")

")

Earlier this year, when social giant Reddit (NYSE:RDDT) went IPO, I wrote a bullish article about the company. My article was published shortly after the firm closed up a whopping 48.4% for its first day of trading. And in that article, I talked about some of the firm’s troubles, particularly how it was struggling to become profitable and cash flow positive. Having said that, the overall trajectory of the business was great and growth was robust. Add on top of this the significant amount of net cash the company had on its books, and I believed that the overall outlook for the company was bullish. This led me to rate the company a ‘buy’.

Since then, things have gone quite well. Shares are up 21.1% at a time when the S&P 500 is up only 7.5%. Considering that this was just five months ago, back in late March, I believe that this represents a meaningful degree of outperformance. But of course, even the best opportunities have only limited upside. So after seeing how much shares had risen, I figured it would make sense to look back again and see if it might be time for a downgrade. Although that was my initial hunch coming into this article, I ultimately concluded the opposite. While shares certainly don’t deserve an upgrade, I do think that they have further upside from here, especially for those who are willing to hold the stock for the long haul. So because of that, I have decided to keep the company rated a ‘buy’ for now.

Fantastic growth

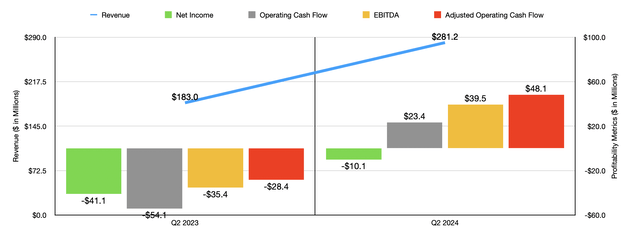

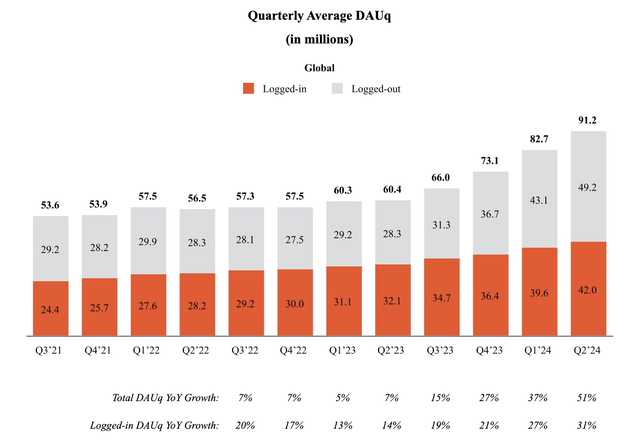

Fundamentally speaking, things have improved for Reddit in a very short period of time. For instance, if you look at the most recent quarter on its own, which would be the second quarter of the 2024 fiscal year, revenue for the company came in at $281.2 million. This represents an increase of 53.7% compared to the $183 million the company generated in revenue just one year earlier. The most significant driver behind this growth was a surge in the number of DAUq (Daily Active Uniques). This is basically the number of daily active users on the platform that are distinct from one another.

Author – SEC EDGAR Data

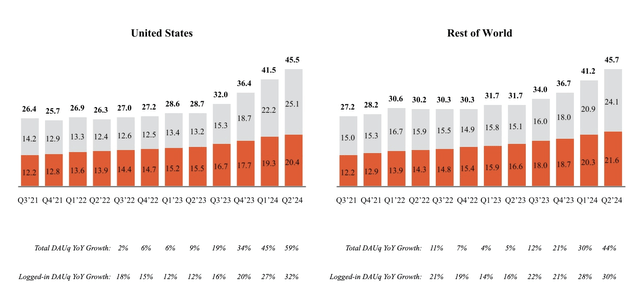

Globally, this number was 91.2 million. This translated to a nice increase over the 82.7 million reported for the first quarter of the year. It was also 51% above the 60.4 million that the company had for the second quarter of 2023. A good chunk of this growth came from the US. From the second quarter of last year to the second quarter of this year, the number of US users jumped from 28.7 million to 45.5 million. Put another way, 54.5% of the growth that the company saw on a year-over-year basis came from the US. From the rest of the world, Reddit reported growth from 31.7 million to 45.7 million.

Reddit

Now, it is important to temper expectations. This is because management measures two different types of DAUq. The first type is those that are logged in to a registered account. And the other would be those that are logged out. This is an important distinction because, according to management, users that are logged into a registered account have a higher engagement rate and spend more time on the platform compared to those that are not. By definition, these users are more valuable. Unfortunately, only 32.1%, or 9.9 million, of the year-over-year increase in DAUq came from logged in accounts.

Reddit

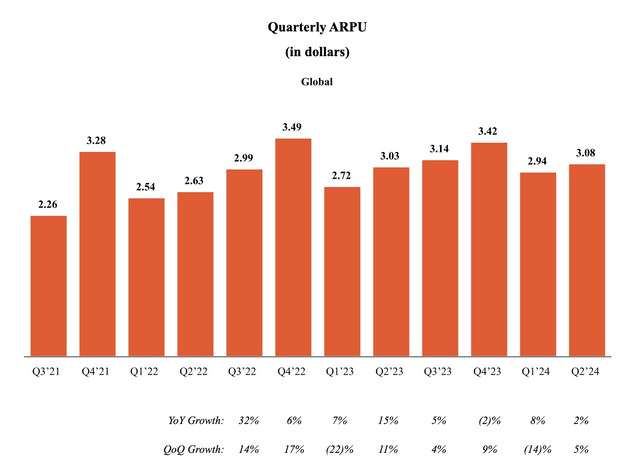

Even though there was an imbalance in the DAUq count reported by management, monetization for the company continues to grow as well. During the most recent quarter, the average user was responsible for $3.08 in revenue. This represents an increase over the $3.03 reported one year earlier. Although this may not seem like much, this disparity, given the current DAUq figures reported by management, translates to an extra $18.2 million in annualized revenue for the company.

Reddit

In the past, I was concerned about the profitability of the business. But these concerns are quickly going away. In the second quarter of 2023, Reddit generated a net loss of $41.1 million. That loss in the most recent quarter was $10.1 million. But that’s not all. Other profitability metrics are improving rapidly as well. Operating cash flow went from negative $54.1 million to positive $23.4 million. If we adjust for changes in working capital, the improvement was from negative $28.4 million to positive $48.1 million. And finally, EBITDA for the company went from negative $35.4 million to positive $39.5 million.

Author – SEC EDGAR Data

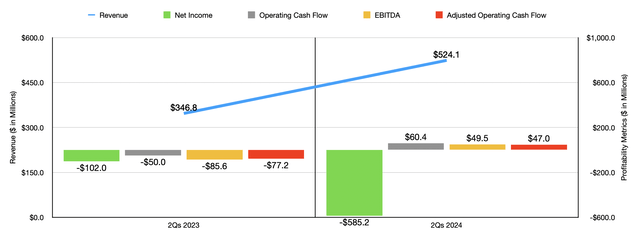

In the chart above, you can see financial results for the first half of 2024 compared to the same time of 2023. As was the case with the second quarter on its own, revenue and cash flows improved markedly. Overall sales were up 51.1% year over year, driven by the same factors that impacted quarterly figures. It is true that the company went from generating a net loss of $102 million to generating an even larger net loss of $585.2 million. But this was because of a $619.2 million increase in stock-based compensation from last year to this year. This makes sense when you consider the timing of the company going public. When we remove this from the equation and focus on other profitability metrics, the picture looks much better. Operating cash flow went from negative $50 million to positive $60.4 million. On an adjusted basis, it improved from negative $77.2 million to positive $47.8 million. And finally, EBITDA for the company expanded from negative $85.6 million to positive $49.5 million.

In all likelihood, this overall trend toward profitability will continue. For the third quarter of this year, management is forecasting EBITDA of between $40 million and $60 million based on revenue of between $290 million and three $110 million. In all likelihood, other profitability metrics will follow suit. A big question that investors are likely to ask, however, is whether or not shares are fairly valued. This is a difficult question to answer because we don’t have any idea as to the consistency of cash flows. We just know that they are improving rapidly. The best way that I know of to answer this question is not to ask if shares are fairly valued, but to ask what the company needs to generate in order to be fairly valued and whether or not that seems likely to occur.

Author – SEC EDGAR Data

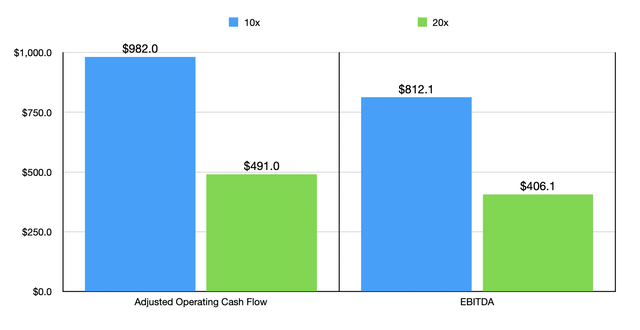

In the chart above, you can see how much adjusted operating cash flow that Reddit would need to generate in order to be fairly valued at either 10 times or 20 times on a price to adjusted operating cash flow basis. You can see the same thing for EBITDA using the EV to EBITDA multiple. The reason why this is lower as opposed to higher is because the company has $1.70 billion of net cash on its books. This provides increased stability, and it reduces the enterprise value of the business. Even if we annualize the high end of results from what management anticipates for the third quarter, we would have EBITDA of $240 million. So we are a bit away from that point. But the rapid increase in growth for the company means that future years should be better.

Author – SEC EDGAR Data

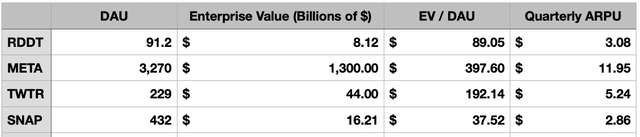

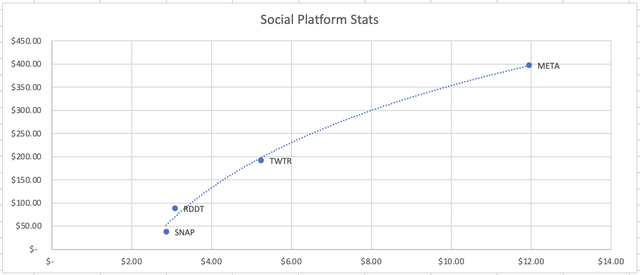

Another thing I wanted to look at was how Reddit stacks up against similar businesses. In the table above, you can see the daily active users for it, as well as for Facebook parent Meta Platforms (META), Snap (SNAP), and Twitter right before it was acquired by Elon Musk for $44 billion. This table looks at the enterprise value for each daily active user on the platform compared to the same metric for the comparable businesses. At $89.05, Reddit is lower than two of the three companies. It is certainly near the lower end of the spectrum. However, as the table also shows, the average revenue per user each quarter also places the company similarly compared to the other businesses. In fact, as the chart below illustrates, there does seem to be some relationship here between overall size and average revenue per user on a quarterly basis.

Author – SEC EDGAR Data

*X-Axis is quarterly ARPU and Y-Axis represents EV/DAU

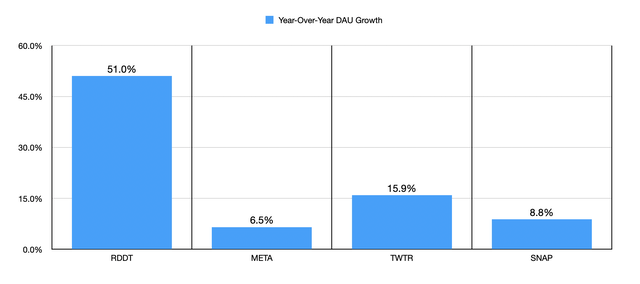

This approach would suggest that Reddit’s valuation is more or less in line based on the size of its user base and how much in revenue it generates per user. However, in the chart below, you can also see the year-over-year growth in user count achieved by each of these businesses. As a note, for Twitter, this growth was based on the most recent quarterly data that was available at the time that it was announced the company would be purchased by Elon Musk. But the others are all based on the most recent quarter. What we have here is a company that’s growing at a much more rapid pace. If we extrapolate that into the future, we can see how things might change. For instance, if we see a 30% user growth rate over the next year, that would imply upside for shareholders of about 24.8%. Although we don’t know what the future holds, with the tremendous amount of cash the company has on hand and its recent growth trajectory, I would say that this kind of expansion is not out of the question.

Author – SEC EDGAR Data

*Data taken from here, here, and here.

Takeaway

Based on all the data provided, I must say that I am impressed with the progress that Reddit has been making. Even though it doesn’t fit my definition of a value investment, the company does seem to be a growth opportunity that’s trading at a reasonable price for the prospects it offers. Obviously, this could change if growth, so I was dramatically, or if the company shrinks. But outside of that, it’s difficult to imagine this turning out to be a bad prospect. Given these factors, I believe that keeping the company rated a ‘buy’ makes sense for now.

Read the full article here

")

")