- Politically-driven: SoFi is largely driven by monetary policy and other regulations, which are unpredictable.

- Recession: A recession may lead to a surge in delinquencies and defaults, which may negatively affect SoFi’s Lending segment. However, SoFi has excellent credit quality with a high Capital Ratio of 15.3%, which positions the company well in an economic storm.

Thesis

SoFi’s Q4 results were nothing short of spectacular.

It was yet another record-breaking performance with all three business segments posting record Revenues.

Most impressive of all, the company turned GAAP Net Income profitable in Q4, which is a major reason why the stock popped 20%+ following its earnings release.

However, as I write this article, SoFi stock has given up pretty much all its post-earnings gains as investors digest the possibility of a “weak” 2024, given management’s ultra-conservative guidance.

But time and time again, management continues to execute — I will let them do the talking.

In the meantime, the stock still trades at attractive valuations, and with profits expected to explode in the coming years, bears better be careful.

The stock will eventually follow the fundamentals.

And the bears will eventually be executed.

Read the full article here