")

")

Safe Bulkers Inc. (NYSE:SB) has seen a 100% bull run in their share price between November 2023 and June 2024.

Currently, they are in a 20% pullback, after reporting mixed earnings results in Q2 2024.

In this article, I will cover some of their highlights during Q2 2024, including some of the headwinds that the company is currently facing, and I will look at different factors, including share buybacks, financial metrics, and price action, to explain the rationale behind my Hold rating.

As always, I will begin with a company overview section for those readers new to Safe Bulkers.

Company Overview

Safe Bulkers is a Monaco-based global shipping company that leases its fleet of 46 dry bulk vessels to other shipping companies.

I considered mentioning that they have an additional 8 new build vessels, expected to be delivered between 2024 – 2027. If you read my article on StealthGas, you know by now that I highly favor new and modern vessels.

The main reason is due to higher operational performance. In other words, less downtimes and more fuel efficiency.

However, these newer carriers need a crew that requires more training to operate efficiently, and that means higher wages and training fees.

Across all their current vessels, the aggregate carrying capacity is 4.6 million DWT. This is a relatively small amount, compared to some of their competitors, like Star Bulk Carriers Corp (15.6 million DWT), Navios Maritime Partners (9.17 million DWT), or Maran Dry Management (7.96 million DWT).

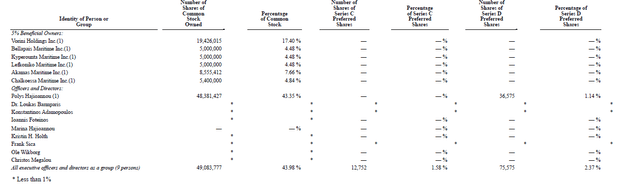

In regards to their ownership, I considered including some data from their latest 20-F (please note that this is for the year ending on December 31, 2023). The CEO and Chairman, Polys Hajioannou, controls approximately 43.35% of the outstanding common stock. He has been leading Safe Bulkers since 2008.

SEC – 20F

Given that the collective ownership of all directors and executive members (9 in total) was 43.98%, I am disappointed that there are no members owning more than 1% of the company.

I generally prefer companies where most of the management team has significant skin in the game.

Recent Performance

As always, I like to start with the dessert, so I will cover the headwinds during Q2 2024.

Considering that iron ore and steel are critical commodities for the dry bulk shipping industry, any weakness in these markets has a direct impact on the demand for shipping services.

If we have a quick look at SLX, the decrease of 14% YTD doesn’t look very promising.

Additionally, China has been ramping up its investment in renewables, with a 12% YoY increase in renewable energy generation in the first half of 2024. This overshadowed their 6% growth in fossil fuels, which I find it concerning given that it could impact global dry bulk rates.

Additionally, there has been a reduction in backhaul cargoes from the Far East to Europe. In other words, there was a decrease in goods shipped on the return leg from the Far East. In my view, this can negatively impact Safe Bulkers, as the demand for their vessels may decrease due to the reduced profitability of these routes.

However, they had an increase in charter rates, especially in the Capesize segment. If we consider all 8 of their Capesize vessels, they have an average remaining charter duration of 2.4 years at an average day rate of $24,500.

Additionally, the Panamax segment also saw an increase in charter rates, with an average rate of $15,000 per day. In my view, this represents a decent amount of cash flow.

I am also encouraged by the increase in the time charter equivalent (TCE) rate averaging $18,615/day during Q2 2024, compared to $17,271/day in Q2 2023.

Naturally, these higher charter rates significantly increased their net income, totaling $27.6 million, a significant increase from the $15.4 million reported in Q2 2023.

Outlook

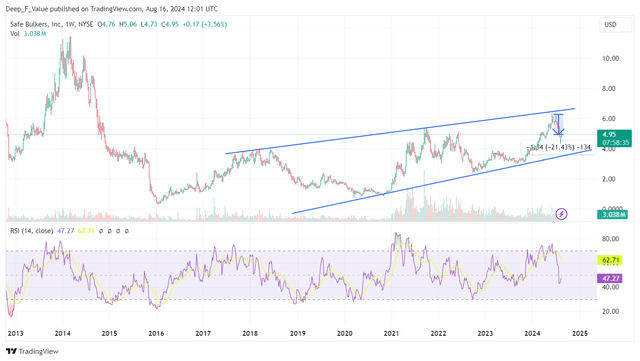

By looking at their share price on a weekly chart, we can see a pullback of 20% following a bull run since November 2023 that increased the share price by 100%.

Trading View

In my view, a pullback of this size is a healthy sign, especially after the share price approached the upper level of a trend line in the weekly chart.

I have to admit that I trust mainly support and resistance levels, and tend to be skeptical about trend lines. However, the fact that the price bounced several times on the upper and lower limit of these lines, makes me believe they are somewhat reliable, although I would take it with a pinch of salt.

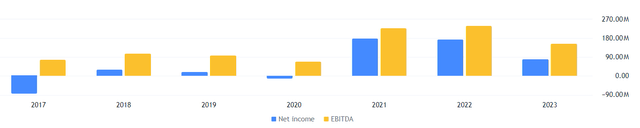

What I trust more in these cases is their financial statements. A quick look at the income sheet shows that net income and EBITDA are down from 2021. Despite that, the share price is pretty much at the same level as it was in 2021.

Trading View

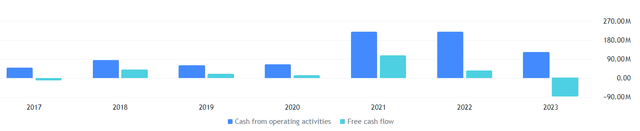

When looking at their cash flow statement, a similar pattern is shown for the cash flow, and free cash flow. The fact that free cash flow was negative in 2023 makes me concerned, given that they have been paying a quarterly dividend of $0.05 per share since 2022.

Trading View

Why is this concerning? Well, if I see companies with a tight free cash flow that pay a good dividend (dividend yield for Safe Bulkers was 5% in 2023), I see a risk of the company cutting its dividend in the near term.

Usually, the announcement of a lower dividend payout is followed by a sharp decline in the share price, especially for companies with declining financial metrics and negative free cash flows, as shareholders are invested due to the good dividend yield. As soon as this yield goes down, so does the share price, in my view.

In regards to their debt, I am not overly concerned, given a quick ratio of 1.88, and a debt-to-assets ratio of 0.37.

When looking at their profitability ratios, I like the fact that despite the decline in operating margins, they increased their net margins in the past few quarters.

Trading View

There were no share buybacks in Q2 2024, however, I am encouraged that in Q1 2024, they bought back over 4.8 million shares, from their 5 million authorized program, approved at the end of last year.

In my view, this was a very good decision, considering the bull run since the end of last year.

Given that their share buyback program was terminated in April 2024, and no announcement of a new program has been made in their Q2 2024 results, I remain skeptical about the short and mid-term future of the share price.

In my view, the 20% pullback that we have seen since mid-June could continue down to the lower trend line. That would be close to the $4 price level, therefore I maintain a Hold rating until I see some price consolidation, ideally accompanied by an announcement of a new share buyback program.

Conclusion

In my view, Safe Bulkers presents a mixed investment case.

On one hand, I highly favor their relatively new vessel fleet, with a strong improvement in charter rates in Q2 2024, particularly in the Capesize and Panamax segments.

However, I am discouraged by the disconnection between some of the key financial metrics in their financial statements, and the share price. I don’t like the fact that net income and operating cash flow have been declining since 2021, however, today, the share price is at a similar level.

Also, the fact that they haven’t announced a new share buyback program in Q2 is also concerning, especially when considering that they repurchased in Q1 over 4.8 million shares, from their 5 million authorized program.

Given these factors, I recommend a Hold rating until I see more favorable price action and a new share buyback program.

Read the full article here

")

")