")

")

")

Shopify (NYSE:SHOP) stock jumped by over 22% on the day it reported earnings last week, surprising investors with the incredible strength of its e-commerce business, despite most competitors delivering underwhelming results, citing economic weakness. The commerce giant proved its ability to continue adding new merchants at higher subscription prices, while also offering the best-in-class software platform to enable merchants to thrive, even with consumer spending trends weakening across the economy. If Shopify can deliver such solid earnings results in a weakening macro environment, imagine what the commerce giant will be able to deliver as the economy picks up again. In this article, we will be highlighting key aspects of Shopify’s strength, particularly relative to e-commerce king Amazon (AMZN). SHOP is being upgraded to a ‘buy’ rating.

In the previous article, we had discussed Shopify’s positioning in the AI revolution, and how the lack of insights relating to its generative AI-powered tools and assistant was concerning, particularly as other key players in the commerce space have already been offering statistical insights into their own Gen AI services.

Since then, the company held its ‘Shopify Editions’ event, where it offered some visibility into the progress they are making on this front. Perhaps most notably was that its Gen AI-powered assistant ‘Sidekick’ was already being used by thousands of merchants, and that it will become available to more and more businesses in 2024.

Although key statistical insights into measured performance improvements, such as enhanced conversion rates using automated image generation or increased sales for merchants, were still absent.

Nonetheless, the company’s robust execution through this weak macro backdrop gives me confidence they will indeed also deliver results on its generative AI-related investments.

Shopify’s noteworthy performance attributes

Shopify remains a solid growth stock, with the market projecting an EPS FWD Long-Term Growth (3-5Y CAGR) rate of 45.27%. And last quarter, the commerce giant reassured investors that it can continue growing at this high pace.

Gross Merchandise Volume [GMV], which represents the total value of all products sold by merchants through its platform, grew by 22% year-over-year last quarter, with Shopify CFO Jeff Hoffmeister proclaiming on the Q2 2024 Shopify earnings call:

The strong Q2 GMV was driven by same-store sales growth of our existing merchants, led by our Plus merchants, continued growth in the number of merchants on our platform globally

…

We saw solid growth across verticals with robust performance in health and beauty and food and beverages. We also saw solid growth in our largest category, apparel and accessories. Notably, this strength in GMV came against a backdrop of mixed consumer spend. We continue to gain market share in the US e-commerce market and abroad.

While Shopify saw healthy demand for merchants’ products, Amazon executives cited weakening consumer spend on their own earnings call, with Amazon CFO Brian Olsavsky sharing on the Q2 2024 Amazon earnings call:

We’re seeing a lot of the same consumer trends that we have been talking about for the last year. Consumers being careful with their spend, trading down, looking for lower ASP products, looking for deals. That continued into Q2, and we expect it to continue into Q3. We’re seeing signs of it continuing in Q3.

From a positive perspective, Amazon CEO Andy Jassy proclaimed that:

North America unit growth is meaningfully outpacing our sales growth as our continued work on selection, low prices, and delivery is resonating.

Indeed, Amazon.com is striving to become a destination for cheap goods. In fact, earlier this year, Amazon cut “fees for merchants selling clothing priced below $20”, in response to increased competition from Chinese rivals Shein and Temu.

Consequently, the e-commerce behemoth’s ‘third-party seller services’ revenue took a hit last quarter, growing by just 12%, compared to 18% over the same period last year. This indeed slowed Amazon’s revenue growth last quarter on the e-commerce side.

On the other hand, Shopify had raised subscription prices for its merchants over the past year, and CFO Jeff Hoffmeister boasted high retention rates on the Q2 2023 earnings call back in August 2023:

We are seeing our merchants, continue to remain on the platform rather than using the price change to move off-platform and largely remain on monthly plans versus moving to annual. For Shopify it provides us with more gross profit dollars to invest back into the business balanced with improved profitability.

The higher subscription prices have continued to boost Shopify’s top-line growth over the past several quarters, with ‘Subscription solutions’ revenue growing by 27% last quarter. Moreover, not only have merchants largely decided to stay with Shopify despite the price hikes, but the commerce software giant has also continued to attract more and more new merchants onto the platform, as Jeff Hoffmeister highlighted on the last earnings call (emphasis added):

For the quarter, the key drivers of our revenue growth were the GMV strength I just discussed, growth in subscription solutions revenue stemming from the growth in the number of merchants on our platform, the pricing changes that have been implemented in the past year

The fact that Shopify has continued to deliver strong merchant growth at higher subscription prices is testament to the rich value proposition of its software platform.

Furthermore, executives also cited their new marketing technology and strategy as key drivers of merchant growth, with Shopify President Harley Finkelstein sharing on the earnings call that:

We relentlessly test and optimize every single channel, keeping well within our average 18-month guardrail. Our tools and our AI models are crafted not just to operate but to excel leveraging emerging technologies to enhance our feedback loops. These tools provide sharper, more iterative feedback, enable more precise analysis, and deliver quicker signals, letting us identify patterns faster than ever, so we can swiftly adapt and respond. Now to give some examples of this agility and this discipline, consider this. After experimenting in a leading digital channel, a new emerging social platform in Q1, and observing substantial growth, we intensified our efforts in Q2. This led to a 51% increase in merchant acquisition quarter-over-quarter on that platform, all while staying within our financial guardrails.

This proves Shopify’s ability to innovate to continue driving top and bottom-line growth for shareholders.

So while Amazon is competitively pressured to lower its own merchant fees and striving to drive down the cost of their goods to appeal to consumers, Shopify boasts strong pricing power on its merchant base, and continues to take market share with notable marketing technology advancements.

Risks to the bull case for Shopify

AI race is heating up: Shopify is undoubtedly proving the fortitude of its software platform, with continuous growth in its merchant base and GMV, coupled with strong pricing power.

However, we are in the middle of an AI revolution, and while Shopify had rolled out various generative AI-powered tools last year that help merchants with their day-to-day tasks, such as automated product descriptions and image generation, executives have barely offered any insights into whether and how these new services have boosted merchant performance.

While Shopify was successfully able to raise prices on its merchants last year while proclaiming high retention rates, the commerce giant’s ability to raise prices again on its merchants in a several years’ time will highly depend on the value proposition of its generative AI-powered tools and services.

Consider the fact that recently, furniture retail giant ‘Ikea’ (which is not a Shopify customer) reportedly proclaimed the higher sales it is witnessing through its app using generative AI models provided by cloud providers:

On the IKEA app, the company introduced an experience called IKEA Kreativ that lets users capture visuals of their rooms, delete existing furniture and then visualize what IKEA furniture would look like in that space.

…

On the initial version of Kreativ, customers who engaged with the experience were four times more likely to make a purchase than those who simply used the app, and seven times more likely to make a purchase than those who only went on the website.

These are the kind of insights we need to hear from Shopify executives boasting about how their AI tools are helping merchants boost their own sales. As this will be the kind of technology that will be essential to continue attracting large enterprises, as well as smaller businesses, to the Shopify platform in the generative AI era.

The point is, the AI race is moving fast, with new, more powerful AI models being released on a frequent basis, unlocking new commerce capabilities with quantitative results. So from this perspective, Shopify executives merely mentioning progress on its generative AI features during earnings calls is discouraging. The software giant has yet to convince both merchants and investors that its own generative AI-powered services will be promising revenue drivers going forward.

With cloud providers making it progressively easier for businesses to build their own generative AI-powered apps and features, supported by natural language coding assistants (e.g. Microsoft’s GitHub Copilot), there is a risk that enterprises become increasingly inclined to build and deploy their own generative AI-powered commerce features, making them less reliant on Shopify’s services. Therefore, Shopify will need to move faster on this front to sustain share price performance from here.

Of course, this is not to say that we should underestimate Shopify in the AI era, either. The commerce giant has certainly proven its ability to leverage the power of its platform and extensive merchant base, conducive to a large commercial database, to innovate new, unique products and services. A great example of this would be ‘Shopify Audiences’, whereby it leverages anonymized sales data from its merchant base to predict customer demand for other adjacent products, feeding into other merchants’ advertising campaigns to help them target high-conversion consumers.

Additionally, as discussed earlier, Shopify’s own AI-powered marketing technology has helped it attract more and more merchants to drive sales revenue growth for itself.

So the software giant boasts a track record of innovating and driving continuous growth, which gives me confidence that Shopify will be able to sustain this prowess in the AI era, leveraging the massive database it possesses to innovate unique, generative AI-powered commerce tools.

Macroeconomic risks: The stock’s performance over the next few years, and the valuation multiple the market will assign it, will highly depend on economic conditions as well. For instance, a higher interest rate environment due to a resurgence in inflation would subdue the prospects of multiple expansion for growth stocks like SHOP. The market is also anticipating a recession soon, which could also potentially undermine Shopify’s ability to achieve the high EPS growth projections, or curb investors’ enthusiasm around growth stocks overall, restraining stock price performance.

Shopify financial performance and valuation

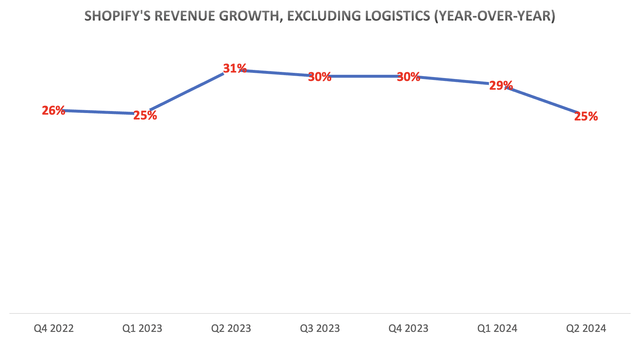

Now a key reason why Shopify stock fell into bear market territory, down by 42% from its 52-week high earlier this year, was the concerns around slowing top-line revenue growth. Back in May 2024, earnings guidance from the company for Q2 2024 projected that the revenue growth rate would be in the “low to mid-20s”. The company delivered at the top of this guidance range, with revenue growing by 25% last quarter, excluding the impact of the sale of its logistics business in the first half of last year.

Nexus Research, data compiled from company filings

The top of the range results surprised Wall Street, amid underwhelming results from key e-commerce rivals prior to Shopify’s results, consequently catapulting the stock higher post-results. The stock is now only down by 21% from its 52-week-high.

Now for Q3 2024, the company has once again guided revenue growth to be in the “low to mid-20s”. Though, investors can be confident that Shopify will be able to deliver growth rates near the top of the range again, particularly as the company’s new marketing technology pays off in the form of on-boarding more and more merchants onto the platform, as discussed earlier.

Moreover, given the 18-month payback period of its marketing strategy, CFO Jeff Hoffmeister guided that:

as we think about the marketing spend, we do, based on the 18-month average payback periods, think about this as something which drives 2025 more than it does 2024

Therefore, while revenue growth has been slowing this year to around the mid-20s, it is expected to re-accelerate higher next year as the company attracts a growing number of merchants onto its platform thanks to its targeted marketing strategies paying off.

Though over the near-term, the increased marketing spend means higher operating expenses, as the CFO guided on the earnings call:

The largest drivers of our Q3 operating expense growth compared to the prior year are marketing and compensation expenses. On marketing, we plan to continue spending on opportunities that fall within an average 18-month payback period and the opportunities to support our key growth initiatives, including international markets, enterprise and point of sale.

Investors should not be too concerned about the rising operating expenses, as the increased marketing spend is clearly already paying off in the form of new merchant additions and consequently higher top-line revenue, as per the citation from Finkelstein earlier in the article. Shopify’s executives doubling down on a well-tested marketing strategy with proven results is an encouraging development for shareholders, as it is conducive to higher top and bottom-line growth going forward, driving the stock price higher.

In fact, the rising marketing costs are well-aligned with revenue growth, as the CFO outlined:

Increases in marketing, we had a year-over-year increase in our affiliate partner payouts. And since these payouts happen only upon a new merchant joining, there’s a clear sign of adding more merchants to the platform

This is testament to executives’ discipline of driving future revenue growth in a cost-efficient manner.

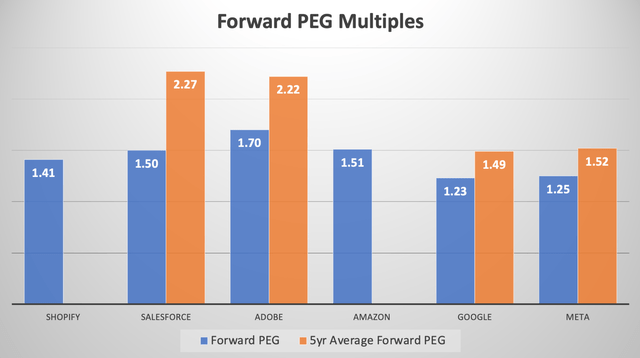

Now with the company delivering encouraging results and offering an improving growth outlook, Shopify’s valuation is certainly not cheap, with SHOP trading at a Forward Price to Cash Flow multiple of 58.93x, and a Forward Price to Earnings ratio of 63.66x.

Though, it is not unusual for a growth stock to trade at such high multiples, with the commerce giant having more than doubled its free cash flow margin to 16% last quarter. Furthermore, Shopify’s EPS FWD Long-Term Growth (3-5Y CAGR) rate is 45.27%, and adjusting the Forward PE by this expected growth rate gives us a Forward Price-Earnings-Growth [PEG] multiple of 1.43x.

Below, we compare this Forward PEG ratio to those of competitors and other key players in the digital commerce space. I have included Google and Meta in the comparison as well, because in the AI era, the services provided by these two tech giants will increasingly overlap with what Shopify strives to offer its merchants; generative AI-powered solutions to help them sell more products.

Nexus Research, data compiled from Seeking Alpha

Shopify stock is cheaper than commerce-software competitors Salesforce and Adobe, and also cheaper than e-commerce king Amazon on a Forward PEG basis. With regards to Google and Meta, the two digital advertising giants are particularly cheap at the moment, as covered in my previous articles covering each stock.

Though, what is of greater value here are the 5-year average Forward PEG ratios of the large and mega-cap commerce stocks, providing us comparative indicators as to what multiple SHOP stock could trade at as it grows larger.

Shopify is currently a $90 billion company, though with earnings expected to grow at such a fast pace of 45% over the next 3-5 years, the stock is expected to become as large as Salesforce and Adobe in a few years’ time, which are both worth around $240 billion, and boast 5-year average Forward PEG multiples of around 2.20x. This suggests room for potential multiple expansion for Shopify shares from here.

Being the leading commerce-software platform provider, and analysts at BofA recently also affirming Shopify’s “market leadership with a number of defensible competitive advantages”, it would not be out of question for SHOP to also trade at a Forward PEG multiple of above 2 going forward. This would be in line with what large-cap tech stocks, with strong market positioning and defensible moats, have historically commanded.

Alternatively, even if it continues to trade at a Forward PEG ratio of around 1.50x, in line with what digital advertising giants Google and Meta have been trading at, there is still scope for lucrative multi-bagger returns ahead.

As mentioned earlier, Shopify’s EPS is expected to grow at a Compounded Annual Growth Rate of 45% over the next 3 to 5 years. Assuming that the stock price grows commensurately with earnings, rallying 45% annually over the next 3 years and thereby sustaining a Forward PE ratio of around 64x, then the stock is set to triple over this period. Moreover, if Shopify can sustain a 45% EPS compounded annual growth rate over the next 5 years, then the stock price could multiply by almost 6.5x.

That being said, the reason SHOP is able to command a Forward PE ratio of 64x today is because of its attractively high EPS growth rate projection of 45%. Though at the end of the 3 to 5-year period, future growth rate projections could potentially be much lower, as companies’ earnings growth rates naturally slow down as they grow larger. For example, Salesforce and Adobe’s EPS FWD Long-Term Growth (3-5Y CAGR) rates are projected to be around 17% each.

So let’s say Shopify’s EPS growth rate projections in 5 years’ time halves to around 22.5%, with the stock correspondingly trading at a Forward PE ratio of around 30x instead of over 60x. In this scenario, instead of a 6.5x stock investment return, the stock could return around 3x, which would still enable investors to triple their money in 5 years’ time.

Additionally, this projection is assuming that Shopify stock maintains its current Forward PEG ratio of 1.41x. But as discussed earlier, the market could indeed assign a Forward PEG multiple of over 2x going forward, given Shopify’s strengthening market position as it grows larger, and in line with how large-cap stocks with strong moats have traded historically. Even if we assume a ratio of 2x going forward, it would imply multiple expansion of around 43% for the stock price.

So on top of the stock potentially tripling over the next 3 to 5 years based off of a high EPS growth rate of 45%, the stock price could also see an additional 40%+ uplift over this period from Forward PEG multiple expansion, creating the possibility of the stock returning around 4x in 3-5 years’ time.

Although, as discussed earlier in the risks section, worsening macroeconomic conditions over the next few years could make it more challenging to realize multi-bagger returns for SHOP investors. And Shopify will also need to step up its game in offering new, innovate generative AI-powered services and features to sustain the value proposition of its platform and achieve the high earnings growth rates expected of it.

Nonetheless, with Shopify proving to the market that it can continue growing its merchant base and maintain healthy financial performance even amid a weakening macro backdrop relative to competitors, the company is certainly winning investors’ confidence that it can achieve the 45% average EPS growth rate projections over the next several years. Hence, setting the stock up for multi-bagger returns ahead. Shopify stock has been upgraded to a ‘buy’.

Read the full article here

")

")

")

")