")

Smartsheet (NYSE:SMAR) is a well-established player in the competitive Project and Work Management [PWM] software space with its easy-to-use platform, especially popular among large enterprises. For long, I’ve been arguing that Smartsheet has a strong business model, being able to operate as a Rule of 40 company in the longer run, thanks to its sticky PWM platform. In my latest article on the company, I concluded:

Smartsheet tests the patience of investors, but I believe it’s worth waiting. Valuation of shares has reached quite conservative levels, which in case of positive fundamental surprises should result in large upside for shares. Recent conservative FY25 guidance has set a low bar for the upcoming quarters, which should limit downside in my opinion. It’s true, that Smartsheet became a show me story recently, but I believe the company will deserve investor’s trust rather sooner than later.

Since the time of writing, Smartsheet has published earnings for its Q1 FY25 quarter, which sparked a strong rally in shares. There haven’t been major positive surprises in the earnings print, but the accompanying earnings call included some notable positives, like the introduction of a new pricing model or the launch of Smartsheet’s new user interface.

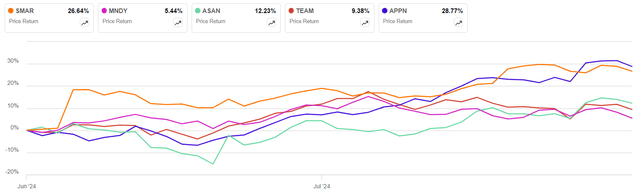

On the top of that, Reuters published an exclusive report recently claiming that Smartsheet has attracted acquisition interest from private equity firms. This has been a similar positive catalyst for shares, resulting in a ~27% gain since the beginning of June, making the company one of the best performers in the public PWM space:

Seeking Alpha

In the light of improving fundamentals and acquisition interest, there could be further positive surprises in the back half of the year, making the recent strong performance just the beginning of a larger rally.

In-line Q1 with catalysts lining up for the second half

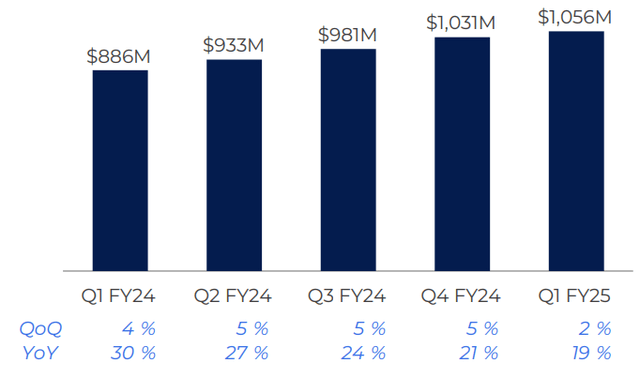

Smartsheet reported revenues of $263 million for its recently closed Q1 FY25 quarter, beating the average analyst estimate by ~2%. Annual recurring revenues (ARR), a more forward-looking topline growth metric the company began to emphasize, recently, came in at $1.056 billion growing 19% yoy:

Smartsheet Q1 earnings presentation

Looking at previous quarters shows that the trend of decreasing topline growth continued into Q1, although at a slightly more moderate pace. The enterprise segment remained the key strength of the company, where the dollar-based net retention rate stayed above 120%. The number of customers with ARR over $1 million increased 50% yoy to 72, representing the company’s fastest growing segment. On the other hand, the SMB segment continued to be a drag on overall growth with a dollar-based net retention rate close to 100%, meaning that the ARR of these companies remained constant yoy.

Enterprise strength has been driven by continued seat expansions at large companies and the cross-selling of Smartsheet’s capabilities, which now represent 35% of total subscription revenue. Control Center, Dynamic View and Data Shuttle remained the most popular capabilities over the quarter. Meanwhile, the weakness in the SMB segment has been the result of limited seat expansions due to continued cost control efforts in the space, coupled with slightly increasing churn.

The net result of these two effects has been a topline growth of 19%, which has been coupled by continuously improving margins thanks to strict control of operating costs and the utilization of economies of scale. Thanks to these efforts, the company decided to raise its full year operating margin guidance by 2%-points to 14-15% already after the first quarter of the year has passed, which is pretty impressive in my opinion.

Looking at the rest of the year, there have been interesting developments recently. Smartsheet decided to introduce a new pricing plan, which the company expects to be meaningfully revenue accretive in the longer run. The core idea behind the change is to increase the number of licensed Smartsheet users, who pay for the service. This will be accomplished by eliminating the free collaborator option from the plan, making organizations to choose whether specific employees license the platform (pay for it) or not going forward. The elimination of this freebie option will be compensated by a provisional member access, enabling temporary free access for members to try out the platform and engage with it.

To make the decision to stick with the platform as a licensed user easier, Smartsheet decided to decrease its price per user to some extent. The company already tested the new pricing model on some of its largest customers and shared positive feedback with investors on the Q1 FY25 earnings call.

The new plan will be effective for new customers from the 24th of June, while existing customers will transition when they renew their annual plan in 2025. Based on this, most of the financial impact will be felt next year, which could contribute to accelerating revenue growth in my opinion. Until then, it’s important to look out for management feedback on quarterly earnings calls as more and more new customers start with the new pricing plan.

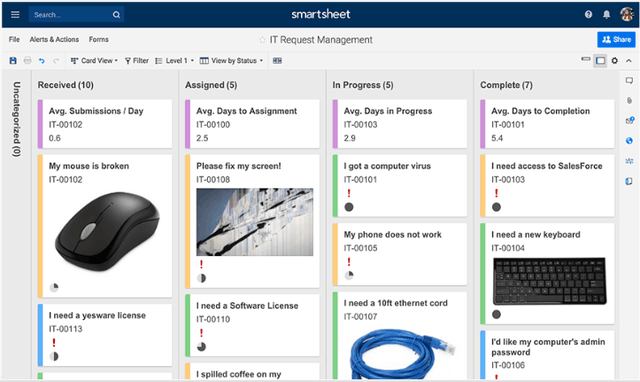

Another important development that could increase the engagement with Smartsheet’s platform has been the recent redesign of its user interface. The first step in this process has been the launch of Timeline View in April, which has been followed by Board View in July, representing a modern version of the previous Card View. This will be followed by the introduction of Table View later this year.

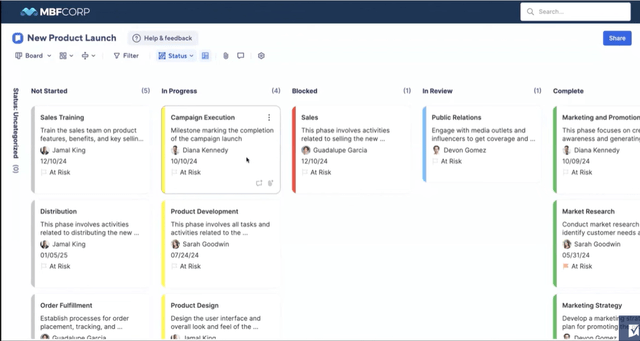

Looking at the new Board View and comparing it with its predecessor (Card View) I believe the new design is clean, transparent and much more aligned with current standards:

Card View (old):

Smartsheet.com

Board View (new):

Smartsheet.com

Over the long run, this could drive further engagement with the platform in my opinion, even if the launch has been somewhat bumpy based on reviews in Smartsheet’s community. There have been complaints about the page freezing or lagging, or even an instance where users couldn’t exit the promotional dialog of the new Board View. It will be worth to follow the company’s next earnings call closely, what management has to say about these issues. Nevertheless, I think these changes combined with the new pricing model have the potential to bring Smartsheet’s adoption in organizations to a next level, which could be evidenced in financial metrics rather next year.

Smartsheet emerging as favorable acquisition target

On the 18th of July, Reuters published an exclusive article on Smartsheet, claiming that the company has attracted acquisition interest from private buyout firms. Due to the stable business model centered around large enterprise customers combined with conservative valuation compared to peers, I haven’t been surprised. Smartsheet teamed up with investment bank Qatalyst Partners to review potential offers but hasn’t decided yet on the sale.

Looking at this quarter’s take-private deals, they enjoyed strong momentum in Q2 as 41 going-private deals have been announced, double the number that of Q1. This has been partly the result of narrowing valuation gaps between buyers and sellers, which has stayed consistently high since interest rates began to increase in mid-2022. I believe this shift could increase the chances of a successful takeout deal, which could quickly increase the value of Smartsheet’s shares if a deal is announced.

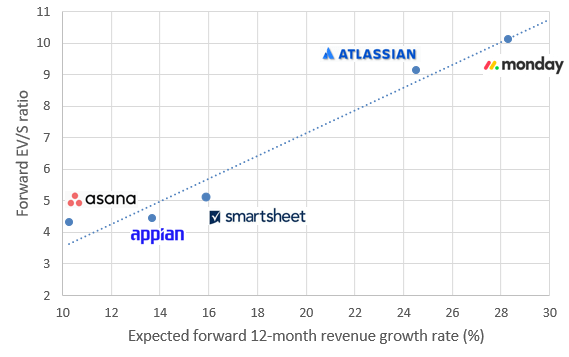

Looking at the company’s growth adjusted relative valuation, we can see that it has caught up to peers recently thanks to the ~30% run up in share price since the beginning of June:

Created by author based on company fundamentals

Smartsheet shares trade currently at an EV/Sales ratio of 5.1, which is coupled with an expected revenue growth rate of 16% for the next twelve months. Based on the respective EV/Sales and revenue combinations of competitors, Smartsheet’s shares could trade at an EV/Sales ratio of 5.66 (dotted line), approximately 10% higher than their current market price.

On the top of this 10% discount compared to peers based on sales-based multiples, I believe there is an additional premium applicable for Smartsheet’s shares resulting from the company’s advancement on the way to profitability. The company guided for 14-15% non-GAAP operating margin for FY25, which is significantly higher than most of its peers (e.g.: monday.com | Your go-to work platform (MNDY) 8-9%, Asana (ASAN) negative 8%). Besides, Smartsheet is very close to break even on a GAAP net income basis, with accumulating losses of only $9-9 million in the preceding two quarters. I believe this is an important metric for private equity investors as well, as it proves the efficiency of the company’s operating model.

Finally, I believe a premium for a potential takeover should also be taken into consideration as shares “only” increased ~5% since the news came out. In my experience, acquisitions usually happen at a ~20-30% premium compared to the share price at the deal announcement, so I believe this news is far from priced in completely yet.

Taking all these things together, I believe Smartsheet shares have the potential to reclaim the $50 level soon, combined with a private take-out option that could lead to a quick bounce in the share price to somewhere $60, 27% above current levels. This is in line with recent update from Jefferies, who claim that Smartsheet would be worth $57- $66 in case of a potential private takeout.

If we assume 50% probability for the takeout, this option would be worth ~$6 assuming a jump to $60 from current ~$47-48 levels. Adding the 10% valuation discount to this option, we get a share price of close to $60, which represents Smartsheet’s true potential more realistically in my opinion.

Risk factors

One important risk factor for Smartsheet investors is that a potential private takeout doesn’t realize. As shares jumped ~5% since the news came out, I believe the negative impact in such a case would be limited.

Another important risk factor to consider is the hardship of migrating existing customers to the new Views the company is introducing throughout the year. This could have short-term negative impacts on expansion if several customers face technical issues, but I believe these should be mitigated over the medium term.

Finally, let’s not forget that the project management software space is very competitive in nature, which could lead to pricing pressures over the longer run. However, based on management comments there are still many greenfield opportunities on the market, where Smartsheet competes only with in-house solutions.

Conclusion

Smartsheet shares currently trade at a price where they traded 5 years ago, with some large swings over these years. I believe recent company-specific news like private takeout interest and the redesign of the platform combined with pricing changes have the potential to finally unlock its real value. As I see limited potential for downside, I believe buying the shares now represents an excellent risk/reward opportunity.

Read the full article here