")

")

ServiceNow, Inc. (NYSE:NOW) released its Q2 results on July 24th after the market closed, beating the market expectations and raising the subscription revenues and operating margin guidance for FY24. I presented my “Strong Buy” thesis in my previous coverage published in March 2024, highlighting its future platforms powered by AI. Benefiting from the megatrend of cloud computing and AI training/inference, ServiceNow is likely to deliver 20%+ revenue growth in the near future, driven by its market expansion into mid-office and back-office platforms. I reiterate a “Strong Buy” rating with a one-year price target of $920 per share.

Now Assist Powers ServiceNow’s Platforms

My biggest takeaway from the earnings call is ServiceNow’s strong growth in its Now Assist, with net new annual contract value (ACV) doubling quarter-over-quarter. Management has disclosed that the company signed 11 Now Assist Deals with $1 million+ ACV in Q2, two of which were over $5 billion.

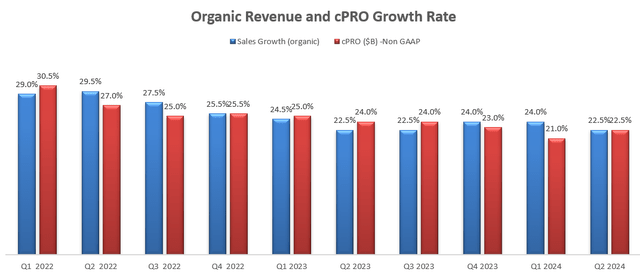

As discussed in my previous coverage, ServiceNow has been applying its AI technology to its platforms, which fuels the organic revenue and order growth. As depicted in the chart below, ServiceNow delivered 22.5% growth in both organic revenue and current remaining performance obligations (cPRO).

ServiceNow quarterly earnings

I anticipate Now Assist and other AI technologies will continue to propel the growth of ServiceNow’s major platforms for the following reasons:

- ServiceNow has launched Now Assist for IT Service Management, Customer Service Management, HR Service Delivery and Creators. By incorporating AI technology, ServiceNow has been expanding its total addressable markets (TAM), providing more runway for future growth.

- Enterprise customers can leverage ServiceNow’s AI platform to improve the operating efficiency for their back-office and mid-office operations. For instance, with the AI technology, ServiceNow’s own IT help desk could save 45 minutes per case and customer service. It is inevitable that the combination of AI and ServiceNow’s platforms could improve the efficiency for enterprise customers.

- During the earnings call, the management indicated an acceleration in the number of large deals. Their focus on the comprehensive IT solutions could help its sales team close larger deals.

FY24 and Valuation Update

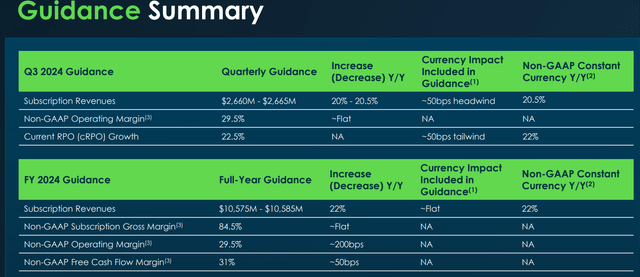

ServiceNow raised its guidance for both top line and margin expansion, as detailed in the table below.

ServiceNow Quarterly Presentation

It is impressive that ServiceNow can deliver such high growth in enterprise software, amid a challenging macro environment. I am considering the following factors for its near-term growth:

- cPRO is a leading indicator of ServiceNow’s future revenue growth. It is notable that ServiceNow has been growing its cPRO by 20%+ over the past few quarters. The high growth of current remaining performance obligations could translate into revenue growth in the near future.

- On July 24th, ServiceNow announced the acquisition of Raytion to enhance its AI-powered search and knowledge management capabilities. I favor this deal, as the combination of Raytion’s platform and ServiceNow’s Now Assist could potentially boost the adoption of AI-powered ServiceNow platforms.

I anticipate ServiceNow will achieve 23.8% growth in revenue for FY24, assuming 20% growth in its core platforms including IT management, Customer Service Management and HR Service Management; 2% growth from AI add-ons; 0.8% growth from acquisitions.

For the growth from FY25 onwards, I anticipate the company will grow its revenue by 20.8% assuming:

- Core platform growth: 15%. The growth rate presumes ServiceNow will continue to penetrate the massive enterprise customer base.

- New platform growth from TAM expansion: 5%. ServiceNow has a long track record of expanding its major platforms across mid-office and back-office markets.

- Assuming the company will allocate 3% of total revenue towards acquisitions, contributing 0.8% to topline growth.

I forecast ServiceNow will expand its margin by 250bps per year, reaching 33.5% by FY33, assuming:

- 100bps expansion from gross profits, driven by new product launch and large deals

- 100bps operating leverage from R&D expenses, as the company scales its businesses

- 50bps operating leverage from SG&A, driven by operation efficiencies.

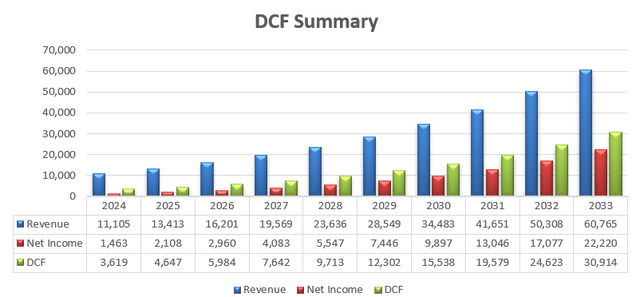

The discounted cash flow (“DCF”) summary can be found as follows:

ServiceNow DCF – Author’s Calculations

I calculate the free cash flow from equity as follows:

ServiceNow DCF – Author’s Calculations

The cost of equity is calculated to be 15% assuming: risk-free rate of 4.2% (US 10Y Treasury Yield); beta of 1.65 (SA); and an equity risk premium of 7%.

Discounting all the future free cash flow, the one-year price target is calculated to be $920 per share.

Key Risks

During the earnings call, ServiceNow announced that CJ Desai, the President and COO, would offer his resignation from the company effective immediately. This was due to a policy violation related to a government contract and the hiring of a former US Army official. The investigation indicates that ServiceNow has an internal management issue with hiring policies. While ServiceNow treated the incident seriously, the management change could potentially create some disruptions in its internal operations and external sales activities with the public sector.

Conclusion

Now Assist has become a strategic technology for ServiceNow, as the AI technology could power ServiceNow’s core platforms, accelerating its revenue and cPRO growth. I reiterate a “Strong Buy” rating with a one-year price target of $920 per share.

Read the full article here

")

")

: Medical Properties Trust Stock (NYSE:MPW)")