")

")

")

Shares of Sirius XM (NASDAQ:SIRI) have been a poor performer over the past year, losing 38% amid challenging subscriber trends and a questionable merger with Liberty’s tracking stock (LSXMA). I last covered Sirius in September, rating shares as a “sell,” given my concerns around this merger. Since then, the stock is down 21% while the market has rallied 21%. Given this dramatic underperformance, now is a good time to revisit shares. I remain bearish.

Seeking Alpha

Looking first to its fundamentals, Sirius reported Q2 earnings results on August 1st, and results were mixed. It earned $0.08, matching consensus, while revenue fell 3% from last year to $2.2 billion. It continues to target $1.2 billion of free cash flow and $2.7 billion of EBITDA this year. Subscriber revenue fell by $67 million to $1.66 billion, while advertising revenue was flat at $443 million.

Q2 results add to “melting ice cube” concerns

Today, SiriusXM is a highly cash generative business, but a challenge for shares has been determining whether this is a company that can sustain and grow cash flow over time or if cash flow will gradually erode, given competition from streaming platforms. This is critical to determining what type of multiple to value Sirius at. This quarter added to concerns that it is a business that is stable, at best, if not gradually declining.

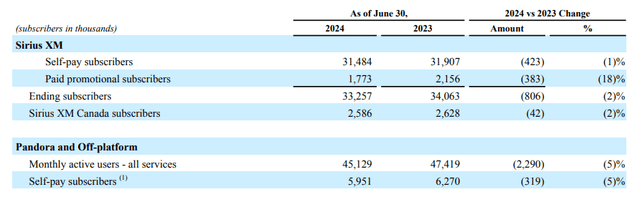

As you can see below, it continues to shed subscribers. Sirius subscribers are down 2%. Self-pay is down 1% while promotional was down 18% from a year ago, as it has had to rely more on free trials than promotional rates. Pandora was down 5%, as the service has struggled to compete against Spotify (SPOT), though some of the decline is also likely tied to efforts to gain pricing at Pandora.

SiriusXM

There was no sign of this pressure eroding in Q1. In SiriusXM, there was a 100k decline in subscribers to 33 million, while its Pandora unit saw a 41k drop in subscribers to 6 million. Within Sirius, there are several factors in play. Existing customer churn is steady at 1.5%. It is seeing increased auto sales help results, but this has been offset by a lower vehicle conversion rate.

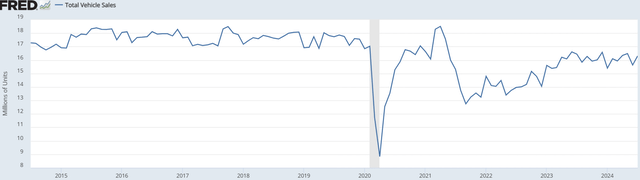

With many car purchases, there is a trial of Sirius included. When auto sales are higher, this translates to more Sirius trials, a positive. The auto sales market remains subdued vs pre-COVID levels, given high interest rates and affordability challenges. However, it has improved somewhat vs the past two years when supply chain issues limited production. Barring a recession, I expect auto sales to be at least flat to current levels, enabling a continuing pipeline of potential subscribers.

St. Louis Federal Reserve

Sirius has a healthy pipeline already of 7.4 million trials, though this was down slightly from 7.5 million last quarter. The problem is not that Sirius has a lack of potential subscribers, rather it is struggling to sign up trial users to a subscription. This has forced the company to become more promotional. Its average revenue per user (ARPU) was down $0.42 to $15.24. Declining revenue per consumer and a shrinking customer base make it hard to view this as anything but a business in gradual decline.

Cost controls are in focus

Given these topline pressures, Sirius has to aggressively manage costs, and so far, it is doing a good job of this. The company cut programming costs by 3% to $148 million, while revenue share was down 4% to $708 million. With much of its cost base tied to royalties/revenue share, there is natural benefit to expenses when revenue declines. Partially offsetting this, there was a 4% increase in sales and marketing to $228 million, though this spending has not really benefited revenue in a noticeable way. Still, given cost reductions, Sirius generated $702 million of EBITDA, flat from last year.

At a segment level, there has been some bifurcation. Within SiriusXM, cost controls have not been able to fully offset revenue pressures, given there is some fixed programming and operational costs. As a result, its gross margin of 60% was down 1% from last year, with gross profit of $986 million. By comparison, even with lower subscribers, Pandora revenue rose by 2% to $538 million thanks to higher pricing and flat advertising. Gross profits were $180 million. This unit’s gross margin rose to 33% from 29%.

This quarter, Pandora gains and corporate cost controls were able to offset declines within SiriusXM. However, with satellite ratio over 80% of the business, if this business continues to decline, it will be difficult for overall corporate results not to follow. While I do not see an argument for an acceleration in the business decline, it is also difficult to see a catalyst for causing subscriber momentum to flip back to positive.

The business generates substantial cash

Ultimately, even a business in modest decline can be attractive if it generates enough cash and is valued appropriately. Sirius is still a very cash generative business. Through six months, it has generated $475 million of free cash flow. Excluding working capital, free cash flow is tracking at $688 million. That has benefited from $91 million of share-based compensation. Still, the company is clearly on track to deliver about $1.2 billion of free cash flow this year, giving shares a 10% free cash flow yield. This safely covers its dividend, which yields 3.4% and costs about $400 million,

The company has also brought its balance sheet onto a better footing. It carries $9 billion of debt for 3.2x debt to EBITDA, in keeping with its low-to-mid 3x debt/EBITDA target. As a standalone entity, Sirius has its balance sheet where it needs to and can direct all free cash flow to shareholders. With a 10% free cash flow yield, even if it can hold cash flow steady, shares could have upside over time if the business were stable. This is where M&A concerns come into focus.

The Liberty deal remains a mixed bag.

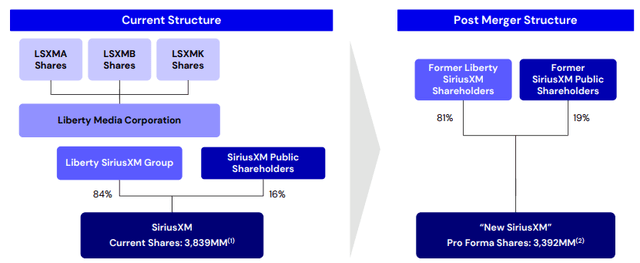

This September, Sirius and the Liberty SiriusXM tracking stock will close. As you can see, SIRI holders will receive 19% of the combined company, up from the 16% they currently own. In the original proposal, SIRI holders would own just 16% of the combined entity. In September, I had argued they should hold closer to 20%, and in the end, they will get close to this level.

SiriusXM

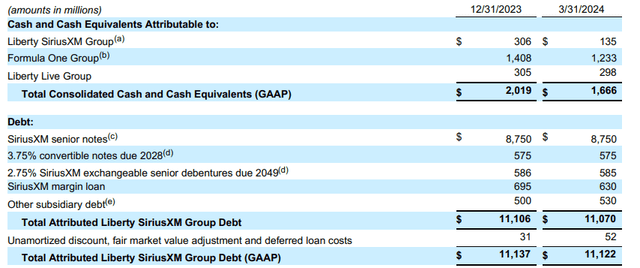

The one wrinkle is that Sirius will be taking on the margin loan and other subsidiary debt, at a $4.23 share price equivalent. As you can see below, Liberty has about $1.7 billion of net liabilities, excluding the convertible note.

Liberty Media

With these liabilities valued at $4.23/share, they reduce Liberty’s share allocation by ~400 million. Using the current market level of $3, they would be reduced by 566 million shares, so Liberty receives an additional 166 million shares worth about $500 million, given the $4.23 valuation.

Essentially, Liberty loses $1.2 billion of stock (400 million shares at $3) for handing over $1.7 billion of liabilities. This $500 million value transfer essentially leaves SIRI holders with ~4% less of the company than they otherwise should have. The more the stock falls, the more generous this $4.23 provision is. Because it assumes this debt, SIRI will now be 3.9x levered. With $800 million of cash flow after the dividend, it has substantial deleveraging capacity, but with at least $1.2 billion of debt reduction needed, this will be an 18-24 month process before we can see meaningful share repurchases.

Shares have further downside

Including share-based compensation (which is non-cash but dilutive) and additional debt costs, the new Sirius has about $1 billion of adjusted free cash flow capacity. Even with a 400 million share count reduction for the added liabilities, that gives shares a ~9% free cash flow yield. For a business with no clear trajectory to free cash flow growth and a need to focus on debt reduction well into 2026, that does not strike me as particularly cheap, especially, as we may see a wave of selling from Liberty holders post transaction.

Given these pressures, I would want to see a 12% free cash flow yield before buying. I target a 10+% return, and this provides for protection against a 2% terminal decline rate, given subscriber pressures. That would argue for buying shares closer to $2.50. Even with underperformance in shares over the past year, I remain a sell. Business momentum is weak, and this merger adds debt in a dilutive fashion. SIRI continues to be unattractive.

Read the full article here

")

")

")

")